At the first industry gathering since Congress extended the PTC and changed the language to help the industry return to substantial growth by 2014, keynote speaker Dan Reicher and others talked about what might be ahead at the American Wind Energy Association’s Western Regional Summit.

“The industry lived to fight another day,” said Reicher, a former Google and Clinton administration energy expert now at Stanford, “but the need to find another incentive mechanism is clear.”

California’s Renewable Portfolio Standard (RPS) goal of getting 33 percent of its power from renewables by 2020 is a floor not a ceiling, promised California Governor’s office Deputy Director of Planning and Research Wade Crowfoot.

Governor Jerry Brown’s RPS will continue to drive growth because Brown’s vision is of an efficient and renewable energy system and an electrified transportation system, Crowfoot said, and the larger goal remains cutting California greenhouse gas emissions 80 percent by 2050.

But getting more renewables into the mix raises five important questions, Crowfoot said.

- How large a percentage of power can renewables provide to the grid?

- How does the grid balance an increasing percent of renewables and what is the balancing solution? Is it storage? Is it charging EVs at night?

- What kind of policy will grow renewable energy without “burning the ratepayer” with excessively high utility prices?

- What is the sustainable incentive solution that moves renewables beyond the boom and bust cycles caused by the PTC?

- What is the right balance between renewables development with other (military readiness, environmental, etc.) questions?

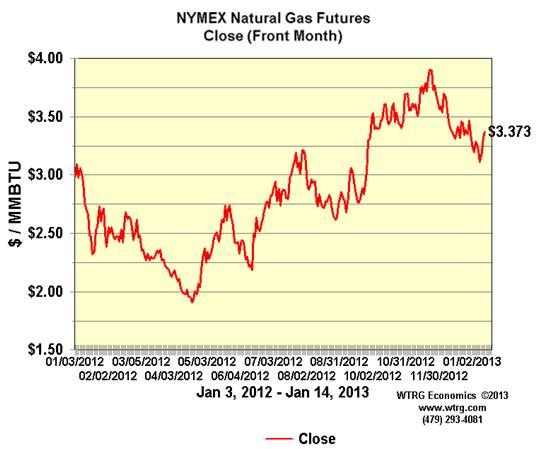

SDG&E VP Matt Burkhart said the recent opening of new transmission has been key to keeping utilities on track to meeting RPS goals. Low natural gas prices have also been important, he said, because they have allowed power prices to remain low as increasing levels of renewables were integrated.

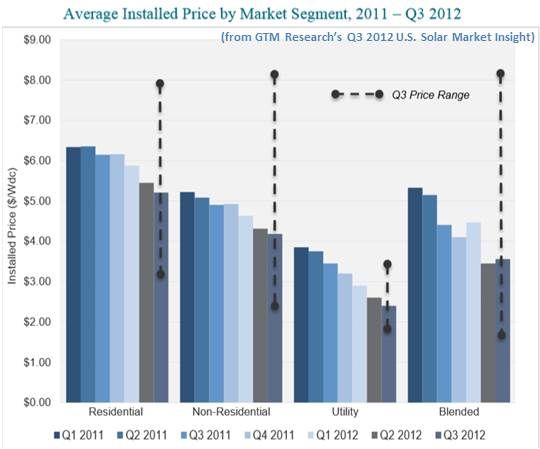

Going forward, Burkhart said, utilities will be fine-tuning their portfolios as they pick renewables for their nearly fully contracted remaining RPS requirements. Wind may be more seriously challenged by the falling price of PV, and because PV solar harvests energy closer to the power companies’ peak demand needs, wind will have to lower its already-competitive prices.

The opportunity, Burkhart said, may be in smaller projects. Projects of between one and twenty megawatts driven by programs like California’s Renewables Auction Mechanism (RAM) and a state subsidy aimed at growing distributed generation could appeal to the marketplace worn out by the challenges of siting and financing mega-projects.

Reicher said the answer to the subsidy issue could be in Master Limited Partnerships (MLPs) and Real Estate Investment Trusts (REITs), investment mechanisms that depend not on federal support but marketplace buy-in. Such investments are already available to the oil and gas industry, Reicher said.

Opening up the opportunity to smaller investors, he explained, democratizes the ownership of renewables.

Congress will have to legislate the use of MLPs in the renewables sector, Reicher said, but a Treasury Department “finding” can make REITs available to renewables investors. Though congressional action is a big ask, Reicher acknowledged, renewables would only be asking for the tools that other generation sources have.

A key factor in demand growth, Reicher said, is the “perfect marriage” between natural gas’ firming of wind’s variability and wind’s stabilizing of natural gas price volatility. “The only thing about natural gas’ price you can be sure of,” he said, “is that you can’t be sure of it.”

Factors such as state RPSs, EPA rulings that have made fossil fuels more expensive, regional carbon markets, plug-in cars charging at night when wind is abundant, increasing use of renewables by the DOD, new transmission where wind is abundant, and growth in distributed wind, offshore wind, and international wind markets all add to Reicher’s expectation for rising wind demand.

Repowering the 1980s-built infrastructure of the original U.S. utility-scale wind projects, EDF Renewables VP Mark Tholke said, could be a potentially large new source of demand.

Expirations of 1980s contracts will open the opportunity to replace 300-plus megawatts in 2015, 200-plus megawatts in 2016, and 100-plus megawatts in every successive year to the end of the decade. On the same footprint, Tholke said, contemporary technology will allow the building of ten times the capacity of the projects being replaced.

Market research described by IHS CERA’s TJ Deora suggested serious obstacles and slowing growth. Following a record-breaking twelve-gigawatt year in 2012 driven by developers’ pursuit of what was thought to be an expiring tax credit, Deora’s research predicted a two-gigawatt 2013 as the wind industry supply chain recovers. That recovery should drive four gigawatts to six gigawatts in 2015 and 2016.

State RPSs will drive demand, Deora said, but factors such as competition from cheap natural gas, cheap PV solar that matches peak demand better than wind, and transmission inadequate to deliver the most affordable wind will work against the industry.

41

41

15

15

9

9