Editor's note: Executives from Suntech, Q Cells, Canadian Solar, Yingli Green Energy and Trina Solar, among others, will discuss the future of PV manufacturing at Greentech Media's Solar Industry Summit 2011 on March 14 and 15. GTM Research's Shyam Mehta gives some of his thoughts on U.S. manufacturing below.

***

On January 14 of this year, Massachusetts-based module manufacturer Evergreen Solar announced it would be closing its 160-MW integrated wafer-cell-module complex in Devens, Massachusetts by the end of this March and shifting all its manufacturing operations to China. That decision, which will lead to more than 800 of its 925 employees being laid off, was met with a lot of humming and hawing by industry insiders. After all, hadn’t Evergreen already made initial steps in that direction by contracting cell and module production to China way back in 2009? Hadn’t its technology advantage of industry-leading silicon utilization almost evaporated with the onset of a sub-$100/kg polysilicon environment? And didn’t this company struggle to turn a profit even at the best of times? In the minds of most industry observers (especially those that were part of the investment community), Evergreen’s latest struggles (of which there have been quite a few) were acts of a tragedy that was playing out in all-too-slow motion, since the ending was known well in advance: this would be insolvency, followed by a possible licensing of its string ribbon IP to a well-capitalized Chinese firm or an equipment producer like Applied Materials. (Personally, I don’t agree that the writing is on the tombstone for Evergreen quite yet, but that’s a story for another day).

In the wider world, however, the news of Evergreen’s plant closure has fueled discussions around a set of broader issues. First, it was presented as evidence that the U.S. renewable energy industry was losing the “green race” to China, crucially in an era where cleantech has been hailed as the key to revitalization for the U.S. economy. More specifically, it also highlighted the seemingly insurmountable difficulties faced by domestic PV manufacturers in staying competitive with Chinese peers in a global industry. In the words of Evergreen’s CEO, “Solar manufacturers in China have received considerable government and financial support and, together with their low manufacturing costs, have become price leaders within the industry…we expect the United States will continue to be at a disadvantage from a manufacturing standpoint.”

The last few words effectively damn the future of domestic PV manufacturing to failure. Forget your fancy technology, your manufacturing standards, your skilled labor, your “Made in the U.S.A.” labels, Evergreen seems to be saying. It doesn’t matter -- it’s a fixed game, and China holds all the cards. Is it correct in saying so?

What Doesn’t Work

First, let’s look beyond the singular example of Evergreen. The last year has seen at least two other prominent PV factory closures in the U.S. -- BP Solar’s plant in Maryland and Spectrawatt’s fledgling facility in New York. In each case, it is safe to say that a lack of cost competitiveness was a major contributing factor.

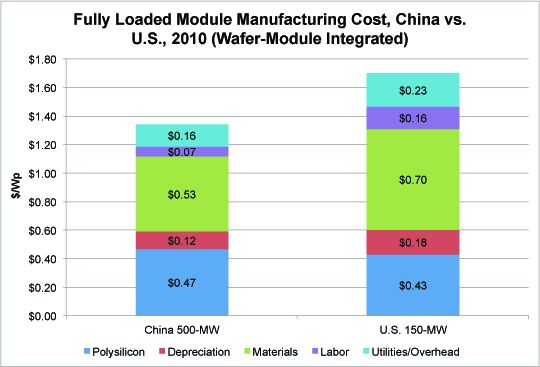

_450_575_80.jpg)

Interestingly, all the facilities in question have been crystalline silicon-based. To undermine the myth that PV manufacturing is a high-tech game, the technology that represents 80% of the global market today is highly mature, has been around for 25 years, and is fairly cookie-cutter as far as its implementation is concerned. Evergreen’s fancy (and more expensive than average) wafers aside, these facilities were basically making the same stuff as the Chinese, at the same efficiency, using the same set of capital equipment, and with almost identical production processes. And while Western and Japanese manufacturers would have you believe otherwise, claims of meaningful differences in module performance or energy harvest between them and the largest Chinese manufacturers have yet to be substantiated. So unless you were to have secured polysilicon at a much lower price than the Chinese (which was true for most Western manufacturers until 2009), why would you expect to be competitive with them? A look at the chart below tells you that they have crucial advantages in almost every aspect of c-Si module cost structure, be it labor, utilities, materials, or overhead. In short, the argument that you can’t beat the Chinese is more correctly expressed as: you can’t beat the Chinese at their own game, which is high-scale manufacturing of a commoditized product.

What Might Work

Located far away from all the doom-and-gloom pronouncements about domestic PV manufacturing is a large factory in Perrysburg, Ohio that manufactures CdTe modules. It is owned by First Solar, and by all accounts, is doing rather well: it produced an estimated 206 MW in 2010 at below 90 cents a watt, which at its current efficiency (11.6%), is extremely competitive. In fact, First Solar feels so comfortable with its U.S. presence that it announced it would construct an additional U.S. plant with an initial capacity of 250 MW by 2012.

So how can First Solar’s U.S. operations continue to be competitive with the Chinese despite all the above-discussed advantages the latter enjoys in manufacturing? Well, First Solar’s technology is low cost (even penalizing it for its lower efficiency relative to c-Si), but it’s also proprietary; it has designed and assembled its own equipment and developed its own process flow, and so far, the Chinese have been unable to duplicate it with any degree of success. Of course, First Solar’s modules would certainly be cheaper if they were manufactured in China: indeed, the U.S.-made modules cost about 10 cents a watt more than those produced at First Solar’s gigawatt-scale fab in Malaysia, another low-cost location. But the Ohio plant is competitive today, and that’s the point; just because the modules could be produced for a slightly lower cost elsewhere is not in and of itself a reason to close a plant. Besides, China’s lower labor costs are less of an issue since the process is so highly automated, and shipping costs (around 4 cents a watt for CdTe) and non-cost factors (proximity to corporate headquarters and R&D resources) play a role when the geographical cost difference is less significant. The moral of the First Solar story is that for a domestic facility to succeed in today’s global market, the technology it deploys must be both low (delivered) cost and proprietary. At this point, First Solar stands alone in this regard, but in this case, the exception does prove the rule. While commercializing disruptive technologies is fraught with risk, it is what the hopes of U.S. PV manufacturing must rest on, for the most part.

In light of this discussion, it’s useful to take a look at recently announced and constructed U.S. PV plants, listed in the table below. These fall into one of two categories. The first class of plants (potentially large thin film plants, most of which utilize highly proprietary technology) fits the general description of what might work above, although only time will tell whether they succeed in lowering costs to competitive efficiency-adjusted levels with the Chinese and clearing product reliability and bankability hurdles associated with new technologies. From the point of view of these manufacturers, the rationale behind locating their plants in the U.S. has little to do with a desire to see America return as a competitive PV production force; it comes down to proximity to R&D resources and key personnel (mostly based in Silicon Valley), the fear of IP theft in countries like China and India, and the generosity of state governments in doling out incentives, since all these firms are startups that have burned through a great deal of their VC funding in the attempt to optimize process flow.

_450_945_80.jpg)

The second class of recently announced/constructed U.S. plants includes small to mid-sized c-Si module assembly plants owned by global players with a much-larger manufacturing base outside the U.S. (Kyocera, SunPower, Suntech). In this case, the facilities are meant to serve the growing end-market in the U.S., which, as GTM Research’s latest Solar Market Insight report will shortly reveal, doubled last year. Many of these plants were also planned in early 2009, when rumors of “Buy American” protectionism were flying around: firms with a foreign manufacturing base targeting the U.S. as a major sales prospect feared that they would be shut out of the market. While I’m not convinced as to the reasoning (do you really need to build a plant in a market to serve it? Wouldn’t a sales office do? How much demand will be driven by military and public works projects? And how many installers care about “Made in the U.S.A” labels?), the small scale of these plants would have a minimal impact on blended costs -- although they would be the first to be closed during a down cycle.

It’s also important to note that U.S. states were not created equal with regard to their suitability for PV manufacturing. The first wave of U.S. plants was largely based on the Eastern seaboard (Maryland, Delaware, Massachusetts). Ideally, a plant should be located in a region that has cheap power prices, a cost-effective yet technically skilled workforce, and meaningful state incentives for renewables manufacturers. None of the states named are particularly attractive based on these criteria. While many thin film manufacturers have chosen to build their first manufacturing plants close to key R&D personnel, which have been based in Colorado (NREL) and California (Silicon Valley), these fabs will likely stay in the small-to-mid-sized range, while the larger “follow-up” plants have been planned for states such as Ohio, Oregon, Indiana, and Mississippi, which may be wiser bets.

Would Incentives Work?

Another source of competitive advantage for Chinese firms that the above cost graphic does not even take into account is the availability of huge reserves of low-cost capital; as of the end of 2010, Chinese PV firms had received over $30 billion in low-interest loans from state banks. For many, a cure-all for the U.S.’s solar manufacturing woes would be to level the playing field by offering financial assistance to domestic manufacturers, be it through low-interest loans, tax credits, or grants.

The question with government support is, how much? U.S. manufacturers are already receiving hundreds of millions of dollars from both the DOE and state governments: Abound and Solyndra have received loan guarantees worth a combined $935 million, while SoloPower is on its way to being awarded $197 million from the same program. Meanwhile, Stion and AQT should receive loans totaling around $200 million from Mississippi and South Carolina. While this pales next to the scale at which China has capitalized its manufacturing firms, the firms named above would be hard pressed to complain.

The second point is to what extent up-front capital subsidies (assuming they are not doled out on a whim, as one could argue is the case in China) can ultimately make a difference. Capital assistance of any sort indirectly lowers costs by allowing you to scale, and crucially, to stay afloat while you’re selling below market price until that time. But while you can make the argument that such assistance may be necessary to provide domestic manufacturers with a jumpstart, it is in no way sufficient. Put another way, incentives may get a plant built, but they won’t keep a plant running. Low-cost debt lowers your cost of capital, and therefore allows you to price product at a lower margin, all else equal, but has little effect on your cost structure. On the other hand, tax credits of the form received by Solarworld and Sanyo through Oregon’s BETC (Business Energy Tax Credit) may cut the cost of equipment and construction by half. This is certainly important given that up-front capital is front-of-mind for would-be manufacturers, but depreciation does not have a huge say in the final module cost structure, as can be seen above: a 50% reduction in capital expenditures would lower the overall gap by only 3%. On a side note, spare a thought for Big Brother: when it actually does step in and provide assistance as in the case of Solyndra and its $535 million loan guarantee, it’s eviscerated for wasting taxpayer dollars. Conversely, in the instance of the Evergreen affair, it’s accused of bringing a knife to a gunfight. Just can’t win.

Would Protectionism Work?

One simple way to stimulate domestic manufacturing (at least, at a level proportional to the size of the end-market) would be to institute a Domestic Content Requirement (DCR) for subsidy eligibility, such as that in Ontario, which requires that 60% of the cost of labor and materials of an installed system originate domestically for feed-in tariff eligibility. This has led to a flurry of plant announcements in Ontario over the past year and a half, including plants from Solar Semiconductor, Celestica, Canadian Solar, and Siliken. Indeed, if there ever there were an argument for build a plant, it would be to do so in a market with healthy installation incentives that also has a meaningful DCR.

But there are multiple problems with this viewpoint. First of all, such a policy would have the effect of keeping prices (especially for domestic components) artificially high, which would undermine the constant and urgent need to lower the delivered cost of PV. And a market like the U.S. that does not have a feed-in tariff is highly price sensitive, meaning this could dampen the growth of the market significantly -- which would ultimately translate to lower installations, less solar electricity generation, and fewer BOS-side jobs. Would this be a sacrifice worth making? Moreover, it puts domestic facilities more or less at the mercy of the domestic market: if (some would say, when) the Ontario market imploded, manufacturers in that region would find themselves at a significant competitive disadvantage to the rest of the world, and the denouement wouldn't be pretty.

Do We Really Need to Make it Work?

All of this brings us to perhaps the most important question in this discussion: why should we be so hell-bent on preserving American solar manufacturing in the first place? Does it have anything to do with the actual generation of solar electricity in this country? Not in the slightest. Could it be energy security? Comparisons with oil don’t really cut it; we procure 85% of our electricity needs from coal, natural gas, and nuclear, most of which is sourced domestically, so there is no pressing concern here. Is it jobs? A module assembly plant creates roughly 1.5 jobs per megawatt; hardly the panacea for our unemployment woes. Meanwhile, installations create three times as many jobs, and this is work that cannot be outsourced. But a factory with moving parts, permanent “green” jobs (few as they may be), cranking out thousands of pretty panels a day seems a lot sexier than a rooftop installation on a Walmart store that is silently producing clean electrons. What seems to be the case is that manufacturing is held up as some sort of status symbol, both in the minds of politicians and the public, partly because it is tangible, and partly on account of nostalgia for a bygone era.

If there is one word that characterizes the PV industry today, it would be “dynamic”. The sector is just beginning to move past infancy towards early childhood, and there’s no telling what the global manufacturing landscape will look like as a fully formed adult. However, it is safe to say that the near-term hopes of U.S. PV manufacturing rest squarely on distributed c-Si module plants and thin film innovation at a large scale. The latter will need a combination of capital assistance, technical expertise, and luck to succeed, but if they don’t, maybe it’s not end of the world. After experiencing 100% growth in installations last year, all signs point to another doubling of U.S. demand in 2011, in no small part due to cost reductions and sales penetration by Chinese c-Si manufacturers. It’s not always a zero-sum game.

***

Watch executives from Abound Solar, Stion, and Suntech Power discuss the future of U.S. PV manufacturing and a host of other issues at Greentech Media’s annual Solar Industry Summit at Palm Springs on March 14 and 15.

41

41

15

15

9

9