I wrote a less than enthusiastic article about the sale of Oerlikon's solar unit to TEL last week.

Amorphous silicon (a-Si) technology has had a troubled commercial track record.

There was the the faceplant of Silicon Valley semiconductor giant, Applied Materials, its customers, and its a-Si photovoltaic efforts. Recently, Novasolar, the reincarnation of Optisolar, furloughed its employees, and ECD, with one of the longest money-losing streaks of any corporate entity, declared bankruptcy. Both of those firms were multi-junction a-Si PV producers.

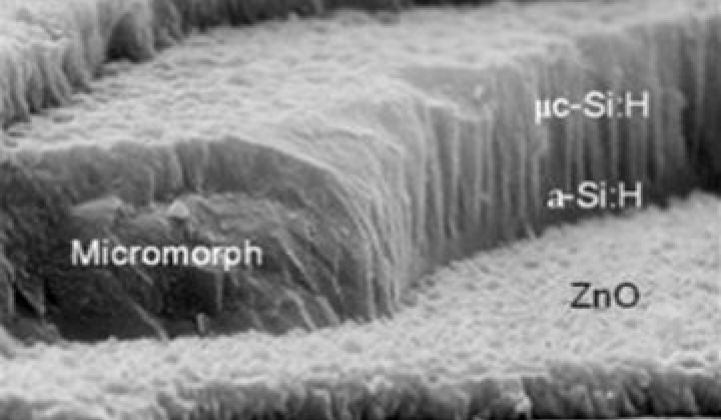

We have been less dismissive concerning equipment vendor Oerlikon's efforts in a-Si because in our many conversations with Chris O’Brien, Oerlikon Solar’s head of market development in North America, he confidently stated that the firm's aggressive cost targets were in reach. He cited first-mover advantages, having a longer legacy in micromorph (tandem-junction) designs, and starting off with an efficiency advantage. He also cited some technical advantages compared to other a-Si vendors and his belief that costs of 70 cents per watt would be achievable by 2011.

I hereby take back those harsh words about Oerlikon's amorphous silicon, because judging by the magnitude of this deal, which was just revealed, amorphous silicon might have some legs. The price for the deal was $275 million. And it would seem that those cost targets have been reached.

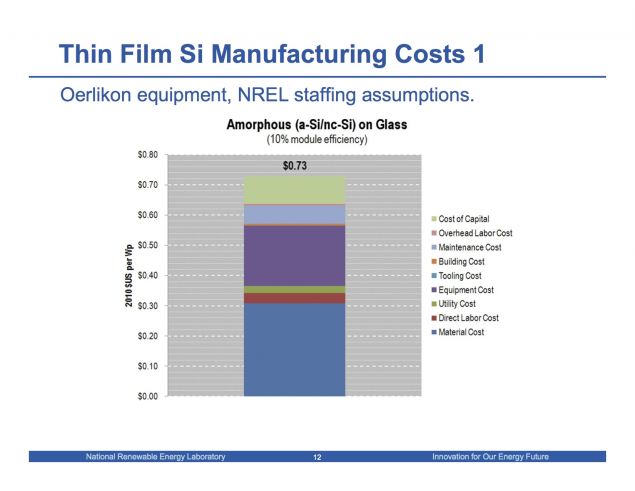

O'Brien furnished a slide from a 2011 analysis by NREL of Oerlikon Solar's previous generation fab which estimated cost of ownership for that technology to be less than $0.70 per watt (excluding the cost of financing). Newer generation technology brings the cost of ownership to $0.50 per watt according to O'Brien.

O'Brien also notes that "While the company did report a small EBIT loss [for 2011], the magnitude is significantly lower than the recent results announced by other leading PV companies."

Oerlikon Solar, based in Zurich, Switzerland, is controlled by Russian tycoon Viktor Vekselberg.

Some of Oerlikon's customers include Tianwei and Astronergy. Those customers are now the charge of Tokyo Electron (TEL). Dr Michael Buscher, CEO of Oerlikon Group, was quoted in a press release as saying, "TEL is an ideal strategic buyer for our solar business. Its main operations are close to the predominantly Asian customer base and having had a partnership with them for three years, they know our Solar Segment well." TEL has been a sales representative for Oerlikon in Asia for the past three years and has more than 10,000 employees in a variety of semiconductor businesses.

Other amorphous silicon players include Sharp, which entered a JV with Enel and ST Microelectronics in a-Si a few years ago. Also struggling to remain competitive in amorphous silicon and its variations are Xunlight, AOS Solar, APSTL, HelioSphera, NanoPV, and Sencera.

All of this action takes place against the backdrop of thin film leader First Solar, with 2 gigawatts of 12 percent efficiency solar module capacity at a cost of less than 75 cents per watt.

One company with big aspirations that might have a shot in a-Si is Astronergy, with the backing of the Chint Group, one of the largest Chinese private businesses. GTM Research finds that "Chinese tandem junction a-Si customers of Oerlikon at scale" can be "very competitive with c-Si, especially in hot regions like the U.S. Southwest, India and SE Asia, where there is better kWh/kW performance." Astronergy has landed a 6.1-megawatt a-Si project in Tucson, Arizona.

41

41

15

15

9

9