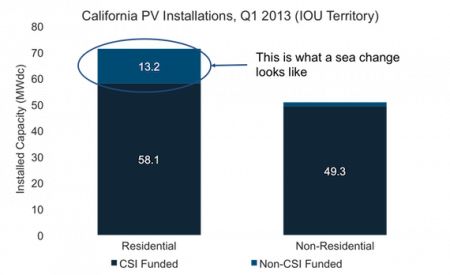

In the first quarter of this year there were 71.3 megawatts of residential solar installed in California’s three investor-owned utility territories, according to our just-released U.S. Solar Market Insight report. Of that total, 13.2 megawatts (18.5 percent) were installed without the support of rebates from the California Solar Initiative (CSI) or any other state-level program.

FIGURE: California PV Installations, Q1 2013 (IOU Territory)

Source: U.S. Solar Market Insight

It would be hard to overstate the significance of this, so I’ll reiterate. In the first three months of this year, around 3,000 residential solar installations were completed in California with no state incentives. These installations did benefit from a number of things: full retail net metering (we’ll come back to this), the federal Investment Tax Credit and accelerated depreciation, and California’s relatively solar-friendly rate structures. But even so, this is emblematic of a sea change in the solar industry and, even more importantly, the energy industry.

Historically, residential solar markets in the U.S. were exclusively driven, and constrained, by state- and utility-level incentives, often in rebate form. When a sufficiently large rebate was introduced, the market reacted, but once rebate funding was depleted, the market disappeared. This served as a de facto cap on residential solar growth, and it is why the California statistic is so significant. If state-level incentives are no longer required, there are 3.5 years of runway before the ITC expires for the market to adapt, expand and mature. Assuming nothing else serves as a major barrier -- and this is a big "if" given net metering battles and the ever-increasing need for project finance -- the sky is the limit.

This trend will only accelerate over the coming years. Residential PV system prices continue to fall. Average system prices reached $4.93/W in Q1 2013 nationally, with some states well below $4.00/W on average. Although this is a far cry from the $6.95/W average cost in Q1 2010, there is plenty of headroom remaining. Even assuming flat prices for modules (which, to be clear, we do not expect), there is around $0.50/W to be saved in customer acquisition costs alone, not to mention all the other “soft costs” in a system. We feel confident in stating that, at least through 2016, prices will continue to fall, and system economics will continue to improve.

Utilities are not blind to this transformation, but their responses vary. Some are working to replace retail net metering with a value of solar tariff, which they argue would more appropriately compensate solar customers for their distributed energy production (this question is the subject of much intense debate that I’ll leave for a later article). Notable examples here would be the California IOUs, APS in Arizona, and CPS Energy in Texas, to differing degrees. Others are steering into the skid and seeking to profit directly by selling, installing and owning their own distributed solar assets. For examples, see Duke Energy, PSE&G, and (perhaps surprisingly) Southern Company.

FIGURE: Utility Distributed Solar Investments to Date

Source: GTM Research

This is no small issue for utilities. There is an increasing body of research and discourse suggesting that distributed energy (including not just solar but also things like combined heat & power, small-scale energy storage, demand response and load management) could be an existential threat to the traditional utility business model. The reasoning is essentially this: how can a utility make a profit if forced to maintain its infrastructure and reliability while bleeding customers?

This leads us to the risks: what could stop the residential solar train in its tracks? First and foremost, net metering. There are a wide variety of potential outcomes for the net metering debates in California and elsewhere, and a number of them could cripple near-term growth. Second, rate design. We at GTM Research have been on a tear recently harping on the importance of rate design in the economics of distributed solar. Solar-unfriendly rates can be just as harmful as net metering caps. Third, the ITC, which is currently in place until 2016, but could at any time be revised or removed by Congress, assuming an omnibus tax bill breaks through congressional gridlock. (Think of that old McDonald’s commercial: “Hey, it could happen.”) Finally, project finance. We estimate that the U.S. residential and commercial solar markets will require roughly $54 billion in project finance between 2013 and 2017. That’s a big number for a market valued at $7.3 billion in 2012.

This is all just to say two things. First, we are on the cusp of an unprecedented shift in the U.S. solar market, and by extension the entire electricity market. Second, there is no guarantee as to which way we head from here. Just be careful not to blink, or you’ll miss it.

Shayle Kann is the Vice President of Research at Greentech Media, where he leads the GTM Research analyst team. For more information on the U.S. Solar Market Insight report, visit http://www.greentechmedia.com/research/ussmi.

41

41

15

15

9

9