U.S. solar PV system costs fell across all market segments from 2019 to 2020 as module prices continued to drive down system costs. While shortages of glass and ethylene-vinyl acetate laminate caused solar module prices to increase at the end of 2020, they still fell on an overall year-on-year basis.

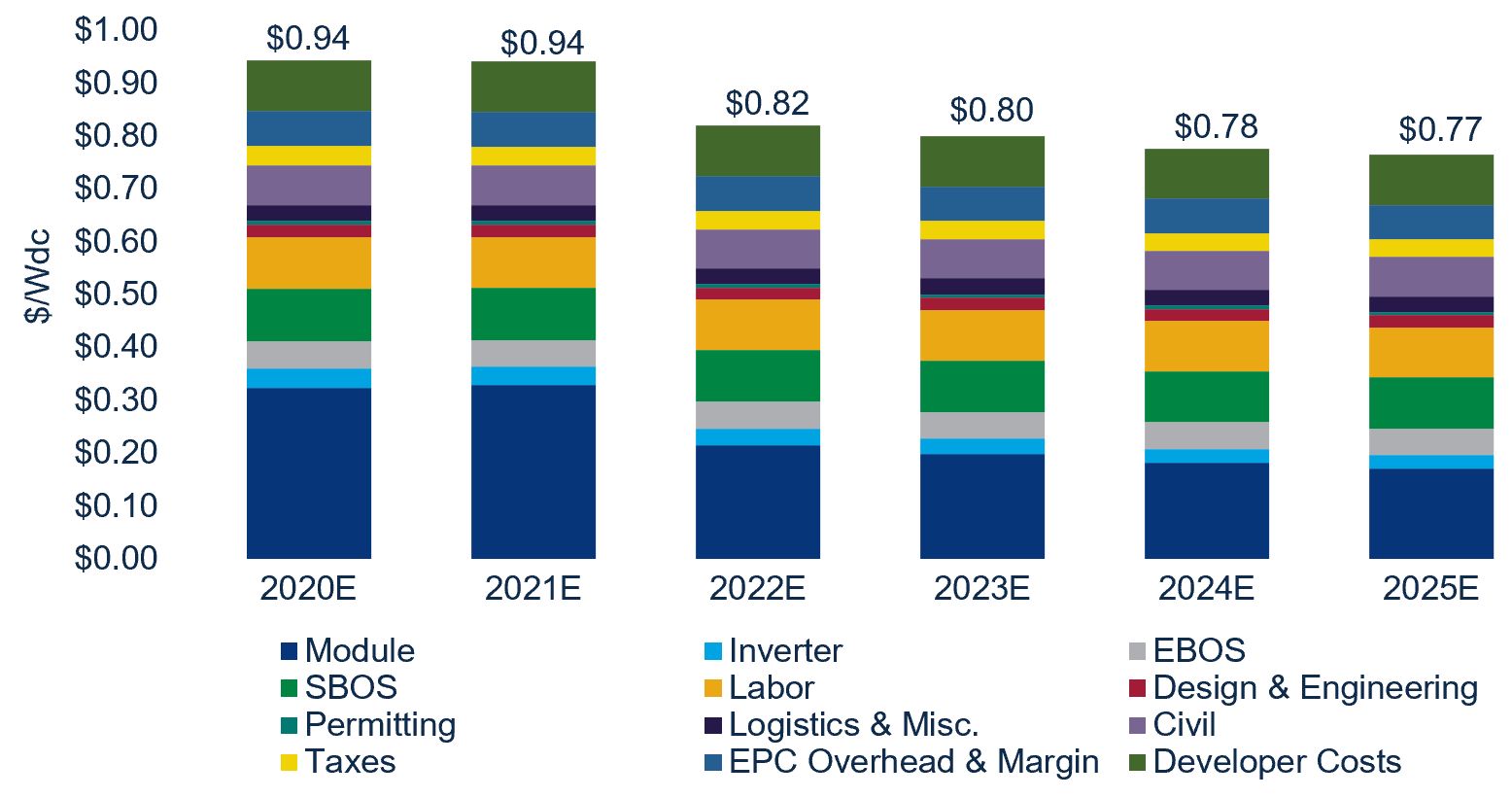

According to Wood Mackenzie’s recently released U.S. Solar PV System Price report, average 100-megawatt utility-scale system costs in 2020 are $0.94/W, with the potential to fall 19% by 2025 (all watt figures shown are DC). These costs will fall 13% from 2021 to 2022, driven by module price reduction as Section 201 tariffs are expected to phase out for imported products.

Average U.S. utility-scale 100 MW single-axis tracker all-in PV system costs with bifacial modules and 1,500-volt central inverter

Source: Wood Mackenzie’s U.S. Solar PV System Pricing: H2 2020

Note: This cost forecast does not assume a Section 201 extension or increase scenario.

Average commercial rooftop system costs in 2020 are $1.65/W and expected to fall 16% by 2025, according to Wood Mackenzie, assuming a 500-kilowatt flat roof system with string inverters and monofacial, monocrystalline passivated emitter and rear contact (PERC) solar modules. In the residential segment, average system prices are $3.10/W in 2020, based on the assumed use of microinverters and monofacial, monocrystalline PERC solar modules.

System costs can vary by as much as 40% to 50% between states within each market segment, driven by labor-cost differences, interconnection costs, permitting processes and other factors.

Tariffs on imported products continue to impact system costs. Section 201 tariffs for bifacial solar cell and module imports into the U.S. have been reinstated as of November 2020. The prices of bifacial monocrystalline PERC solar modules imported from Southeast Asia to the U.S. were lower than monofacial, monocrystalline PERC prices in 2020, while bifacial modules were exempt from these tariffs. However, without the bifacial exemption, these module prices are about 8% higher than monofacial, monocrystalline PERC prices.

Some inverter prices increased in 2020 as a result of residual Section 301 tariff impacts. These tariffs affect all inverters imported from China to the US, and the rate was increased from 10% to 25% in 2019. While this primarily caused inverter price hikes in 2019, there were more increases in prices in the residential segment in 2020. Single-phase string inverter and microinverter prices saw further increases in 2020, which kept average residential system prices from falling as quickly as they otherwise might have.

With the current surge in COVID-19 cases in the U.S., all market segments are likely to be able to handle the ramifications more effectively than when the pandemic first hit the country in early 2020. Of course, this assumes solar PV construction will be allowed to continue despite any new shelter-in-place orders that may be imposed. In the residential segment, which has shorter project cycles compared to the commercial and utility-scale segments, virtual customer acquisition and permitting processes are more established and streamlined now.

Further impacts from COVID-19, as well as the fate of the federal Investment Tax Credit, will determine how much lower customer-acquisition costs can go for residential solar, but there is potential for these costs to decline more rapidly than originally forecast, especially for companies that have had more expensive processes in place.

As of now, these costs make up roughly one-quarter of total residential system costs, but if any efficiencies learned in 2020 prove to be profitable, there is potential for these costs to represent a smaller portion of overall system costs. Soft-cost reduction continues to be a leading priority for companies operating in all market segments, and a reduction in customer-acquisition costs could yield more competitive system prices.

Project capacities climb and larger-format modules gain traction

Project capacities are increasing, particularly for large-scale ground-mount facilities in the utility-scale space. With larger projects come economies of scale benefits. The average cost of a 100 MW single-axis tracker system in the U.S. was as much as 8% less than that of a 10 MW system in 2020.

However, procurement strategies and soft-cost optimization will determine just how much costs can be reduced on a dollar-per-installed-watt basis with more megawatts installed. Hardware costs can only go so low. Reductions in costs such as project management, due diligence and labor can yield more cost-per-watt benefits.

Solar module power classes will continue to increase, especially as larger-format wafers come onto the scene. These modules will be physically larger and heavier but with higher power ratings. As a result, developers and engineering, procurement and construction providers are analyzing their cost stacks to understand the full savings potential and determine how labor costs might be impacted.

***

Learn more about the Wood Mackenzie U.S. PV pricing report.

Molly Cox is a solar analyst with Wood Mackenzie.

41

41

15

15

9

9