In January, BYD captured the world’s attention when it announced the completion of one of the world’s largest battery energy storage systems, a 36-megawatt-hour lithium-ion battery system, located in Zhangbei, Hebei.

In fact, BYD’s system is only one part of China’s first national energy storage project. When fully commissioned later this year, the Zhangbei system will reach 20 megawatts/95 megawatt-hours, representing six energy storage providers and three distinct technologies.

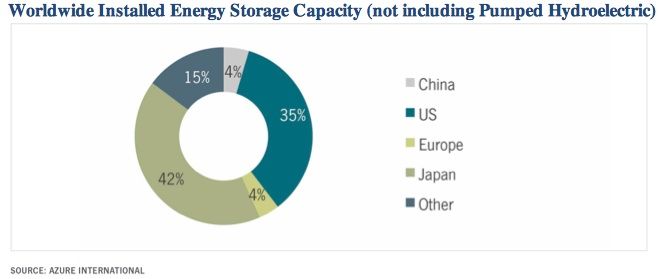

The Zhangbei project marks China’s first big move into the worldwide energy storage market, where China is currently far behind other countries. In 2012, China will lead the world in installed generation capacity, total electricity generated, installed wind capacity, and investment in renewable energy. These facts alone suggest that it should also be the most promising market for energy storage in the world, yet China currently has just 4 percent of the worldwide installed advanced energy storage capacity.

A recent report, China Grid-Scale Energy Storage Market 2012-2016, published by GTM Research, reveals why China’s energy storage market has lagged and why it may soon enter a new phase of rapid growth despite facing major market-design hurdles.

The report finds that the market for energy storage in China is unique from those in other regions in several major respects. First, storage applications have a higher potential value in China due to the high penetration of both wind energy and coal power, and due to rapid transition between an electricity market dominated by flat industrial demand to one with fast-growing “peaky” demand from urban residents. The second major respect in which China differs concerns underdeveloped electric power markets which can hold back storage options.

Major issues driving the need for storage

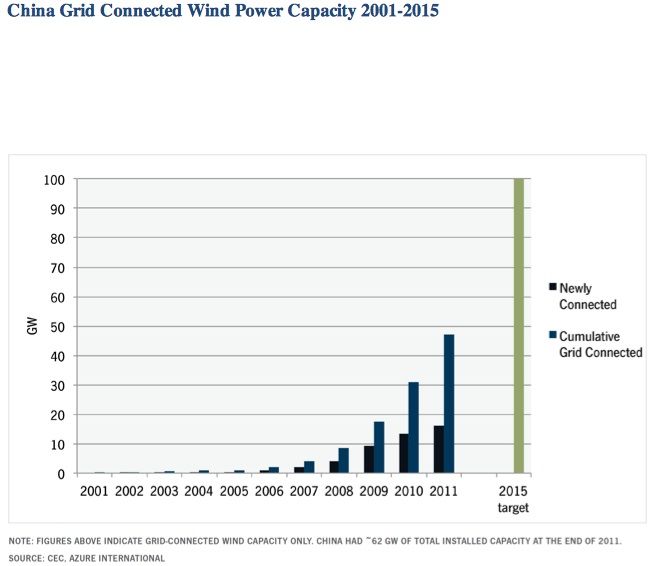

Renewable integration: Wind power has grown rapidly in recent years due to aggressive government targets and policies. At the end of 2011, China had 47 gigawatts of grid-connected wind capacity, and the 12th Five-Year Plan calls for 100 gigawatts by the end of 2015. The 12th Five-Year Plan also calls for 15 gigawatts of solar capacity by 2015. But China’s grid operators have struggled to absorb wind power. In 2011, almost 17 percent of electricity produced in China’s top 10 wind power bases was curtailed, with curtailment reaching as high as 25 percent in Gansu province.

Inflexible generation: As of the end of 2011, coal-fired power plants accounted for over 65 percent of installed capacity and provided over 75 percent of China’s electricity. Large coal-fired power plants have long startup times, require high minimum loads, and cannot be cycled (turned on and off) on a daily basis. This limits their ability to match large differences between peak and off-peak demand. In regions with high penetration of combined heat and power (CHP) plants, generation is even less flexible. Inflexible generation is a major contributor to wind power curtailment.

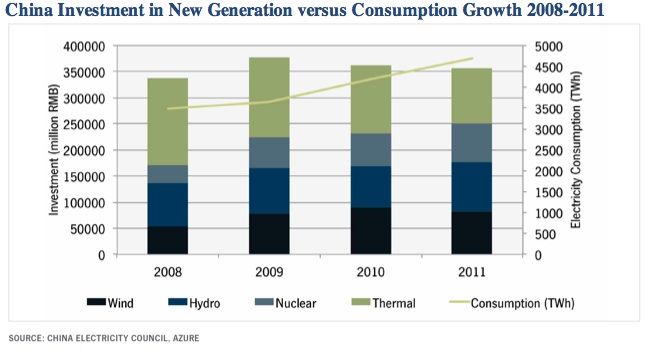

Load growth: From 2011 to 2015, China’s electricity consumption is expected to grow at an annual growth rate of 7.5 to 9.5 percent. While power consumption continues to grow, investment in new generation -- especially in thermal generation -- has been in decline. This has led to increasing power shortages -- there is simply not enough new generation capacity coming on-line to meet growing demand. The China Electricity Council forecasts power shortages reaching 30 gigawatts to 40 gigawatts in 2012 and 70 gigawatts in 2013.

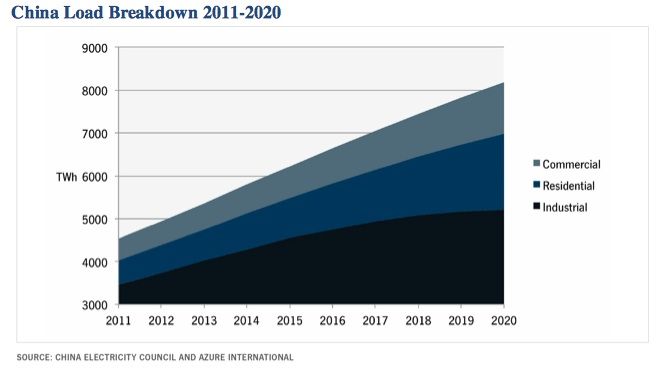

Changing Lload: Load in China is not only growing at a rapid pace, it is also becoming “peakier” as residential and commercial load rises more quickly than industrial demand. Though industrial demand will continue to dominate consumption, rising residential and commercial loads have already posed problems for grid stability. New economic reforms also focus on shifting the economy toward the commercial and advanced industrial sectors as opposed to energy intensive heavy industries. As the quality of life for China’s residents continues to improve, so will the adoption of air conditioning and other appliances along with the demands those loads place on the grid.

In terms of inherent need for energy storage solutions, China ranks among the top countries in the world. However, the path toward commercialization contains a number of significant obstacles related to power market design.

Market not structured for many storage applications

In China, prices for wholesale energy and ancillary services are fixed by provincial pricing authorities, and, with the exception of several provinces, prices do not vary over the course of a day. While fixed prices simplify the calculation of expected revenues, they hide the overall cost of generation and provide little incentive for generators and other technologies designed to supply power only during peak load (e.g., peaker plants).

Fixed prices within the Chinese power market misalign incentives: the actual value of the services an energy storage system can provide (as defined by the cost savings it provides to the system as a whole) may differ from the compensation it will receive. This is particularly the case in China’s recently established ancillary service markets. The compensation for these non-voluntary services is often well below the variable cost of providing them, let alone the full costs.

China’s power market was designed to compensate large coal-fired plants. As a result, it is not optimized for a more balanced set of competing technologies. In some cases, the definition of ancillary services are so specific to coal-fired generation that they cannot be applied to competing technologies, including energy storage. Energy storage can be used to shift a greater amount of baseload power to meet peak demand, as well as provide ancillary services much more efficiently and accurately than coal-fired power plants. While current compensation mechanisms do not reflect this fact, there are some indications that the government will further reform the power market system or provide additional funding for energy storage operated within the grid. After all, power shortages and grid instability are issues that the government cannot ignore.

Government policy priority

While China’s market structure is the biggest barrier to energy storage, the government’s will to win appears resolute enough to overcome these difficulties. The central government has made it clear that it intends to pursue energy storage and batteries as part of the same set of national industrial policies that have helped other renewable energy sources achieve scale in the country. In the short term, this will likely lead to a number of additional demonstration projects, some of which may have the same scale and impact as the Zhangbei project. Though many may dismiss the market for pre-commercial technologies as unappealing, the size of these projects and growth rate they could represent will make them just as interesting for players in the industry as their forerunners in wind and solar before those fields achieved commercial scale.

Findings

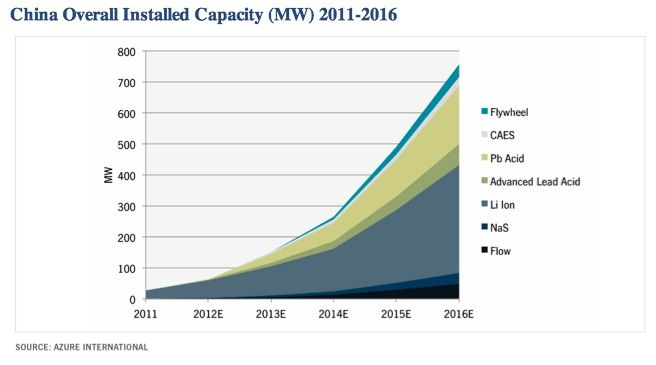

The Chinese energy storage market will grow at a 92 percent compound annual growth rate from 2012 to 2016, with annual sales reaching $482 million in 2016. In 2016, the total installed capacity will exceed 750 megawatts. Lithium-ion and lead acid will take the largest share of the market.

- Despite high growth, China’s energy storage market will remain in the demonstration market stage for several reasons. China’s grid power market is not yet structured to provide incentives for certain important energy storage applications, and needed reforms may be too complex and far-reaching to implement in the next few years. Chinese power producers and grid operators are just beginning to work with energy storage.

- Over the next five years, the energy storage market will be driven by policy, which may include feed-in tariffs, large-scale demonstrations, and directives to certain regions and companies to develop the industry further.

- Attractive applications within China’s energy storage market will differ substantially from the U.S. market. China will emphasize energy-oriented applications over power-oriented applications.

- An intangible wild card exists within the set of quantifiable activities and data. The Chinese government, and companies participating in the Chinese electric power sector, have proven to be much more dynamic than many experts in Western countries had predicted. For example, the wind industry in China shot from insignificance to world-leading in a period of just five years. This ascent was propelled by what outside observers initially dismissed as weak policy (namely, China’s 2004 Renewable Energy Law), due to lack of understanding of how China functions. Most experts have underestimated the will, ability and intention of China to expand domestic energy resources to ensure national energy security.

More details vital for energy storage developers, grid operators, and power producers looking to enter or understand China’s energy storage market can be found here.

41

41

15

15

9

9