Seeking to leverage their respective advantages in the PV sector, Yingli Green Energy (YGE) and GCL-Poly (3800:HK) have entered into a strategic cooperation framework agreement. According to announcements this morning, the companies will endeavor to fully cooperate with each other along the PV supply chain, including research and development, product manufacturing, and project development.

So what does this mean? Yingli will now have access to low-cost wafers, as well as a captive pipeline for its modules. GCL gains a dedicated polysilicon and wafer customer and low-cost modules for its development activities. Additionally, should the Chinese government impose tariffs on imported polysilicon, Yingli would be able to avoid the duties.

Source: GTM Research Competitive Intelligence Tracker

While this strategic agreement is certainly exciting news, this is not the first time we've seen GCL cooperating further down value chain. In 2011, the company announced a joint venture with Canadian Solar for the development of a 600-megawatt wafer plant in Suzhou dedicated to Canadian's requirements. The JV strategically expanded capacity for both firms; however, unlike the agreement with Yingli, it it focused solely on wafers. There is no evidence to suggest that GCL uses Canadian modules in any of its development activities.

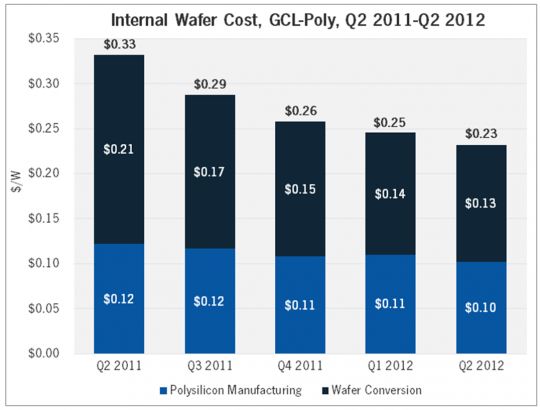

Today's announcement represents a win-win situation and is an example of informal consolidation in the Chinese market. Yingli needs low-cost silicon materials and a captive pipeline for its modules -- GCL's cost structure is industry-leading (average cost in 2012 stood at $19.70 per kilogram for polysilicon and $0.25 per watt for wafers), and as of December 31, the company had 327 megawatts of projects ready to commence construction, 1,000 megawatts in the planning stages, and 1 gigawatt under agreement with China Merchants New Energy. GCL needs a cell and module partner; Yingli was the world's number-one PV module supplier last year. Both have intellectual property in their respective value chain segments that could benefit the other.

Source: GTM Research Competitive Intelligence Tracker

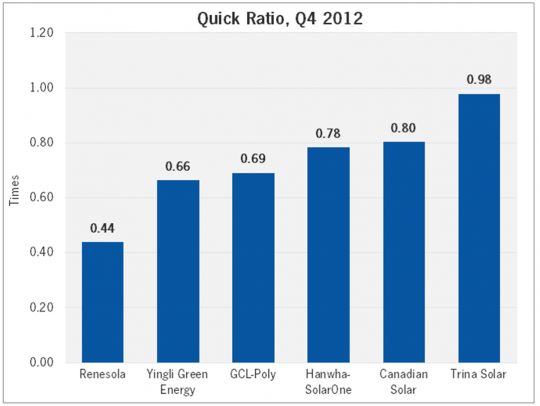

As oversupply continues to squeeze the global PV market, neither company wishes to lay out the capital for acquisition activities. Most publicly traded companies are dealing with depleted balance sheets and don't have the cash for such transactions, as indicated by the chart above. ("Quick ratio" measures a company's ability to meet its short-term obligations with its most liquid assets. The higher the quick ratio, the better the position of the company.) Therefore such a partnership is the next-best, or even the more ideal, option. While the agreement is non-binding, and therefore has no legal teeth, it could indicate a move toward future consolidation within the Chinese market. Specifically, it would not be surprising to see Yingli and GCL assimilating into a single entity further down the line.

Follow the implications of the GCL-Yingli partnership going forward with a subscription to GTM Research’s Global PV Competitive Intelligence Tracker.

41

41

15

15

9

9