In the last few years, subsidized solar markets like those of Germany, Spain, and Italy have created waves of investment and development binges -- along with mixed results. Germany status as a savior market has been sustained for years now, while Spain's ill-conceived feed-in tariff structure resulted in one big year followed by an extremely painful hangover.

Solar project developers like Phoenix Solar and module manufacturers such as First Solar have, reasonably, exploited these savior markets for every subsidy euro or dollar that could be extracted. New markets in 2010 and 2011 have included the U.S. and its thriving utility-scale sector. The domestic China market in 2012 holds the promise of anywhere from three to eight gigawatts of demand -- at least for Chinese suppliers.

But firms that live by the subsidy will perish by the subsidy as well. As the German feed-in tariff has ratcheted down, there has been a streak of bankruptcies for German solar manufacturers.

Go South -- and West -- and someplace sunny

A common theme echoed by these now-humbled solar players is to "wean themselves off" of the tariff structure -- in the words of Dr. Murray Cameron, the CEO of Phoenix Solar and Member of the EPIA Board. First Solar has unveiled a five-year plan focused on emerging markets in the Sun Belt with a goal to ship 2.6 to 3.0 gigawatts at system prices, enabling a levelized cost of energy (LCOE) of $0.10 to $0.14 per kilowatt-hour.

Cameron said that the "good old days of feed-in tariffs" are ending and the industry needs to "get away from the gluttony" of subsidies and "actually sell solar to more complex and demanding markets."

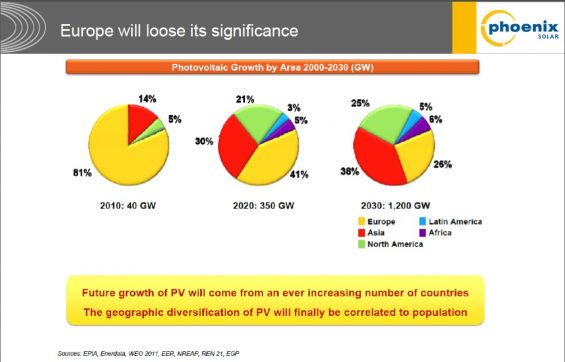

"There's business to be done in emerging markets," according to Cameron, but there's going to be "pain because we haven't prepared ourselves for the transition to new markets and low prices." He said that it was "remarkable that Europe will lose its significance, but there is still good news: there are ten one-gigawatt markets."

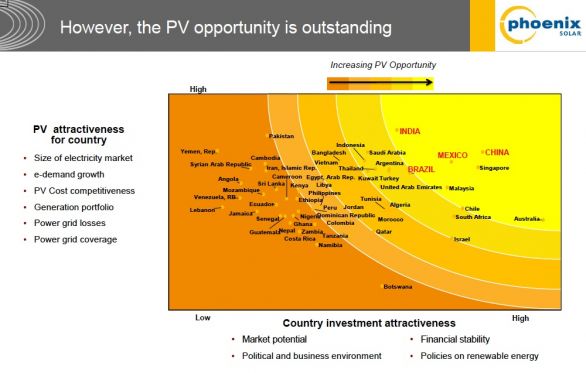

Both First Solar and the EPIA have come up with charts and filters that point solar in the same direction -- towards India, Saudi Arabia, Brazil, Mexico, China, and in First Solar's case -- the country of Texas.

The EPIA looked at the 140 countries in the Sun Belt and selected 66 with the greatest potential, and then rated them by size of the electricity market and growth rate, the cost competitiveness of PV, generation portfolio, and power grid coverage.

_584_328_80.jpg)

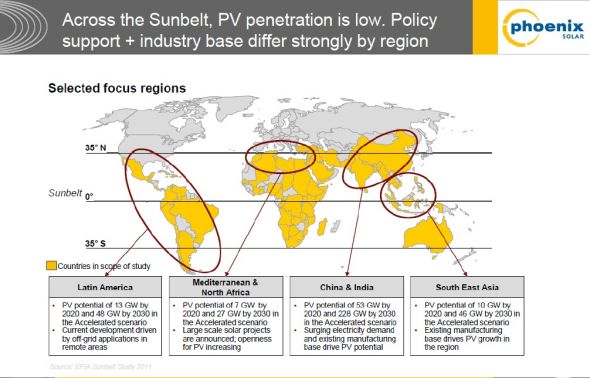

Cameron suggested that in many of the emerging regions, "The markets will work differently. First will come large-scale and then rooftops." Larger systems are going in first because of the grid. In India, the "low-voltage grid is in a sad state, the medium-voltage grid is shaky, but there's plenty of stability in the high-voltage grid."

The winners, according to Cameron, will be China, Mexico, Brazil, India, and Singapore.

There are also opportunities for 500 megawatts of PV in Thailand by 2022 and 1.25 gigawatts in Malaysia, which "feels it has to diversify despite low-cost electricity and gas reserves." Cameron saw 20 gigawatts of potential in India for PV and CSP but would have to cope with peak demand at night.

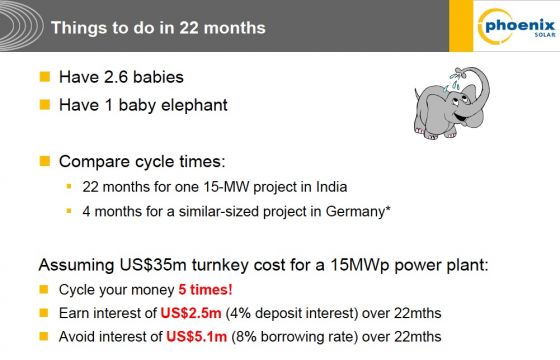

Cameron notes that a 15-megawatt project in Germany can be completed in four months versus the 22 months that it might take for commissioning in India. That's roughly the same time it takes to gestate an elephant.

41

41

15

15

9

9