A transformation in solar and wind financing that began with third-party ownership, crowd-funding, and community-owned projects is about to move renewables profits from Wall Street to Main Street.

“Solar- and wind-power developers generally raise money for new projects through private deals with banks, insurance companies or corporations,” the Wall Street Journal recently reported. “But they are eager to tap public markets, where the pool of investors would expand to include pension funds or individual investors.”

“Tax equity has long been and will continue to be the primary bottleneck to growth for U.S. solar,” explained GTM Research VP Shayle Kann. But new ways to fund solar and wind are in the works, Kann said.

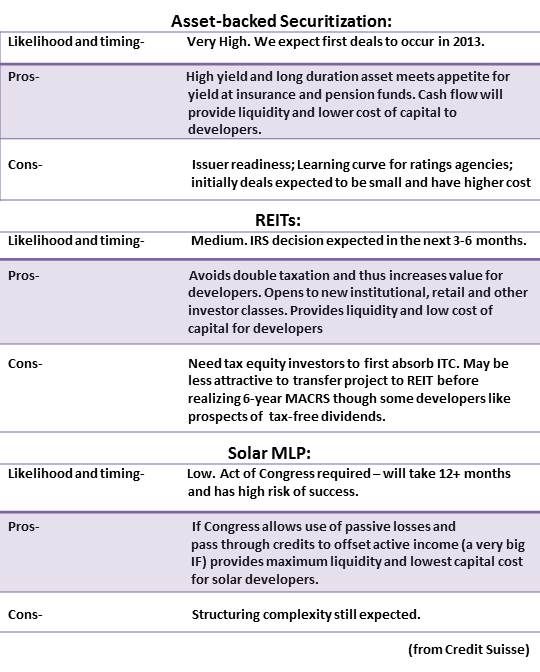

Solar securitization, which is “taking a portfolio of contracted revenue from solar projects, bundling it, and selling it as individual securities,” Kann said, is likely to happen in 2013. “The most likely first version would be bundling a bunch of residential solar leases and securitizing those leases either into one security or various tranches. Think of it like mortgage-backed securities.”

The same can be done with utility-scale power purchase agreements (PPAs). According to the technical definition of securitization, it has already been done, said Kann. Warren Buffett’s MidAmerican Energy sold bonds to help finance its purchase of the Topaz Solar Farm. “Those bonds,” Kann noted, “are securities, and tradable, and solar-backed.”

The other ways that market investors may soon be able to buy into wind and solar are through Real Estate Investment Trusts (REITs) and Master Limited Partnerships (MLPs). Both can be exchange-traded and shelter taxes.

A REIT “is a corporation, trust, or association that invests primarily in income-producing real estate assets,” Standard & Poor’s explained in its March 6 Sectors. REITs “are traded (both publicly and privately) in individual investment units.” An IRS ruling could make renewables projects one of the property types eligible.

In an MLP, “a general partner is responsible for running the partnership, while the individual investors are the limited partners,” Standard & Poor’s explained. “Natural resources, commodities, or real estate” are currently eligible -- but not renewable energy projects. Including them would require a congressional amendment to the MLP Act.

“We think these structures would drive growth by creating a larger investor pool, making solar more competitive with more traditional sources and ultimately providing a lower cost of capital,” Standard & Poor’s said. We think these structures are also the next logical transition to an unsubsidized solar market. We think potentially new emerging investment structures will benefit downstream providers the most and could provide a major catalyst for solar.”

Rumors have been circulating for a month that the Treasury Department is on the verge of issuing a ruling allowing renewables developers to use REITs. Hannon Armstrong Sustainable Infrastructure Capital has already obtained a private letter ruling that allows a renewable energy REIT, Credit Suisse reported in its 25 February Solar Snippet. And Renewable Energy Trust Capital (RET) recently requested one, according to Standard & Poor’s.

The questions about REITs, Kann said, are whether the IRS will issue a blanket ruling allowing REITs for all renewables projects and what the impact will be.

Senators Jerry Moran (R-KN) and Chris Coons (D-DE) introduced Senate legislation in June 2012 that would amend the MLP Act to allow renewables to use that vehicle, and Rep. Ted Poe (R-TX) introduced the same legislation in the House last September. There is bipartisan sponsorship from eleven senators (three Republicans) and three representatives (one Republican).

But, Credit Suisse noted, “we view MLP changes as more difficult than solar REITS, as MLP changes would require congressional legislation as opposed to IRS rule interpretations.”

“The timing of when these vehicles might be allowed into the industry remains an uncertainty,” Standard & Poor’s observed. “We think 2013 is a real possibility.”

Two recent uses of Main Street money, Credit Suisse pointed out, demonstrate how much such financing may lower the cost of capital.

Utility-scale solar rates of return may be as high as 15 percent to 20 percent. The MidAmerican Energy sale of $850 million in Topaz Solar Farm BBB-rated bonds, at a 3.8 percent interest, was oversubscribed.

Residential solar tax equity typically requires rates of return in the 8 percent to 12 percent range. However, startup Solar Mosaic recently offered a 4.5 percent return on crowd-funded project financing and sold out all but one project the first day.

“Both REITs and securitization would be big deals,” Kann said. “Either could go a long way to open up pools of new capital and lower the cost of capital.”

Below is an explanation of how Credit Suisse ranks the likelihood and impact of these various financing mechanisms:

41

41

15

15

9

9