Four greentech IPOs are seemingly going to make it through the IPO gate in spring 2012. It's the biggest flurry of greentech IPOs in memory and serves to show the diversity of the greentech field.

It's a disparate collection of firms: Enphase, a small cap PV microinverter pioneer, BrightSource Energy, a massively ambitious concentrated solar power (CSP) developer, Enerkem, a municipal-solid-waste-to-fuel firm, and Luca Technologies, a firm that performs "active biogenesis of methane." BrightSource, Enerkem, and Luca are expected to debut this week. Both Enerkem and Luca were scheduled for last week but apparently could not "fill their book."

What these firms do have in common is that they are all VC-funded and will all be losing money for the foreseeable future.

***

Enphase has been a public company for one week now.

Enphase (Nasdaq:ENPH), the Petaluma-based microinverter firm priced its IPO on March 30 and saw its stock jump from the $6.00 start price. The company raised $54 million in its initial public offering and has a market cap of approximately $285 million. A colleague remarks that this places the company in a micro cap category. And that poses some challenges in the investor relations and analyst coverage department. Other big challenges for Enphase are maintaining its meteoric sales growth amidst increasing competition and finding a path to profitability in a still difficult market.

Enphase stock price as of April 6, 2011.

***

BrightSource Energy is looking to raise up to $182.5 million in its initial public offering. The Oakland-based solar firm plans to issue 7.9 million shares, at a price of $21 to $23 per share, according to an updated SEC filing, and plans to price the shares on April 12, almost a year after registering its S-1 with the SEC.

BrightSource is in the massive-scale concentrating solar power (CSP) business, a technology which addresses a common refrain about the limitations of photovoltaic solar power -- that the technology only works when the sun is shining. CSP boasts the ability to store thermal energy long after the sun goes down. This ability improves CSP's capacity factor and dispatchability, and has the potential to improve CSP's levelized cost of energy (LCOE).

BrightSource’s power tower solar thermal system uses a field of software-controlled mirrors called heliostats to reflect the sun’s energy onto a boiler atop a tower to produce high-temperature and high-pressure steam. The steam is used to turn a conventional steam turbine to produce electricity. When paired with storage, the steam is directed to a heat exchanger, where molten salts are further heated to achieve a higher temperature, storing the heat energy for future use.

BrightSource has won more than $500 million in VC funding from VantagePoint Venture Partners, DBL Ventures, DFJ, Alstom, et al. BrightSource has also received project funding from NRG and Google, as well as $1.6 billion in DOE loan guarantees for the Ivanpah project.

CSP needs every advantage it can muster, given the plunging cost of PV and the exploding scale of the global photovoltaic market. In fact, a number of planned CSP plants have switched to PV because of the challenging economics of CSP, as well as financiers' familiarity with PV.

GTM Research has looked at the LCOE economics of CSP in a recent report, Concentrating Solar Power 2011: Technology, Costs and Markets. GTM calculates that CSP towers with storage can earn higher revenue and profits per kilowatt-hour than PV. The high-level finding is that power tower technology is cost-competitive with PV on a levelized cost basis, and that power tower with storage could represent the lowest cost per kWh solar option in 2016 and beyond.

BrightSource has signed 13 power purchase agreements (PPAs) to deliver approximately 2.4 gigawatts of installed capacity to two of the largest electric utilities in the U.S.: PG&E and Southern California Edison.

According to the S-1, BSE has a development site portfolio of approximately 90,000 acres under its control in California and the U.S. Southwest, with the potential to accommodate approximately 9 gigawatts of installed capacity. Two California sites are currently in advanced development: Rio Mesa Solar (6,600 acres) and Hidden Hills Ranch (10,000 acres).

The S-1 is not very forthcoming about the pricing that has been negotiated for these PPAs. This document from PG&E states, "The price of procurement under [Ivanpah] Projects 1 and 2 is equal to or less than the applicable 2008 MPR (Market Price Referent)." 2008 MPR numbers can be found here. A 25-year PPA starting in 2012 shows a 2008 MPR of $0.1251 per kilowatt-hour. The S-1 also doesn't go into detail about the amount of transmission-buildout required for that "9 gigawatts of installed capacity."

The fate of the stock price will indicate institutional investors' take on CSP technology -- pitting massive scale at potentially low cost versus the exposure CSP faces in permitting, environmental and financing risk. For the year ended December 2011, BrightSource generated $159.10 million in revenues, and lost $110 million. Competitors in the CSP with storage market include SolarReserve and Abengoa.

Greentech Media's LCOE Forecast for Various Solar Technologies

_566_418_80.jpg)

***

Enerkem, a Canadian municipal-waste-to-cellulosic-ethanol conversion firm filed its F1 with the SEC to go public on the Nasdaq in February of this year. The firm is looking to raise up to $158 million by offering 8.3 million shares at a price range of $17.00 to $19.00. The firm had $3.4 million in income and $26.4 million in losses in the last 12 months.

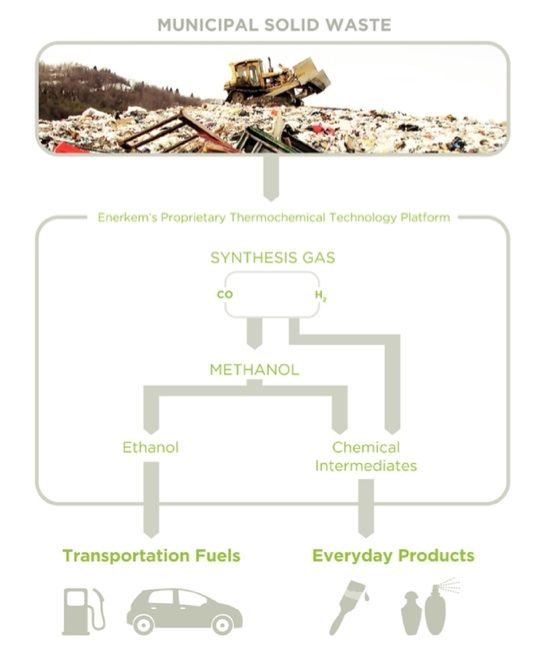

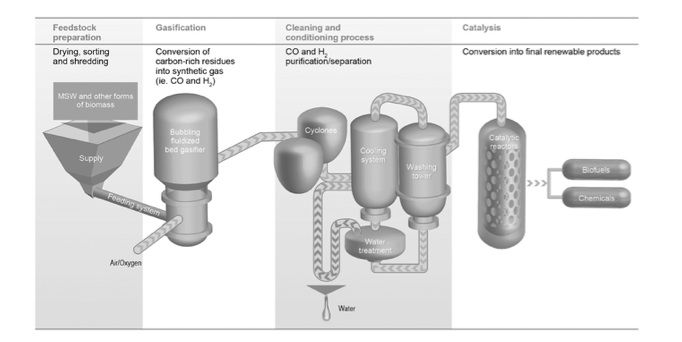

The company was founded in 2000, and has developed a “proprietary thermochemical technology” platform to process municipal solid waste (MSW) -- otherwise known as trash -- into syngas, which can then be converted into methanol and then ethanol, or other chemical intermediates.

Enerkem's platform can apparently accept nearly anything, including “mixed textiles, plastics, fibers, and wood.” The company also claims that its gasification process has lower operating and capital costs than syngas competitors “due to lower temperature, pressure and energy requirements to break down heterogeneous waste feedstock.”

Enerkem says it has validated its technology over the course of its 10-year operating history, first at a small-scale (4.8 metric tons per day) pilot plant in Sherbrooke, Quebec, Canada, and later at a commercial demonstration facility in Westbury, Quebec, Canada which is currently processing ten times that amount. The glaring issue is that Enerkem has yet to convert methanol into ethanol at its demo plant. It's not exactly a difficult process, but the fact that the company is waiting for a full-scale plant to do so could lead to production and logistical problems.

Of course, that's only a commercial demo plant. Enerkem is still in the development stage and has yet to generate any significant revenue. That may change soon: Enerkem is currently building a 10-million-gallon-per-year plant in Edmonton, and has already secured a 25-year MSW feedstock supply agreement with the City of Edmonton. The company claims that facility, with seven times more production than its demo plant, will have the lowest scale-up to full commercial capacity to date of any cellulosic ethanol producer, which helps mitigate ramp-up problems that can plague a firm's projections.

In addition, Enerkem has a pair of 10-million-gallon-per-year plants of the same design being developed in Pontotoc, Mississippi and Varennes, Quebec, Canada. On top of those facilities, Enerkem is negotiating non-binding agreements to sell its proprietary systems to two of its strategic shareholders, Waste Management of Canada and Valero. Other investors in the company include Rho Ventures and Braemar Ventures.

- At 10 million gallons per year, Enerkem thinks it can produce ethanol at $1.50 to $1.70 per gallon.

- Enerkem's most recent round of fundraising netted $30 million.

Additionally, the firm expects to receive payments for accepting trash, known as tipping fees. Enerkem cites an industry publication in saying that average landfill tipping fees were $47 per metric ton in 2009.

According to Enerkem, there are 140 million metric tons of waste produced in the U.S. every year that are suitable for its platform. At its target of 100 gallons of ethanol per metric ton of sorted waste, that's enough headroom for 14 billion gallons of ethanol production a year.

It all comes down to a familiar story with biofuel IPOs as of late: If Enerkem hits its projections, it has an interesting model in a sector that's not extremely populated.

But right now, that's still a big “if" despite the positive drivers of the U.S. Renewable Fuel Standards Program which mandates that 16 billion gallons per year of cellulosic biofuels be blended in the national transportation fuel mix by 2022.

***

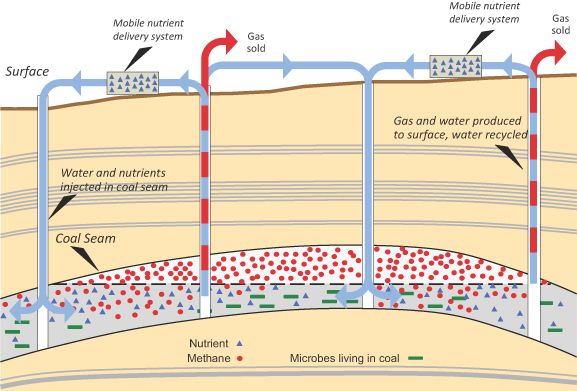

Luca Technologies of Golden, CO is looking to raise up to $125 million in an IPO on the Nasdaq. The firm uses naturally occurring microorganisms to generate natural gas. "Our proprietary technology stimulates native microorganisms that reside in subsurface hydrocarbon deposits, such as coal, oil and organic-rich shales, to accelerate the bioconversion of these resources into methane," according to the firm. Investors in the company include Kleiner Perkins Caufield & Byers and One Equity Partners.

In 2011, Luca reported a loss of $18 million and revenue of $1.0 million. In 2010, Luca reported a loss of $20 million with revenue of $2.4 million.

According to the S-1:

We leverage the ability of naturally occurring microorganisms to convert subsurface hydrocarbon deposits, such as coal, to methane gas. This complex process is susceptible to interruption by various chemical and biological conditions, including traditional coalbed methane development which involves removing water from the coal seam to reduce pressure and allow previously adsorbed natural gas to flow up a well. As a result, the natural and ongoing biogenic creation of methane gas slows or ceases, with a large mass of unutilized hydrocarbon deposit remaining in place underground.

To accelerate biogenic methane gas production rates, we use our proprietary Restoration Process to deliver customized nutrient formulations and water to restore coal reservoir habitats to conditions that may enable native microbial communities to be enhanced to create commercial volumes of natural gas on a real-time basis. We produce this newly created natural gas and deliver it to market using existing wells, pipelines and natural gas infrastructure.

Oil and natural gas resources developed and produced by the traditional E&P industry often exhibit production rates that peak early in the lives of wells, and then steeply decline as stored hydrocarbons are depleted and pressure is reduced. In contrast, wells producing newly created methane gas using our Restoration Process are more akin to “gas farms,” producing natural gas at lower, but constant or slightly increasing rates for extended periods of time.

Our Restoration Process is designed to sustain the life processes of naturally occurring microbial communities. We do not introduce foreign microbes, nor do we rely upon genetically-engineered microorganisms. Microbes are already present in coalbed water and are responsible for biogenic methane gas creation. The first step in our Restoration Process involves the identification and assessment of underground environments where the native conditions are suitable for microbial life activation, and where the biogenic process has been active in the past. As a second step, we perform lab and field studies to assess microbial activation. In the lab, using water and hydrocarbon deposits from a prospective basin, we attempt to identify optimal nutrient formulations for methane creation. These nutrient formulations are then field-tested prior to initiation of commercial activity within an area or basin.

Single-digit millions revenue that has decreased from the previous year does not seem like an encouraging sign for what looks like a wildcatting business, albeit one with an interesting biotechnology angle. This type of business might have been interesting when natural gas was at $7 to $8/mmbtu. The business is a lot less interesting at today's $4/mmbtu price.

Ray Lane is currently the KPCB board member at Luca, having taken over after KP's Jonn Dennison and Ben Kortlang left that role -- which seems like a bit of churn at the board level.

***

Derek Mead contributed to this article.

41

41

15

15

9

9