Good locations for utility-scale wind projects are getting harder to find than ruby slippers in Oz. At likely sites, developers often encounter environmental issues, local opposition and/or inadequate transmission access that can consume time and money even as the marketplace becomes more competitive.

It could be that what the Good Witch of the West told Dorothy right before she went back to Kansas is just the advice wind developers need to hear: “If you ever go looking for your heart’s desire, never look any farther than your own backyard, because if it isn’t there, you never lost it to begin with.”

In their own backyards, developers can find a niche segment of the wind sector known as community wind which could eliminate their problems, according to Lawrence Berkeley National Laboratory research scientist and wind authority Mark Bolinger.

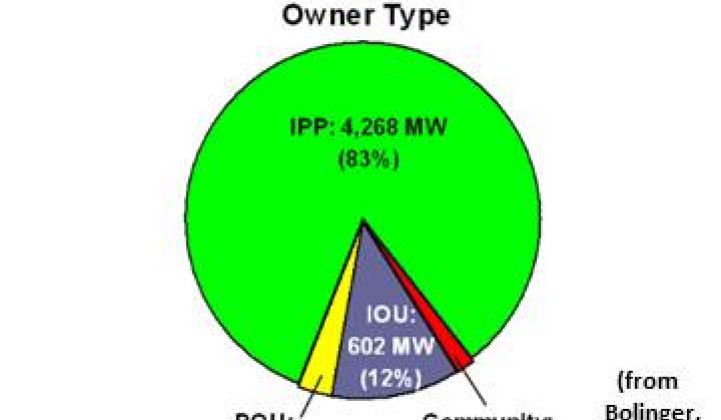

“Community wind is any wind project using utility-scale turbines, those greater than 100 kilowatts,” Bolinger said, “that is not owned by an investor-owned utility (IOU), not owned by a publicly owned utility such as an electric cooperative or a municipal utility (MOU), and also not owned exclusively by an independent power producer (IPP).”

Bolinger spoke as part of an Agrion Global Network for Energy online introduction to community wind webinar. Speaking with him was Ray Henger, Chief Financial Officer for community wind developer Own Energy. Henger set out the three basic community wind ownership models.

Community wind that is “self-funded locally” is typically owned by “one or two people or a community institution like a university or a hospital,” Henger said. Technical services are typically outsourced to professional operators. Such owners usually retain control up to their “funding limits.”

If “community funded locally,” Henger said, a “partnership group uses community funds and there is community participation and buy-in.” Management, he added, can be complicated by the broader ownership base.

In the third model, local interests team up with a national IPP partner. Significant equity and responsibilities remain at the local level, Henger said, until the later stages of development, when the more experienced and better funded IPP provides necessary capital and takes a larger role.

The primary distinction, Henger said, “is the point at which the costs to develop a project begin to get replaced by the long-term equity that ultimately gets outsourced” to “a larger group or a national partner.”

Last year, there were 20 community wind projects built in 12 states representing a 91-megawatt installed capacity. By the end of the first half of this year, 108 megawatts of installed capacity have come online in 13 projects across six states.

The 2011 growth spurt, Bolinger said, is fueled by the 2009 Recovery Act provision allowing community wind developers to use the federal 30 percent investment tax credit (ITC) or a cash grant in lieu of the ITC through the federal 1603 program.

Previously, Bolinger said, developers were limited to tax-based incentives. A combination of production tax credits (PTCs) and Accelerated Tax Depreciation (ATD) would cover approximately 41 percent of a community wind’s installed cost. Now, with the 30 percent cash grant and the ATD, developers can cut the installed cost in half and less than half of the benefit is tax-based.

And, Bolinger said, because the incentives are based on cost rather than performance, higher cost projects become practical and a turbine with a standard 25 percent to 35 percent capacity factor generates viable returns and a five- to six-year break-even.

Though Recovery Act incentives have led to an expansion of community wind development, Bolinger said, their expected demise in the present impecunious Congress will likely prevent community wind from emerging from niche status.

Bollinger detailed a list of ancillary benefits that add to community wind’s appeal.

Utility-scale developers who use turbines from manufacturers without a proven U.S. performance record often face difficulties securing the financing they require, Bollinger explained. On the other hand, community wind’s lower financing threshold offers new turbine makers the chance to enter the broader U.S. market, especially if they provide “a favorable term price and a stronger warranty.”

Five 2010 projects used turbines made by U.S. market entrants (Alstom, Unison, Hyundai, Kenersys). Previously, Suzlon, DeWind, Goldwind, AAER, Nordic, and PowerWind used community wind to get market footing.

And, Bolinger noted, community wind eliminates barriers for new investors, owners and operators. Because these projects are smaller in scale and often financed at a local level, local banks may be willing to take a financing risk in the hopes of striking up an ongoing relationship with a potentially successful turbine maker, particularly if the company has a proven track record in another country.

As a result, Bolinger said, community wind can be “a testbed for financial innovation and a local economic engine.”

Henger concluded the Agrion presentation by detailing ways community wind financing works. “Tax equity providers have become reduced,” he said, adding, “the cost of tax equity is still in the eight percent range.” As a result, “community wind currently suffers” and “will require a higher cost of capital to complete.” Presently, “the focus is no longer on debt; the focus is on tax equity.”

Nevertheless, good places for Big Wind remain hard to find, while there are people in every community looking for good deals, even in wind developers’ own backyards.

41

41

15

15

9

9