Despite slightly negative market growth for a second straight year, on-site commercial solar remains a compelling opportunity for many large energy consumers looking to drive energy savings and meet sustainability targets.

In a new briefing for GTM’s Grid Edge Customer Network members, we detailed the corporate solar landscape and provided some highlights ahead.

At a high level, there are a number of ways to do business.

To the prospective customer with available capital and tax appetite to absorb tax credits and accelerated depreciation, a cash purchase can be the fastest and most streamlined approach to acquiring on-site solar with minimal expense and interest rates. Though such a direct ownership approach doesn’t require the host organization to have a high credit rating or to enter into a long-duration commitment of 15 to 20 years, it does generate additional ownership responsibilities, including operation and maintenance costs.

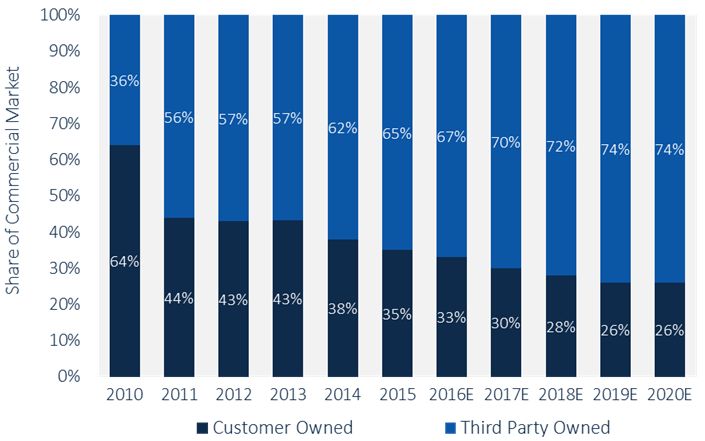

While some companies have gone solar by leveraging company cash or debt, 65 percent of 2015 commercial installations were executed through third-party financing and ownership structures -- a trend that is expected to increase moving forward.

FIGURE 1: Commercial PV Installations by Ownership Structure

Source: GTM Research's U.S. Commercial Solar Development Landscape, 2016-2020

Signing a third-party power-purchase agreement (PPA) provides fixed energy rates without requiring an initial capital investment and allows the customer to avoid taking on the responsibility of system O&M. To those with no or low income tax, a PPA can directly translate into a positive revenue stream and hedge against future electricity-price volatility.

Similar to PPAs, a solar lease also requires a long-duration contract and a comprehensive credit review. However, rather than paying for the energy generated by the solar system, a lease allows the host customer to use the equipment in exchange for recurring payments. Upon termination of the lease, customers are generally able to buy system at reduced cost, renew the lease under new terms, or end the contract and remove the system.

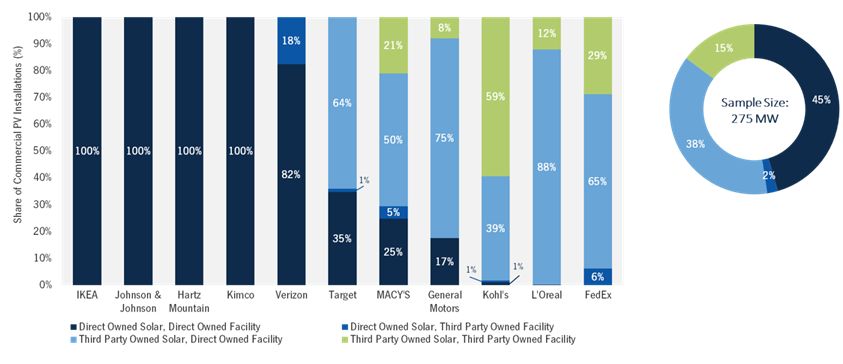

Unsurprisingly, when we examine historical solar adoption data collected by the Solar Energy Industries Association (SEIA), we find that large corporations tend to favor either direct or third-party ownership models, with few pursuing a combination of both.

FIGURE 2: Cross-Correlation of Solar and Facility Ownership of Select Corporations

Source: SEIA Solar Means Business, GTM Research Grid Edge Customer Network Briefing

The select sample size above represents just a small portion of commercial solar adoption. It further confirms the preference for third-party ownership models (in this example, TPO accounts for 53 percent of the 275-megawatt sample size).

Companies that own their facilities like Ikea, Johnson & Johnson and Hartz Mountain most often choose to self-finance and directly own on-site solar. However, directly owned solar systems only account for 2 percent of the sample set’s capacity.

Ikea, a privately held multinational that has deployed a total of 41 megawatts of solar across 90 percent of its U.S. facilities across 20 states, continues to pursue a direct-ownership approach to on-site solar procurement, largely based on three characteristics:

- Ikea operates under longer planning horizons, as it generally builds its own facilities, purchases associated land and establishes long-term relationships with suppliers.

- The company often leverages its large balance sheet to lower self-financing cost of capital.

- Cutting out middlemen allows Ikea to capture all financial and environmental benefits.

Even though commercial solar turnkey development has seen average cost reductions of over 60 percent in the past five years, challenges continue to overshadow adoption drivers. Unlike the more familiar cookie-cutter residential market that uses easy-to-access FICO scores to assess creditworthiness, commercial and industrial developers and financiers often find that the heterogeneous nature of large energy consumers, coupled with a general lack of standardization and evaluation metrics, requires a much more flexible approach.

Furthermore, compared to the residential market where funds are generally closed in large tranches of similar deals, commercial financiers face larger transaction costs and lower potential liquidity, resulting in higher costs of capital. Business models must accommodate these additional costs and uncertainties, which is often detrimental to smaller-scale project economics (<1 megawatt); project stakeholders frequently end up at the negotiating table, ultimately agreeing to terms on a case-by-case basis.

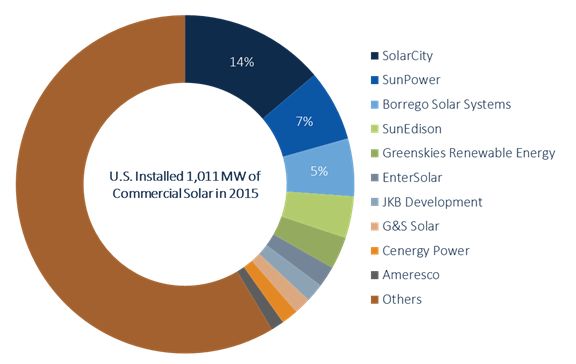

This has resulted in a fragmented developer landscape, with few national players and many local installers operating within each state. Over the 2015 timeframe, SolarCity led all installers with 14 percent of installations, followed by SunPower and Borrego Solar.

FIGURE 3: Top 10 Commercial Installers, 2015

Source: GTM Research U.S. PV Leaderboard Q1 2016

Looking forward, the recently announced federal solar Investment Tax Credit extension is expected to help revive market growth in annual commercial solar installations by 294 percent in 2020 over 2015 figures.

Created to help large consumers navigate the energy management and procurement landscape, GTM's Grid Edge Customer Network streamlines the decision-making process by providing actionable analysis and insights into the latest technology, regulatory changes and market developments.

***

Omar Saadeh is a senior analyst with GTM Research and the lead author of the Grid Edge Customer Network executive briefings. Grid Edge Customer Network members include end-use customers who are charged with making enterprise-wide energy decisions. They gain access to exclusive research, events and data services. Learn more here.

41

41

15

15

9

9