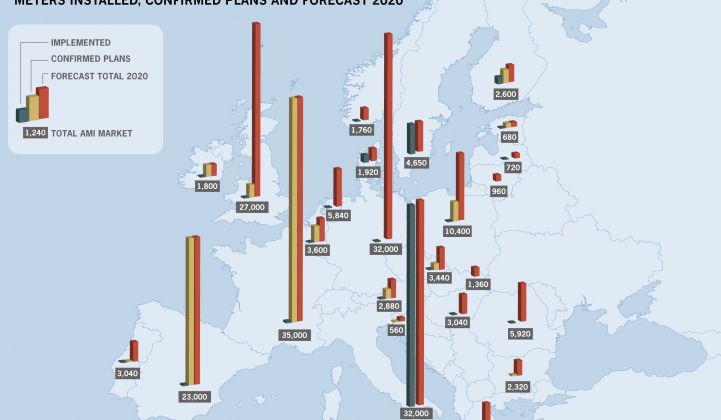

Europe is going to be the next big market for smart meters -- and Germany, the continent’s most populous nation, could be the biggest single customer in that market. But so far, Germany has lagged behind its Northern European and Scandinavian neighbors in deploying smart meters. It also hasn’t matched the big, national smart meter rollout plans of France, Spain and Italy, although it, like every other EU member, is required to have 80 percent of its meters made “smart” in one way or another by decade’s end.

What’s the holdup? Experts point to a lack of push from regulators, a lack of funding from the government, and a set of complications arising from Germany’s deregulated energy marketplace that have limited residential smart metering projects to a small number of pilot projects. At the same time, Germany has been taking its time to come up with a standard, interoperable set of technologies for every home and other small-scale utility customer in the country before it plunges ahead with millions of new meters.

U.S. smart meter giant Itron and Germany’s Deutsche Telekom announced a partnership last week, aimed at satisfying the long-term requirements of the still-evolving market. Under the terms of the deal, Itron has committed to buy and embed Deutsche Telekom’s SIM cards in its GPRS meters. That could allow Itron to deploy cellular-connected smart meters and other devices across Europe, much as Itron is doing in the United States via its acquisition of SmartSynch.

The two companies didn’t get into specifics on just how and where they’re working together, other than to say they will seek “opportunities in the area of smart energy (smart metering, smart grid, and smart home) in European markets,” backed by Deutsche Telekom’s communications network.

Itron recently reorganized its business to differentiate between the point-to-point, often cellular-based technology used for Europe’s commercial and industrial (C&I) market, and the larger-scale, mesh or powerline-carrier technologies being contemplated in Europe for home energy networks. Deutsche Telekom, for its part, already has a thriving utility and energy machine-to-machine (M2M) line of business, and is working with utility partners, much as Verizon, AT&T and Sprint are doing in the U.S..

“This means that they also have an end-to-end solution offering -- so at first glance, they are competitors,” Andre Wankelmuth, Itron’s director of marketing for metering and home area networks in Europe, said. But the two companies also see lots of room for cooperation, and are already working together in countries including the Czech Republic and Switzerland, he said. As for Germany, the two have their eye on projects there as well, Wankelmuth said, though he wouldn’t provide details.

Germany’s Regulatory and Business Challenge

It’s important to note that Germany has some smart meters already. German law has required smart meters for all new construction or major retrofits since 2010, and many large C&I utility customers have two-way communicating interval meters of various makes and models, just like in the U.S., Japan and the rest of Europe.

Indeed, Itron manages tens of thousands of such C&I smart meters from an operations center in northern Germany, said Jean-Paul Piques, senior marketing director for Itron in Europe. But that’s a small fraction of the potential multimillion endpoints that the country’s mass residential markets offer, he added.

Unlike the United States, however, which directed billions of dollars of stimulus grants toward smart meters, Germany’s government hasn’t offered any subsidies or incentives, as this 2011 report from Frost & Sullivan lays out. Indeed, Germany’s model as it stands makes it hard to pay for smart meters, because while the distribution grid operators are obliged to pay for them, they’re limited by regulations as to how much they can charge for them.

Also unlike the United States, German regulators have chosen to put standards before deployment, not after. Germany’s government and industry representatives have been working for years on the technical and regulatory framework for any mass-market deployment, with a focus on standards-based interoperability, as well as data privacy and security, Wankelmuth said. Until that framework is set, it’s hard for utilities or private investors to stake any claims.

Germany’s Open, Interoperable Home Energy Network?

Still, there are signs that Germany may be turning a corner. An October report from Berg Insight noted that government regulators, disappointed by the slow uptake of smart meter and home energy management offerings being put on the market by retail service providers, may be considering a “regulation-driven” nationwide rollout.

At the same time, Germany’s private-public technical working groups have settled on a set of standards for linking homes to utilities via a device once known as the multi-utility controller, or MUC, but now known as the “BSI gateway,” Wankelmuth said. The name comes from the Bundesamt für Sicherheit in der Informationstechnik (BSI), Germany’s information security office, which is overseeing privacy and security aspects of the plan.

In simple terms, the BSI gateway is a single point in the home or building that links water, gas and electric meters and other in-home devices to the utility’s backhaul networks. Right now, plans call for the BSI gateway to use wireline or wireless Modbus to talk to meters and in-home devices, and cellular or powerline carrier to connect to the utility, he said. That’s a bit different than the typical U.S. model, where smart meters are the endpoints themselves -- but it fits in with Europe’s desire to have low-power gas and water meters contained in the same network, he said.

Having the “smarts” reside in a box that stays with the home also helps in deregulated, competitive markets like Germany, the U.K. and other parts of Europe, where customers can theoretically switch their service provider, and thus their meter, every 30 days or so. At the same time, retail electricity and gas providers can use smart thermostats, in-home energy displays and other devices to attract and retain customers – if the underlying technology is in place to support them.

It’s also important to note that Itron’s big smart grid partner Cisco is also working in Germany’s smart metering market. In 2009, it joined German retail electricity provider Yello Strom in a residential smart meter-home energy management pilot, one of a handful of projects where third-party power providers have leaped ahead of the market at large to offer in-home energy technology. On the broader smart metering rollout front, Cisco is also working on a powerline carrier (PLC) technology known as G3-PLC, along with such industry players as Itron, Landis+Gyr, and a host of semiconductor companies, which Itron hopes to use in Europe.

41

41

15

15

9

9