Hopefully, the engineering and investment community has learned something from the $4 billion to $5 billion invested in the CIGS solar material over the last decade. We've watched a number of copper-indium-gallium-diselenide solar companies raise funding and collapse with varying degrees of drama -- including Solyndra, Nanosolar, SoloPower, and AQT.

In March of this year, Solexant re-emerged from stealth. The firm began in 2006 as a cadmium-telluride (CdTe) solar on roll-to-roll startup and was on the same build-a-factory-before-the-process-is-optimized death spin as the rest. But the board switched in semiconductor equipment/process veteran and solar investor Brad Mattson in June 2011. Mattson was the CEO and founder of semiconductor equipment successes Mattson Technology and Novellus Systems.

Mattson shut down the 100-megawatt factory plans, scaled back the headcount, increased R&D and took a good look at what the company was doing. Mattson had seen over 200 solar startups while at VantagePoint Venture Partners and went about studying the solar materials systems and processes with a relatively blank sheet of paper. At one point, the firm was investigating five materials systems. Solexant acquired the remains of Wakonda (GaAs), set world records in CZTS, and worked further with CdTe.

A few years of R&D, some strategic hiring, and a cooperative set of investors have yielded a new technology slant and a new name.

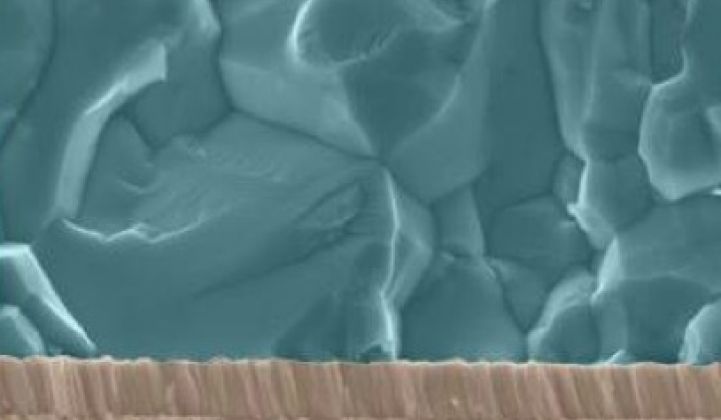

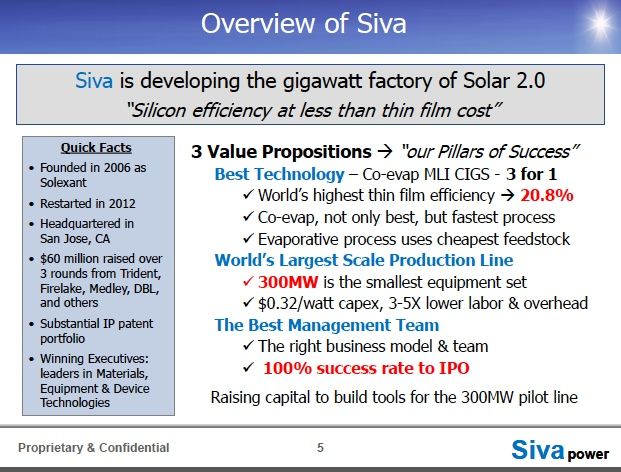

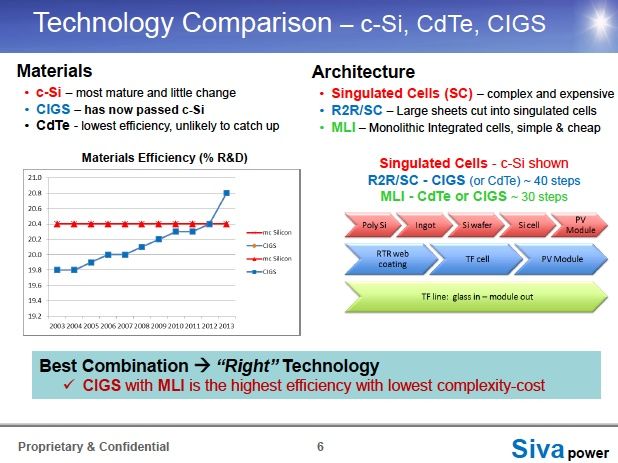

Solexant is a now called Siva Power -- a CIGS solar module manufacturer. Mattson's ultimate technology conclusion was monolithically integrated, co-evaporated CIGS on glass, because it is "higher efficiency than anything else." (Not sputtering, not electroplating, not roll-to-roll, not foil, no singulation, no MOCVD.) As in semiconductors, Mattson is looking to lower the cost of ownership -- and he has done it before. Mattson called co-evaporated CIGS one of those rare instances and a "gift of physics" where the highest efficiency solution is also the fastest. Co-evaporation doesn't require the selenization step needed in a sputtering process.

Mattson and CTO Markus Beck (bringing immense CIGS experience from Solyndra and First Solar) look to build "a profitable path to sub-$0.40 per watt solar power, along with unprecedented production scale."

The rebranding, the book tour, the hair plugs, Mattson at the Emmys -- it's all about raising money for a 300-megawatt CIGS production line. And that is as much of a challenge as producing 300 megawatts of 15 percent efficient CIGS cost-effectively.

“It has been frustrating to see CIGS technology breaking efficiency records for many years, but not see that technical success translate into success in the commercial arena,” said Dr. Rommel Noufi, a member of Siva's advisory board, in a release.

Mattson realizes the challenge in CIGS, saying, "The ability to adjust the CIGS composition is not a negative, as portrayed, but a positive, because it allows you to vary the composition through the film with different stoichiometry on the back contact, bulk, and front contact. This is an awesome advantage and one of the reasons CIGS holds all the records. Yes, it requires superior process control, but we figured out how to do process control in other industries decades ago."

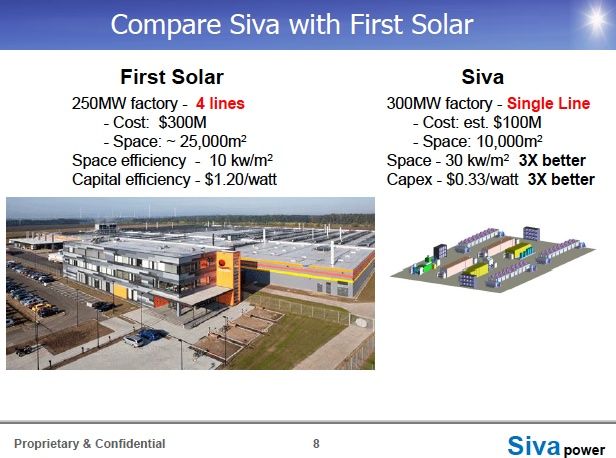

Mattson sees the solar industry as being in the "gigawatt era" -- but the idea with thin film is to build that gigawatt in a 10,000-square-meter factory, not a 200,000-square-meter factory.

Mattson speaks like someone who has taken a sober look at the energy gap and found the obvious answer is solar power and thin-film solar built in America, at that. Natural gas, wind and solar are the generation sources of the future, according to the CEO. New solar installation eclipses wind in 2013, said Mattson, and natural gas has passed its peak. "Now is the time to invest in solar," said the CEO, adding, "We are at the beginning of a 30-year to 45-year-long S-curve."

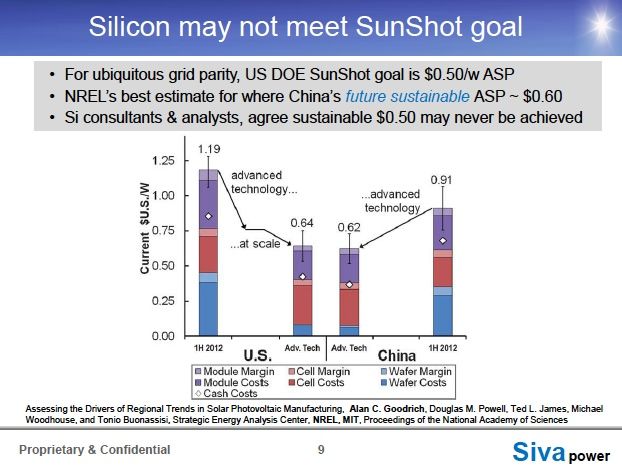

Mattson insists that silicon solar panels have a "real sustainable cost of 70 to 80 cents [per watt]."

For Mattson's CIGS reboot, it's about scale, repeatability, and smart vacuum tool and source design. Mattson called the source "the heart of the system" and noted that Beck, the CTO, was on his fourth-generation design of CIGS evaporation sources. Mattson said, "The rest is vacuum glass handling like flat-panel displays."

Mattson's team has determined that roll-to-roll processing actually has lower throughput than glass handling. Roll-to-roll requires singulation and diodes; Mattson also suggests that working on metal is a limitation to process efficiency and conversion efficiency.

For Mattson, CIGS' second act is about scaling -- building one 300-megawatt system instead of building ten 30-megawatt systems. Mattson said that First Solar is winning because of scale. "Their substrate is 30 times better than silicon -- but they picked the wrong material."

Mattson looks out at the "pioneers with arrows in their backs" and VCs already singed by CIGS -- and sees other asset classes as potential sources of capital.

Here's a partial list of CIGS solar players, both active and inactive:

- Solar Frontier, 577 megawatts shipped in 2011

- Solibro, 95 megawatts shipped in 2011 (sold to Hanergy)

- MiaSolé, 60 megawatts shipped in 2011 (sold to Hanergy)

- Solyndra (bankrupt)

- Avancis (stopped manufacturing in Q3)

- Global Solar Energy (selling consumer solar, sold to Hanergy)

- Soltecture (bankrupt)

- Manz

- Nanosolar (bankrupt)

- AQT (bankrupt)

- HelioVolt (no commercial production, majority owner is SK Innovations)

- Ascent Solar (selling consumer solar, majority owner is TFG Radiant)

- ISET (company is transitioning to "micro-solar components")

- Stion (limited commercial production, allied with TSMC)

- SoloPower (dormant)

- Siva (formerly known as Solexant, co-evap on glass)

- Solarion

- TSMC (technology licensed from Stion)

- NuvoSun (acquired by Dow)

Siva has raised more than $60 million from Olympus Capital Partners, DBL Investors, Birchmere Ventures, Trident Capital, Firelake Capital, and Medley Partners.

Mattson has lived through a number of semiconductor business cycles and sees the solar industry at the beginning of a long growth curve. "The challenge isn't the science. It's an equipment challenge. It's engineering. And it can be done." He added, "Silicon scaled, but the Chinese are not scaling -- they are replicating like a cookie cutter. This is not scaling. China cannot compete with us if we scale properly."

41

41

15

15

9

9