Independent power producers (IPPs) have, to date, largely relied on securing power purchase agreements (PPAs) with utilities for the price certainty needed to finance utility-scale solar projects.

Because the levelized cost of electricity (LCOE) of wind has recently been more competitive than that of solar, developers have had another path to price certainty, explained Lincoln Renewable Energy (LRE) COO and former Acciona (PINK:ACXIF) North America CEO Dan Foley.

LRE just announced the finalization of a twenty year PPA with Southern California Edison (NYSE:EIX) for the output of its adjacent twenty-megawatt Marathon and ten-megawatt Agincourt solar power plants, scheduled for 2013 construction in Southern California.

Foley said that soon, as the result of small marketplace changes, it could be possible to build utility-scale solar without a PPA.

“They always talk about plants being 'built merchant',” he said of some wind projects, “that they float with the market. Not all of them. Many projects were able to fix the price through derivatives. It looks merchant,” Foley said, “but it is a synthetic PPA.”

Power projects are required to report details of transactions through Federal Energy Regulatory Commission (FERC) Electronic Quarterly Reports (EQRs), Foley explained. “Wind projects may be labeled 'merchant' because there is no indication at FERC of a PPA,” he explained.

A synthetic PPA, Foley said, is the result of a long-term agreement with a power marketer. “The project sells its power into the market and receives the hourly clearing price, which floats every hour. This hourly clearing price is used as the index for a fixed-for-floating swap.”

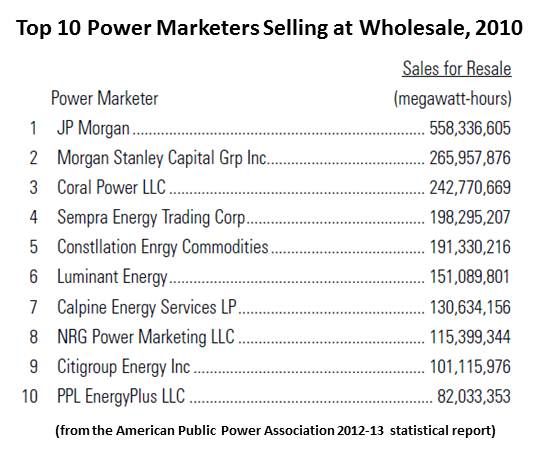

The top five power marketers, according to the American Public Power Association’s 2010 rankings, were JP Morgan (NYSE:JPM) (558-million-plus megawatt-hours), Morgan Stanley Capital Group (NYSE:MS) (almost 265 megawatt-hours), Coral Power LLC (242 million-plus), Sempra Energy Trading Corp. (NYSE:SRE) (198 million-plus), and Constellation Energy Commodities (NYSE:CEG) (191 million-plus).

Through the swap, which is made through a long-term contract, an IPP can secure price certainty, Foley said. “The project and the power marketer agree on the price. And every hour the contract is settled, based on the fixed price and the index, for the duration of the contract term -- as opposed to a PPA, where the contract is settled at a fixed price for every megawatt-hour the project produces.”

Foley offered a hypothetical example. Suppose the swap fixes the price at $52 per megawatt-hour for the electricity from a wind project.

The power marketer may also make a long-term deal with a power purchaser, known as a load-serving entity (LSE), at $58 per megawatt-hour. This would give the LSE long-term price stability without the risk of playing the commodity market.

If the hourly market clearing price is $40 per megawatt-hour, the market pays the wind project $40 per megawatt-hour and the power marketer pays the project $12 per megawatt-hour. The load pays the market $40 per megawatt-hour and pays the power marketer $18 per megawatt-hour. The power marketer makes $6 per megawatt-hour.

If the hourly market clearing price is $60 per megawatt-hour, the market pays the wind farm $60 per megawatt-hour and the wind farm pays the power marketer $8 per megawatt-hour. The load pays the market $60 per megawatt-hour and the power marketer pays the load $2 per megawatt-hour. The power marketer makes $6 per megawatt-hour.

“The actual spreads aren’t that wide,” Foley stipulated, “and the actual price depends on what the duration of the contract is: ten, fifteen, or twenty years. That price also depends on the location. Power in New Jersey is a lot more expensive than in Oklahoma. It’s really location-specific.”

This “merchant hedge gives the IPP the price certainty, which allows the project to support more leverage. With that leverage, the IPP can approach a tax equity player like for financing. The top ten providers of tax equity for U.S. renewables in 2010, according to a Mintz Levin white paper, were Bank of America (NYSE:BAC), Credit Suisse (NYSE:CS), MetLife (NYSE:MET), Wells Fargo (NYSE:WFC) and Citigroup (NYSE:C).

Though wind developers have been able to do this, Foley said, “solar is not there because the forward curve for the electricity commodity isn’t quite high enough to support PV solar.”

One of three things could happen, Foley said. “Natural gas prices could come up; solar installation costs could come down; or panel efficiency could increase. But if you look at the trends of those three, they are all trending in the right direction. It’s just not quite there.”

When power marketers provide a guaranteed price, Foley said, solar developers will have “a fixed cash flow” because “in solar, you generally know how many megawatt-hours you are going to generate every year. As a result, “I can tell you exactly what my cash flow is going to be and I can borrow up to some percentage of that.”

Based on his reading of utility-scale PV project installed costs, panel efficiencies and the trend in natural gas prices, Foley said he expects merchant hedges to be play a big role for developers when the investment tax credit expires in 2016.

But, he added, “I would expect that ERCOT [in Texas] and CAISO [in California] will be the only markets where the merchant hedges are viable due to their market construct.”

41

41

15

15

9

9