The long-term plans of China’s biggest wind developers, as detailed in the new GTM Research/Azure International China Wind Market Quarterly: 4th Quarter 2012, reflect a renewed commitment to renewables by the Chinese government.

“The government appears to be back in the game of promoting the domestic renewable energy market,” according to the report. New policies, including new additions to the government’s 2013 targets for solar (10 gigawatts) and wind (18 gigawatts) and a streamlining of access to subsidy funding, are expected “to act as a counterweight to forces outside of China that have hurt the wind and solar sectors.”

Recent signs of an improving domestic Chinese economy and waning anxiety about Europe’s financial crisis add to growing optimism in China’s renewables sector, according to the report.

Though major Chinese wind manufacturers like Goldwind (HKG:2208), Sinovel (SHA:601558), and Ming Yang (NYSE:MY) struggled through the same kind of inventory clearing losses China’s solar panel manufacturers had to endure in 2012, developers fared better, thanks to pipelines that only slowed installation activity gradually and ongoing revenues from past projects.

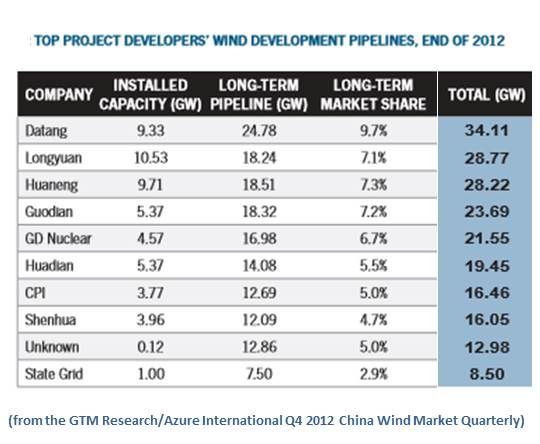

China’s top three wind developers are Longyuan, Huaneng, and Datang, in that order. Reflecting an ongoing consolidation of big players, the top ten wind developers took approximately 70 percent of China’s Q4 2012 development market.

Longyuan (HKG:0916) is a subsidiary of the Guodian Group, one of the five dominant power-sector state-owned enterprises (SOEs) that provide electricity from all generation sources. Also among the Big Five SOEs are the Huaneng Group, which owns wind developer Huaneng Renewables, and the Datang Corporation, which owns Datang, China’s fastest-growing big wind developer.

Though the Q4 wind installations increase was smaller than in prior years, China’s wind developers’ pipelines reflected optimism about the sector. But grid integration and policy challenges, the report cautioned, “may not be explicitly figured into these corporations’ ever-more-ambitious wind development plans.”

On the other hand, big power producers appear to be “enticed by higher profits than their conventional generation businesses,” the report noted, “and will continue to invest heavily in wind power.” Guangdong Nuclear, for instance, was among the Q4 wind development leaders, with Q4 growth of 26 percent.

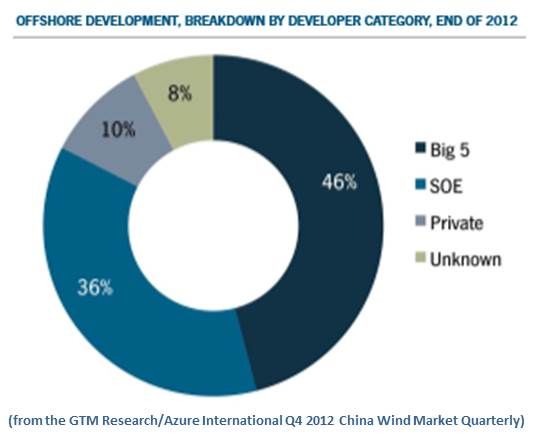

Longyuan showed a year-on-year 1H 2012 4.6 percent increase in net profit (RMB 1,821 million) and a 12.4 percent increase in revenues. Longyuan is leading China’s incipient offshore wind sector, though the increased cost and delay between construction and production of ocean development may hamper the company going forward.

Huaneng Renewables (HKG:0958) had a year-on-year 1H revenue growth of 2.4 percent. Net profit fell 62 percent (RMB 277 million) due to increased ledger expenses.

Datang (HKG:1798), which currently has the biggest development pipeline among the big three, increased its 1H revenues by 2.8 percent, though its profit fell 90 percent (RMB 61 million) due to increased ledger expenses. Nevertheless, “Datang is poised to become the largest wind company in China,” the Quarterly reported,” increasing its market share from 16 percent to 20 percent.”

The pipeline numbers may, the report added, underestimate the growth potential of developers such as Hebei Construction Group, State Grid and China Resources (HK:0836), because “industry development targets tend to favor China’s well-established Big Five power producers.”

42

42

15

15

9

9