With bank funds -- by some estimates, in the trillions -- on the sidelines waiting for safe investments, the stimulus bills’ infusion of $65 billion in 2009 and 2010 saved the renewables industries.

Maybe the loan guarantees didn’t always work out, but the solar industry is soaring thanks to the six-year extension of the investment tax credit (ITC), and the wind industry will get at least one more good year out of the three-year extension of the production tax credit (PTC). Both are far better off for the cash grant provision and the manufacturing tax credits in the 2008 stimulus bill and the 2009 American Recovery and Reinvestment Act (ARRA).

Despite the occasional media hubbub, renewables investments have been sound. Jobs are being created. And even if the nation’s economic growth remains slow, demand for electricity will slowly increase and state mandates will drive demand for renewables, assuring returns on future investments.

But wind faces a challenge. The stimulus bills’ cash grant and manufacturing tax credit provisions would appear to be history after 2011. Given Congress’s penny-pinching impulses, extension of the PTC beyond 2012 is in serious doubt.

Meanwhile, those trillions sit idle while banks look for sound investments.

A report titled "The Return -- and Returns -- of Tax Equity for U.S. Renewable Projects," commissioned by The Reznick Group, argues the PTC should be extended because the returning need for tax equity financing in the wind industry could benefit the broader economy by putting that bank money to work while providing wind with urgently needed support. (The current study is on wind investments. A study on solar is in the works.)

“The total need for tax equity financing next year could be more than seven billion dollars,” the study states. That “exceeds the investment appetite of established tax equity providers, [... but] the 500 largest public companies in the U.S. alone paid $137 billion in taxes” last year.

“U.S. corporations have historically made use of these kinds of incentives,” the study also reports, noting that Google and Pacific Gas & Electric have already gotten back in the renewables’ sector tax equity market.

There were “comparable numbers” to that seven billion dollars invested in the PTC in the expansion years before 2008, according to Reznick Group Renewable Energy Practice Leader Tim Kemper. “It was a little off,” he said, which is why the report further argues that Congress should give the wind industry both a PTC extension and the option of an ITC. “It is going to be important that we entice additional investors,” Kemper said, but for some investors, the PTC is “not their parameter for making tax investments.”

The PTC gives investors a 2.3 cent tax credit for every kilowatt-hour of electricity the project generates. The ITC gives investors a tax credit equal to 30 percent of their investment at the end of the project’s first year of production.

“Optionality,” Kemper said, attracts a new set of investors. The ITC option “makes deals that potentially weren’t doable in the past able to get financed.”

It is broadly assumed, Kemper explained, “that PTC works better for an investment that is very high capacity factor and costs are relatively reasonable,” while “the ITC is better for low capacity factor and higher costs.”

This serviceable generalization is, however, inadequate for the many different kinds of wind projects being proposed.

Ambitious undertakings, despite the potential for tremendous productivity, might more easily find backing as more tax equity returns to the PTC market. For example, Oregon’s 845-megawatt Shepherd’s Flat land-based wind project went ahead only after it won a DOE loan guarantee.

In the U.S. Southeast, projects aimed at taking advantage of new wind technologies that can harvest very low winds may not have the productivity to interest PTC investors, but might attract those who see value in an ITC-based investment that provides a big tax credit relatively quickly.

Bluewater Wind CEO Peter Mandelstam, who may be out of business if the tax credits are not extended, recently pointed out to GTM that neither DOE loan guarantees nor the PTC would serve offshore projects. Though they have enormous productivity potential, they take too long to get built to qualify for a DOE loan guarantee. They take even longer to provide a return on production to PTC investors. “What really focuses a banker’s attention is the prospect of closing a deal within six months,” Mandelstam said in calling for a policy that gives onshore developers a PTC and offshore developers an ITC.

“You have to look at each deal individually,” Kemper said. It is not clear that either the PTC or the ITC is absolutely preferable for a developer or an investor. What is clear is that offering the choice “broadens the deal base.” Without both options, he said, “you are cutting off capital to the market.”

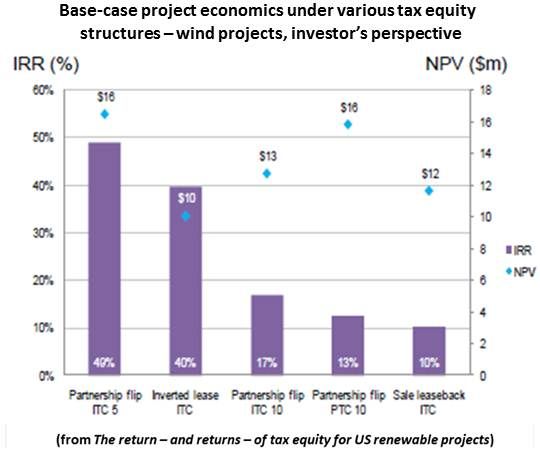

The Reznick Group study breaks tax credit investment into three primary tax equity structures: the partnership flip, the sale leaseback and the inverted lease. Each offers advantages and disadvantages. “It really comes down to what the tax equity investor is comfortable with,” Kemper said, “and what the developer is trying to achieve."

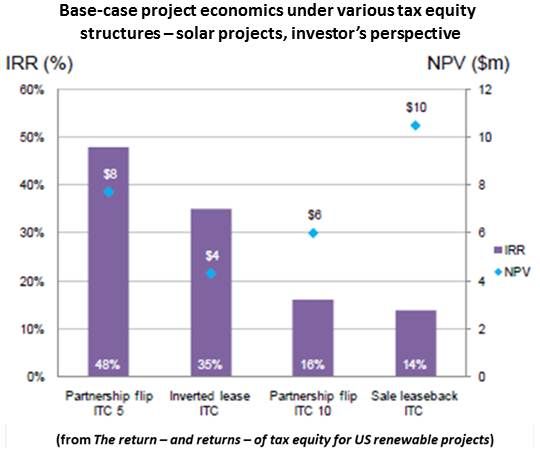

A “base-case analysis,” the study reports, “shows developers achieving returns of 6 percent to 19 percent and investors achieving 10 percent to 49 percent for wind projects.”

Optionality would facilitate the best returns because investors and developers could choose, as the study reports, between the ITC and the PTC based on “the three ‘P’s: performance, perspective and priorities.”

41

41

15

15

9

9