In a surprising move earlier this month, DNV GL announced its acquisition of Spanish solar monitoring firm GreenPowerMonitor. Three days later, BlueNRGY, the solar and wind EPC/O&M provider that picked up financially distressed U.S. monitoring provider Draker Energy in 2015, announced a $3.7 million investment in U.K.-based competitor Inaccess. Inaccess' CEO was tapped to lead the Draker business. And the very next day, O&M and asset management company Bay4 Energy Services gobbled up wind and solar PV monitoring firm Ekhosoft.

After this latest batch of transactions, five of the top six monitoring independent software vendors (ISVs) are now owned by a larger entity. Germany-based market leaders meteocontrol and skytron energy are subsidiaries of vertically integrated firms Shunfeng and First Solar, respectively; and Solare Datensysteme (maker of Solar-Log products) is owned by Swiss utility BKW.

Further down in the global rankings of monitoring providers, two major U.S. players were also the recent targets of acquisitions: Locus Energy was acquired by energy market data provider Genscape, and Power Factors was acquired by O&M firm MaxGen Energy Services. All eyes are now turning to AlsoEnergy, the No. 1 monitoring ISV in the U.S. and the only large player in North America that has not yet been acquired.

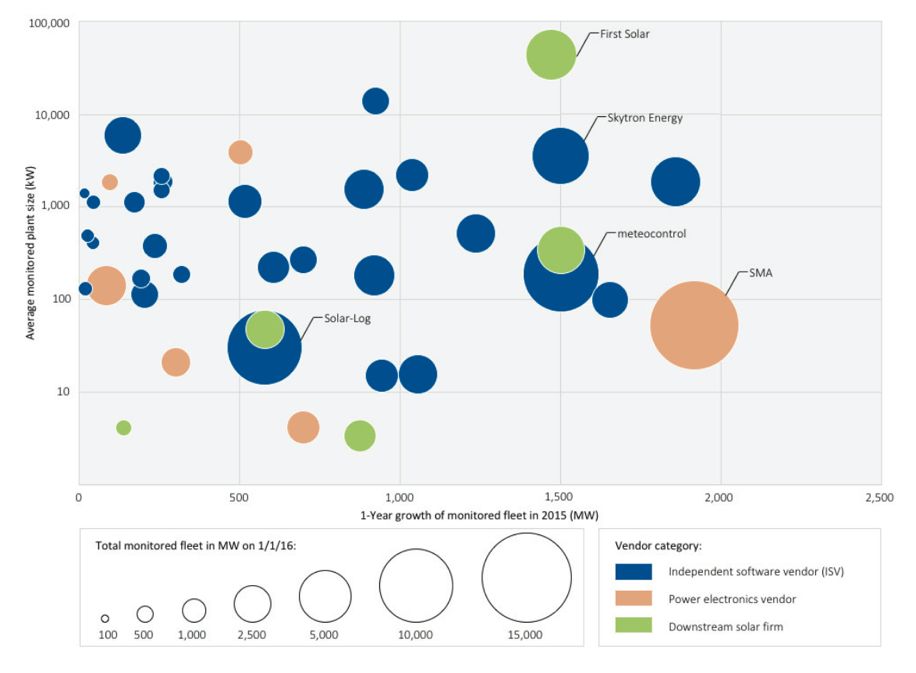

Despite such intense M&A activity, however, the market is not consolidating. Most of the recent changes in vendor ownership fail to reduce the number of active market players. The global solar monitoring space remains very crowded, as shown by the competitive landscape chart below from GTM Research’s latest global PV monitoring report.

Source: Global PV Monitoring 2016: Markets, Trends and Leading Players by GTM Research and SoliChamba Consulting

Companies are changing hands. But they keep offering the same products with the same business models. And they face the same challenge of having to reduce costs in order to protect margins as prices get squeezed in every market and segment.

The most recent notable consolidation events in the monitoring market came in 2013, when AlsoEnergy acquired competitor and U.S. commercial PV monitoring market leader Deck Monitoring, and Inaccess acquired the U.K. PV monitoring market leader Sense One Technologies. Since then, many acquisitions occurred -- but none of them resulted in market consolidation.

From this perspective, the most intriguing announcement of this past week is the seemingly complex BlueNRGY/Draker/Inaccess deal. Inaccess was in the process of acquiring Draker before BlueNRGY bought the business last year. By taking the helm of Draker, Inaccess has an opportunity to consolidate two software platforms over time, as it did with the pvSense product it acquired in 2013.

This effort obviously comes with challenges and risks, but it has the potential to bring Draker and Inaccess economies of scale with a combined monitored portfolio of 6 gigawatts. In the Global PV Monitoring 2016 report, Inaccess ranked No. 6 globally among ISVs in 2015, and Draker was No. 11, while the combined entity would rank fourth.

Will AlsoEnergy be the next target for a large corporation looking to get into the monitoring business?

***

For more information on PV monitoring market size, trends, and competitive landscape analyzed by country and segment, read Global PV Monitoring 2016: Markets, Trends and Leading Players by GTM Research and SoliChamba Consulting.

41

41

15

15

9

9