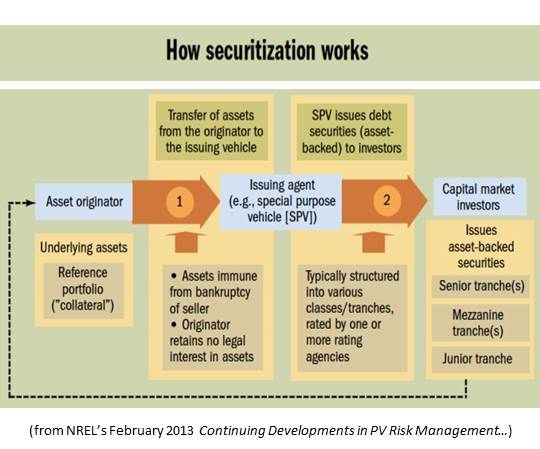

“Securitization,” explained GTM Research VP Shayle Kann, “is taking a portfolio of contracted revenue from solar projects, bundling it, and selling it as individual securities.” It could be the answer to the increasing shortage of tax equity funding for solar which, Kann said, “will continue to be the primary bottleneck to growth for U.S. solar.”

No rooftop solar-asset backed securities have yet been issued. But “multiple residential and commercial solar developers such as Sunrun, SunPower (NASDAQ:SPWR) and SolarCity (NASDAQ:SCTY) are likely working on issuing asset-backed securities over the next three to nine months,” Credit Suisse reported in its February 25 Solar Snippet. Other third-party leasing companies like Clean Power Finance and Vivint, the report added, are also showing strong enough growth to participate.

“We believe that solar securitization for residential solar projects will happen in 2013,” Credit Suisse (NYSE:CS) predicted. Early investors will be insurance companies looking for secure long-term investments.

The U.S. Department of Energy (DOE) formed the Solar Access to Public Capital (SAPC) working group through the National Renewable Energy Laboratory (NREL) to facilitate securitization of solar by standardizing the power purchase agreements (PPAs), leases, and other instruments on which they are based and to improve clarity on risk. There will be a free webinar on the group’s progress March 22 at 10 a.m. (MST).

Will institutional investors' move into securities backed by solar assets turn out better than the mortgage-backed securities implosion that led to the global financial crisis?

“The U.S. solar power industry continues to expand,” observed Standard & Poor (NYSE:MHP) in the report "Will Securitization Help Fuel the U.S. Solar Power Industry?" The report continued, “Securitization -- a financing technique that aggregates pools of assets, financial contracts, or loans, and through a structuring process transforms their future cash flows into a security -- may be a viable option for developers that wish to monetize cash flows from future lease or power purchase agreement payments. Such transactions could provide the issuers' parents with a significant amount of upfront cash for capital spending or other business ventures.”

For solar’s venture into asset-backed securities to work out, purchasers much be able to accurately assess their value. “It is the responsibility of the ratings agencies to rate these things appropriately,” Kann said. “The tricky part is to quantify the risks.”

The questions are, Kann added, whether ratings agencies rate solar asset-backed securities high enough -- and whether there will be buyers.

The first issues, Credit Suisse said, will be in the $50 million range. Later, investments in the $150 million range will increase liquidity and provide returns in the 5 percent to 6 percent range. “We believe that rating agencies and insurance companies are receptive to solar securitization, and we anticipate investment grade ratings on solar project securities,” according to the report.

Standard & Poor's report detailed three categories of risk: (1) limited performance data, (2) a lack of large-scale services, and (3) declining panel prices.

Data on rooftop solar at “a significant scale” only covers perhaps five years, S&P noted, while the PPAs and leases on which the securities will be based run up to twenty years. “We believe that reliance on short-term data may not accurately reflect how an offtaker will behave over an extended period of time.”

“You have the risk that the homeowner defaults on the contract,” Kann observed. “You have the technical risk that the system underperforms. And there is a risk that the lease provider goes out of business and can no longer provide the operations and maintenance on the system.”

Without proper maintenance, the return on the system would be reduced and the system owner’s commitment to it would be compromised.

“SolarCity recently put a backup service agreement in place,” Kann said. "If the company can no longer service its agreements, there is a well-rated, larger company that will take over. The point is to convince financiers and ratings agencies the assets are less risky.”

At least some of the companies that write the initial leases and PPAs, he added, maintain equity in them and therefore have an interest in seeing that the offtakers meet their obligations. Doing that maintains the value of the securities.

Further uncertainties come from panel price volatility, electricity market fluctuations and the difficulties of designing a financial product to cover systems that vary in productivity depending on solar irradiance and local regulation.

Nevertheless, S&P’s report concluded, “securitization of solar systems could be a feasible financing tool for developers who wish to monetize future cash flows.” It will cut developers’ financing cost because “the creditworthiness of the transaction is dependent upon the collateral pool and not the credit quality of the issuer, which in most cases is in the speculative-grade category.”

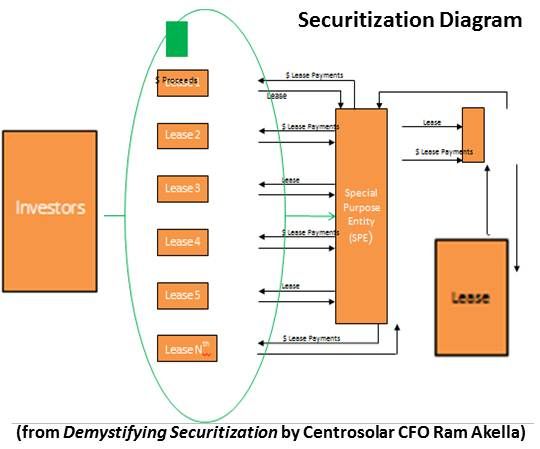

The housing market disaster was the result of over-borrowing, inflated valuations and over-leveraging, Centrosolar (PINK:CEOLF) America Managing Director Ram Akella recently opined to GTM. Many asset classes have been securitized, but “mortgages are the only place where things went sideways.” If the solar industry remains disciplined about issuing high quality securities, he insisted, “this further financial innovation will help make solar technologies even more affordable for an average consumer because it will bring in investors who don’t have the wherewithal to look at solar directly but know securitized products.”

***

Sources for this piece had observations about Real Estate Investment Trusts (REITs) and Master Limited Partnerships (MLPs), the other most frequently discussed alternative investment vehicles for solar. They will be reported in the next installment.

41

41

15

15

9

9