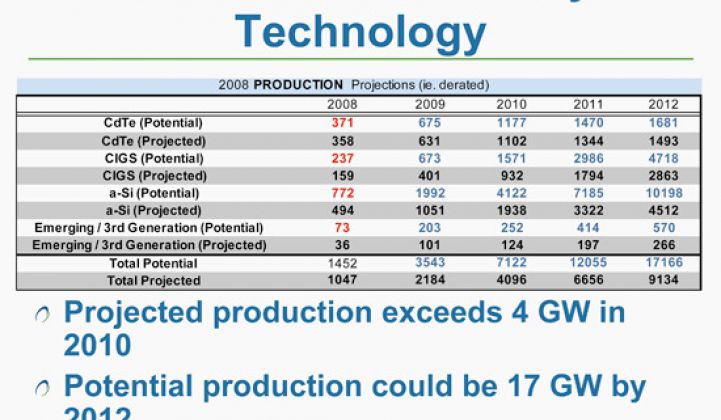

At a Greentech Media conference Wednesday, Travis Bradford, president of the Prometheus Institute, forecasted that thin-film solar production will grow from 1 gigawatt this year to more than 9 gigawatts in 2012.

“We project increased penetration of all technologies – cadmium telluride, copper indium gallium diselenide and amorphous silicon – above even our aggressive forecasts in 2007,” said Bradford.

Cadmium-telluride films, led by First Solar (NSDQ: FSLR), make up the largest portion of the thin-film market, he said, adding that he expects the company’s costs to drop from less than $1.25 per watt to less than $1 per watt by 2009.

However, those costs could be subject to the price of glass, which in turn depends on energy prices, he said. The cost of telluride, which is a mining byproduct of zinc, also has increased, he said.

“Cadmium telluride is the current leader,” he said. “There are some difficulties. But First Solar will continue to do well.”

According to Bradford, the big story of next year is likely to be copper-indium-gallium-diselenide – also known as CIGS – technologies.

Even though none of these companies have yet produced CIGS films in significant volumes, he said the technologies have potential.

“Many of these [technologies] are ready to go,” he said. “In some cases, it takes as much of a third of the capital less than First Solar to build a plant. … We think CIGS will be the big story on 2009 because we know how many companies are putting in multi megawatts of CIGS in 2009. We are convinced. Just like polysilicon was the big story of 2007 and First Solar is the big story of 2008, we believe in 2009 the big story will really be CIGS.”

Global Solar,Nanosolar, HelioVolt Corp. and Miasolé all have announced plans to expand production of CIGS in the last few months.

Meanwhile, Prometheus, which is a Greentech Media partner, expects amorphous-silicon films – such as those made by Applied Materials and Oerlikon – to stumble slightly in 2008 and 2009, as technologies get debugged and verified, before taking off in 2010, he said.

By 2012, the institute forecasts that amorphous silicon will make up the largest chunk of the thin-film pie with 4.5 gigawatts of production, with CIGS coming in second at more than 2.6 gigawatts.

The institute also named what it expects will be the top thin-film producers in 2012, starting with First Solar, Miasolé and Sharp.

“There are so many technologies, even if we’re wrong in one bucket, in one technology, there are a lot of different ways to hit 4 gigawatts in 2010 and our projections in 2012,” Bradford said.

41

41

15

15

9

9