The electricity business of 2024 is going to look a lot different than the situation today -- and the utility industry knows it.

The Electric Power Research Institute, a 501(c)(3) nonprofit, is essentially the research arm of the electrical utility industry. The group's recent report, The Integrated Grid, is the first phase of a larger effort to look at distributed energy resources on the grid edge and their impact on business as usual. The report provides a technical rationale for staying plugged into the grid and a cogent argument in favor of capacity fees and charges for grid services. The authors also exhibit a fondness for smart inverters.

We spoke with EPRI's Jeffrey Hamel, the executive director of the Power Delivery and Utilization Team which authored the report (which can be downloaded here).

"The Integrated Grid can mean a lot of things to a lot of different people," said Hamel. But to him, it means "how DG resources, generation and storage all come together."

The report covers distributed energy resources such as "small natural-gas-fueled generators, combined heat and power plants, electricity storage, and solar photovoltaics on rooftops and in larger arrays connected to the distribution system."

In a presentation earlier this month, Hamel acknowledged that "there is a massive change underfoot." He said that all load growth was being met by renewables and natural gas. "We have to consider [what happens] when solar is not on-line" so "we may not have to build vast amounts of fast-ramp generation for a 7 p.m. system peak" He asks, "How do we ensure that the grid is optimized at a system level so we are fully utilizing all of the resources available, from central station generation to distributed generation?"

That's the perspective The Integrated Grid is trying to provide, said Hamel. "We want to provide the distribution system operator with insight." He added that "it's not just distributed generation; storage is coming."

"What's happening at the edge of the grid will affect what's happening at the transmission level," said Hamel.

Hamel suggested that "an integrated grid allows higher penetration of renewables" and will prevent curtailment of wind and solar. Hamel notes that distributed generation "is not just about variable sources," adding, "We can see a future with more gas-based DG. But customers will still remain connected to the grid. The grid provides voltage quality and startup power."

He continued: "Being able to integrate DER [distributed energy resources] into the planning and operation of the system is how we can get value out of the system." He said that distributed generation has to be incorporated into the grid with "visibility and control of these resources" through a management system incorporating sensors, communications and voltage control technology.

"Part of the work we're doing is on interconnection standards," said Hamel. He cited the IEEE 1547 DER interconnection standards working group and CPUC Rule 21. He said the team is watching German interconnection efforts with an eye toward smart inverters providing grid services such as voltage support, adding that "technology like smart inverters is already cost-effective."

Hamel suggested that "this type of innovation makes DG an enabler instead of a constraint."

What do utilities want?

Hamel didn't discuss rate structures during our conversation, but the report makes the case for the value of grid services and a need to revisit power market rules and rate structures. If EPRI is at all representative of its utility members, then here is what utilities want:

- "Capacity-related costs must become a distinct element of the cost of grid-supplied electricity to ensure long-term system reliability."

- "Power market rules that ensure long-term adequacy of both energy and capacity"

- "A policy and regulatory framework to ensure that costs incurred to transform to an integrated grid are allocated and recovered responsibly, efficiently, and equitably."

- "New market frameworks using economics and engineering to equip investors and other stakeholders in assessing potential contributions of distributed resources to system capacity and energy costs."

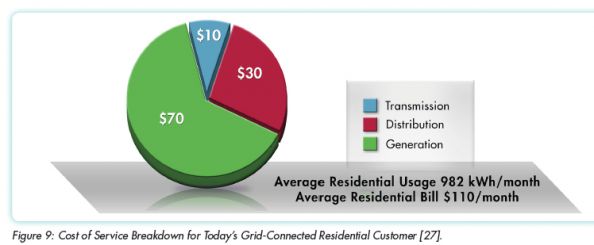

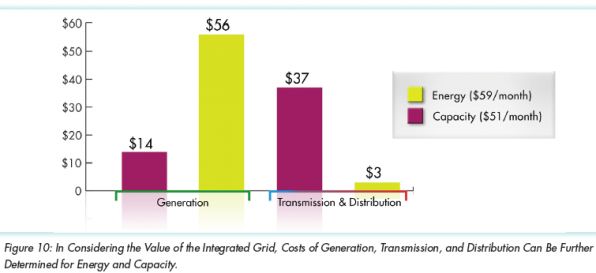

The report claims that "the cost of supply and delivery capacity can account for almost 50% of the overall cost of electricity for an average residential customer. Traditionally, residential rate structures are based on metered energy usage. With no separate charge for capacity costs, the energy charge has traditionally been set to recover both costs. This mixing of fixed and variable cost recovery is feasible when electricity is generated from central stations, delivered through a conventional T&D system, and used with an electromechanical meter that measures energy use only by a single entity."

But that's not the case when distributed generation enters the equation. The rate structures forced by the widespread advent of DER (and seemingly accepted by EPRI) appear to further shift the role of the utility to that of grid services provider rather than kilowatt-hour supplier.

41

41

15

15

9

9