The U.S. is going to deploy 1.2 gigawatts of photovoltaic solar power this quarter.

That's the kind of news that serves as a bellwether for the solar market, not the SolarCity IPO. If you were looking for the now-humbled SolarCity IPO to serve as the greentech savior and for Elon Musk and Lyndon Rive to lead solar to the promised land, then you were the victim of facile thinking.

The solar industry is going to be lifted out of its doldrums by getting to massive volumes at lower prices at residential, commercial, and utility scale -- not by accounting tricks, exploiting tax investment schemes, or overvalued IPOs. Those are the tools of Solar 1.0.

Solar 2.0 requires the massive consolidation that the market is currently slogging through. Solar 2.0 is when photovoltaic solar competes with fossil fuels in an unsubsidized environment. Certainly, the third-party financing pioneered by SolarCity and others is a tool in the toolbox, but it's not a panacea. Solar needs manufacturing efficiency, capacity that matches demand, and regulatory and policy consistency, as well as the innovative financing offered by the disappointed IPO aspirant and firms like Clean Power Finance, Sungevity, Sunrun, SunEdison, and OneRoof.

And that brings us to today's data point.

According to GTM Research, the U.S. will install 1.2 gigawatts of photovoltaics in the fourth quarter of 2012.

That healthy quarterly number will bring the annual U.S. solar total to 3.2 gigawatts for the year and set the U.S. up for 3.9 gigawatts of solar deployed in 2013, according to GTM Research.

The analysts at GTM forecast the U.S. solar market at 8 gigawatts in 2016.

Shayle Kann, Director of Research at GTM, notes that the U.S. market tends toward an odd seasonality, with installers rushing to complete projects before incentives wane or contracts impose penalties. The most recent U.S. Solar Market Insight report notes, "In 2010 and 2011, the fourth quarter represented 41 percent and 42 percent of all annual installations, respectively," adding, "To be sure, much of this forecast hinges on the timely completion of a number of utility-scale projects currently in the late stages of construction."

Kann also notes that the U.S. has the "firepower" to deploy gigawatt levels of solar every quarter.

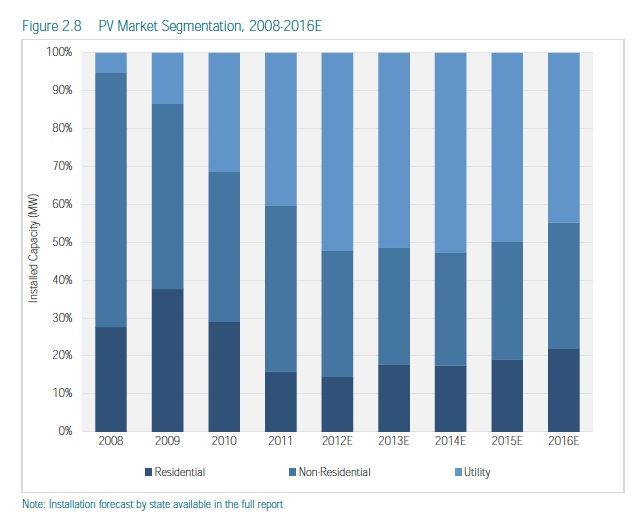

Here's the sector breakdown according to the GTM Research analyst team. The obvious takeaway is the marked stress on utility scale, not residential, over the next few years in the U.S.

More detail on the U.S. solar market can be found in this quarter's U.S. Solar Market Insight report. To download the free Executive Summary, visit www.greentechmedia.com/research/ussmi.

41

41

15

15

9

9