[pagebreak:CarbonCaptureItsPossibleSolutionsPartII]

How do you combat a necessary evil on a budget? That's the dilemma with carbon capture. Scientists, policy makers and energy companies all agree that carbon dioxide from coal burning plants needs to be kept out of the atmosphere. The problem is how to do it without running up expenses that will make China, India, the United States and even Europe retreat behind years of prototype trials.

Thus far, carbon capture and sequestration (CCS) has been concerned with research and very little about actually putting the technology to real use. In Part I: Carbon Storage, the Money and the Market, we examined the history of carbon capture. Below we'll look at some of the forces driving the carbon market.

Part II: Carbon Economics

The Market

Carbon capture and sequestration has the potential to account for 220 to 2,200 gigatons of CO2 over the next century, says the Intergovernmental Panel on Global Change (IPCC). It's a nice vague number. In a single year, Europe generates about 4 gigatons. About half of the CO2 generated worldwide comes from stationary sources like power plants that could potentially be equipped with CCS.

The total cost for CCS depends on when it is built and the volumes and technological breakthroughs of the future. Experimental CCS plants will be able to sequester and store CO2 at a cost of $80 to $120 per ton (€60 to €9), according to a McKinsey report on CCS. That includes capture, transport and storage. Capture accounts for about two-thirds of the cost.

Early commercial-scale projects – those that might be built in the 2015 to 2025 time frame – might do the whole job for $67 to $47 per ton, which could drop to $40 to $60 per ton by 2030, which is comparable with expected carbon cap fees at the time. Thus, CCS could pay for itself. Further reductions of $7 to $10 per ton are possible at that time.

The least expensive storage would be in onshore, shallow and highly permeable reservoirs. Places with an existing infrastructure like Germany's Ruhr Valley are a key example. McKinsey, in fact, estimates that only around 3.5 gigatons a year could be abated through CCS. At $45 a ton, that's $157 billion of CCS a year.

The Business Case

The investments needed to make CCS become a commercially competitive alternative are obviously massive. But who's going to foot the bill? And why? Big oil companies are already familiar with much of the technology used for CCS. But the utility companies are also players in the game since they are choosing where to buy the power used in the grid. Until now the utility industry has been focused on reliability and low cost. But that might need to change if the initially much more expensive power from CCS power plants will get a chance to get on the grid.

[pagebreak:Carbon Capture Cont'd]

According to Sally Benson, Director of the Global Climate & Energy Project (GCEP) at Stanford, setting a price tag on carbon emissions will do the job. "If there were a price on CO2 today and it was known that it would increase over time, people would be much more aggressive to employ the new technology," she said.

For the utility companies it's going to be more costly and with lower reliability. On the other hand, oil companies, accustomed to high risk with high reward kind of projects, will need to shift to a business model with long-term utility systems. Policymakers need to really figure out how to stimulate this market since it's not reasonable to think that the oil companies or utilities will do it themselves. Expect high taxes on fossil fuels and CO2 pollution before any major changes are made.

Early Experiments

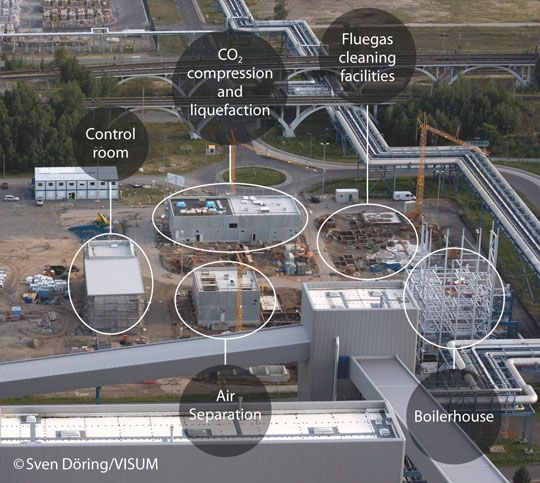

One of the most common arguments against CCS technologies is that there is a the lack of full scale testing and evaluation. There are pilot projects, like the Schwarze Pumpe, a 1,600-megawatt coal-fired power plant in Germany. It will capture up to 100,000 tons of CO2 and bury it under a nearby gas field, 3,000 meters below ground level. It's one of the first projects that actually puts the technology to use in a full-scale demonstration.

The Schwarze Pumpe

Source: Vattenfall

[pagebreak:Carbon Capture Cont'd]

But the question remains: How soon could we have the CCS methods implemented on a larger scale?

"It depends on the pace of investments. What's needed right now is to do some very large-scale integrated demonstration where you capture CO2, you generate electricity, you compress it and you transport it. You can show people that this is the way this technology looks when it's integrated together. You can get cost data. You can get reliability data. That's what is important," said the GCEP's Benson.

"We should be constructing these plants now and we shouldn't be talking about design. We can't wait. We've got to do this. This is the time," she said.

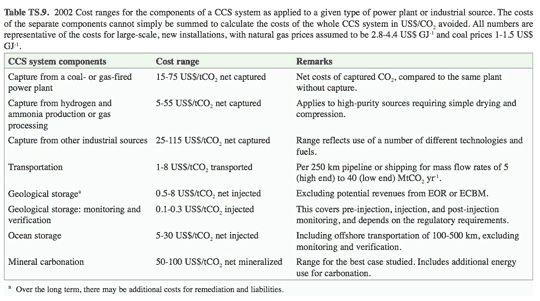

According to the IPCC, the cost ranges are spread out as such:

Cost Ranges for the Components of a CCS System

Source: IPCC

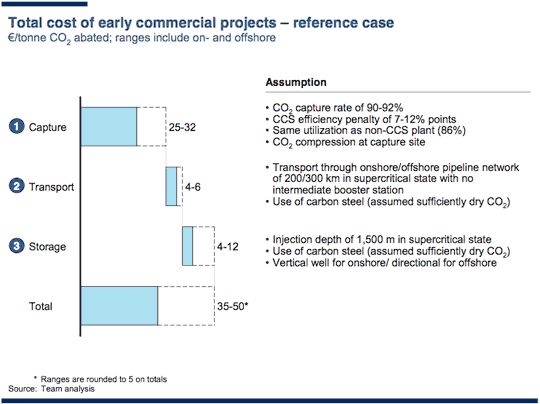

And here are the McKinsey calculations of a CCS reference case:

BP is injecting one million tons of CO2 into a reservoir located in In Salah, Algeria. The gas project will eventually store 17 million tons of CO2, which, says BP, is an emission reduction equivalent to removing four million cars from the road.

BP has also formed a $73 million joint venture with the Chinese Academy of Sciences that will aim to bring technology from Chinese labs to the market. Projects will likely include carbon capture and sequestration.

Other CCS Projects So Far

- Weyburn-Midal Project, Canada: Captures CO2 from coal gasification plant in North Dakota. It is used for enhanced oil recovery.

- The Snohvit: A Norwegian project that was one of the first in the world back in the 1990s.

- Alberta, Canada: Government officials have invested in CCS technology (Alberta Saline Aquifer Project (ASAP).

- Nirranda Underground Wells: Demonstration plant in Nirranda South in South Western Victoria, jointly funded by Australian government and companies.

Continue to Part III: New Ideas in Carbon Capture.

41

41

15

15

9

9