There’s little doubt that 2013 has been a breakout year for grid-scale energy storage. On the utility side, we’ve seen California mandate an unprecedented 1.3 gigawatts of grid storage by decade’s end, and other markets in the United States and abroad are moving toward goals of their own. On the customer side, we’ve seen a flood of entrants making storage a part of their renewable power, distributed generation and commercial energy management plans.

Now comes the hard part: proving that advanced batteries, thermal energy storage, and a whole host of other technologies can compete on economic terms. Part of that challenge lies in reducing costs. The Department of Energy has set a target of $250 per kilowatt-hour for advanced energy storage -- a goal that’s still out of reach for commercially available systems today.

But it’s also important to tackle the other side of the cost-benefit equation and find new ways for storage systems to pay for themselves over time. While energy storage systems are capable of performing many different tasks for the grid and for customers, regulatory and economic barriers must be overcome to allow them to tap these multiple opportunities.

On that front, here are a series of charts that help lay out the key economic opportunities for energy storage in 2014, along with guidelines to the regulatory drivers that could make them possible.

Demand Charges: Unlocking Value for Customer-Sited Storage

Let’s turn first to “behind the meter” energy storage, where a number of industry observers --- including GTM Research -- see the earliest potential for economically attractive deployment. The key to this value is in mitigating demand charges. That's the portion of a customer's electric bill calculated not on how many kilowatt-hours they consume, but on a snapshot of their highest amount drawn from the grid at any single moment.

Demand charges exist to allow utilities to cover utilities’ fixed power delivery costs, as represented by each customer's peak power needs. But in the complicated world of utility rate tariffs, they can also be hiked to make up for revenue lost to shifts in energy prices and reduced energy demand, whether that’s due to falling natural gas prices, a slow-growth economy, increased customer efficiency -- or the spread of on-site solar and other customer-owned generation.

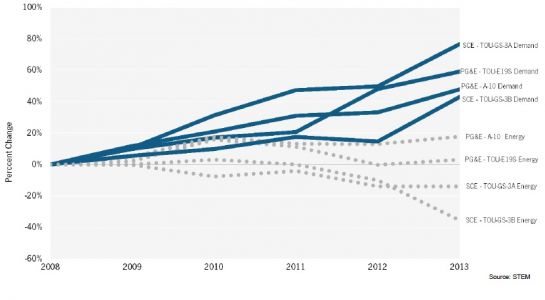

One thing’s clear: in many major U.S. power markets, demand charges are going way up as energy charges are shrinking. Here’s one chart demonstrating that trend for California utilities Pacific Gas & Electric and Southern California Edison, courtesy of energy storage startup Stem:

Similar trends exist in New York and the Northeastern U.S., in Hawaii, in Colorado and in other markets, according to Stefan Kratz, sales director for Stem. Buildings with “peaky” loads (that is, hard-to-predict spikes in usage) have a particularly hard time managing demand, which makes an energy storage system that automatically kicks in to smooth out those peaks a resource with considerable value.

In California, that proposition, along with access to state incentives, has allowed Stem to sign up customers for a collective 6 megawatts of installed storage systems. It’s also the key payback being targeted by storage systems in New York City, where storage projects could also play a role, alongside on-site generation and demand response, to relieve congested distribution systems without forcing expensive upgrades.

There’s another important aspect of demand charge mitigation as a service: its relatively short duration requirements. Preventing power spikes in fifteen-minute intervals is something that a lithium-ion battery can do without having to deplete itself and thus shorten its lifespan.

Storage Plus Solar and Wind: The Next Stage in Renewable Energy

It’s also important to highlight the role that demand charge trends are playing in another growth area for energy storage: backing up customer-owned solar PV. Commercial customers that have installed PV to reduce their energy bills are increasingly finding that storing that solar power provides greater paybacks, whether to prevent demand spikes or to shift it to times of the day when grid power is more expensive, such as the late afternoon and early evening hours.

Pairing solar with storage can also help grid operators and utilities turn an intermittent, unpredictable source of customer-generated power into a more stable and dispatchable resource. But while utilities are driven by grid management imperatives, customers are looking at their own economic drivers, which can include emergency backup power, time-of-use price arbitrage, or playing into ancillary services markets as revenue streams.

Right now, markets like Japan and Germany are leading the charge on solar-storage combinations, driven by incentives and solar feed-in tariff policies that make it more reliable an investment than in the United States. But we’re seeing some important moves in U.S. markets as well, including Solar Grid Storage’s projects on the East Coast, as well as SolarCity’s big move into storage as a low- to no-cost add-on to its third-party solar offering for commercial and residential customers.

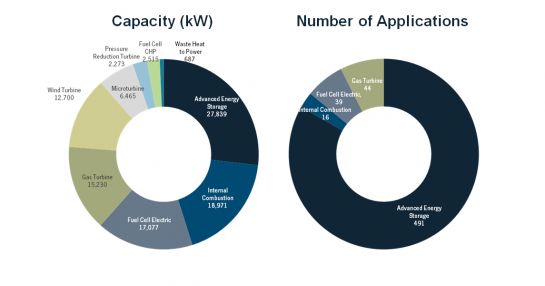

California’s Self Generation Incentive Program, which offers incentives for a wide array of customer-sited energy technology, has seen a huge increase in advanced energy storage (AES) technologies applying for credits, as this chart shows:

Customer-sited energy storage is also given a specific role in California’s new energy storage mandate, though specific rules for how that will be managed are still to be determined. In the meantime, California’s big three investor-owned utilities have thrown up roadblocks to allowing small-scale solar-storage projects to interconnect with the grid -- a move that illustrates the challenges to come in aligning utilities and customers’ interests behind this technology combination.

In the meantime, wind power has long been a test bed for storage that helps smooth its fluctuations in generation, as well as “firming up” the resource for project developers that want to optimize their power purchase agreements with grid operators and buyers. Indeed, the largest energy storage projects to date -- AES Energy Storage’s Laurel Mountain project with A123, and Duke Energy’s Notrees project with Xtreme Power -- are integrated into wind farms.

A September 2013 study from Sandia National Laboratories (PDF) lays out the case for energy storage-renewable integration:

“An energy storage system tied in with a long-term power purchase agreement on a renewable energy power plant also shifts the apparent risk off a utility relative to a standalone system being tied to renewable generation, while at the same time, guaranteeing a revenue stream to the developer. Incentives can also help reduce risk to utilities or developers investing in energy storage systems.”

Frequency Regulation: A Killer App for Grid Storage -- But With Limits

Moving into the world of grid economics, ancillary services -- namely, frequency regulation -- remain the primary economic driver for grid-scale storage today. Providing fast-reacting power resources to manage grid stability is a natural fit for energy storage, particularly under new federally mandated changes to energy markets that reward resources that can react at a moment’s notice.

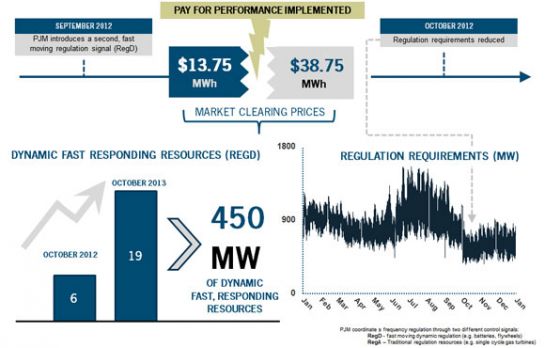

The Federal Energy Regulatory Commission (FERC)’s Order 755 provides just that incentive, and has led to a boom in storage projects providing frequency regulation in territories served by mid-Atlantic grid operator PJM, as this graphic indicates:

Energy storage projects from giant energy companies like AES Energy Storage and NextEra Energy Resources (PDF), startups like Viridity Energy and Enbala Networks, and a host of battery vendors including East Penn and Ecoult and Xtreme Power and Invenergy are all providing frequency regulation in PJM today.

While PJM is the first independent system operator (ISO) or regional transmission operator (RTO) to implement the changes ordered by FERC Order 755, others are set to follow suit in the coming year or so. Meanwhile, Texas grid operator ERCOT is looking at creating a new ancillary services program, known as Fast Responding Regulation Service, which would enable energy storage to play a role.

Because frequency regulation is called upon in four-second intervals, it’s well suited to battery technologies that still can’t provide hours and hours of continuous energy at a cost that competes with gas-fired power plants or pumped hydro storage systems. Of course, frequency regulation services make up only a tiny portion of total energy markets, which indicates some natural limitations to growth in these markets.

There’s also a tricky issue in the way that energy storage, demand response and other non-traditional resources work in today’s frequency regulation markets that could limit their growth. Unlike natural-gas-fired power plants that have to include fuel prices and lost opportunity costs in their bids, energy storage and demand response are allowed to bid services at a clearing price of zero, then get paid the highest-priced bid for that moment of time.

But as a Sandia Labs’ September report (PDF) points out, "If there is enough of this energy storage to completely supply the specific ancillary service needed, the market price collapses to zero. With no energy market income to cover capital costs, the storage device is not economically viable even if their total costs are less than the traditional generators’ marginal opportunity costs.” While today’s frequency regulation markets are still far from reaching this point, it’s certainly something that needs to be addressed before it happens.

Opening Up Energy Storage’s Unique Value for Flexible Capacity

This point underscores the fact that energy storage needs to gain access to broader energy markets to grow. While today’s energy markets aren’t configured in ways that take storage’s unique characteristics into account, that’s starting to change -- particularly when it comes to the concept of flexible generation resources to meet future grid needs.

Flexibility, or the ability for a generation resource to quickly ramp up and down, isn’t something that grid operators and utilities have had to worry about for most of the history of the grid. Instead, generation was measured on its ability to either produce baseload power or peak power at the lowest possible cost, whether to meet predictable demand curves through the course of the day, or to supply enough energy to meet predictable growth into future years.

But with the growth of intermittent wind and solar power, “We’re entering a period during which this ‘built-in’ flexibility might not be sufficient to meet variability,” Praveen Kathpal, vice president of market and regulatory affairs for AES Energy Storage, explained in an email. That means “a bit of planning may actually be necessary so that we not only have sufficient megawatts to meet peak, but also have sufficient megawatts that can move up and down.”

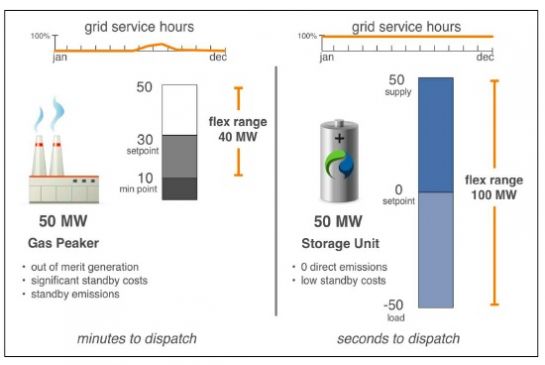

That’s where energy storage’s unique characteristics could play a significant role. Because storage systems can absorb power as well as inject it into the grid, they can effectively double their flexible capacity, compared to a gas-fired turbine that can only produce electricity, not absorb it. And while gas-fired turbines have to run at a midpoint output to be able to ramp down with minutes of advance warning, storage can go up or down within seconds, as this graphic from the Energy Storage Association makes clear:

As Kathpal noted, “The mechanisms used to incentivize megawatts to exist -- capacity markets, long-term planning, PPAs -- are in the process of being modified to account for this new constraint of flexibility.” Specifically, capacity markets, which offer payments to projects that promise to deliver generation resources in years to come, are in the midst of changes to bring energy storage's value to bear.

The first example comes from California, where utility Southern California Edison recently opened up a process to secure 1,400 to 1,800 megawatts of capacity by 2022 to meet needs in the Los Angeles region. Of that, at least 50 megawatts must come from energy storage resources, under order by the California Public Utilities Commission. It’s the first time that energy storage has been explicitly required as a long-term resource of this kind, but given California’s 1.3-gigawatt energy storage mandate, it’s likely to serve as a roadmap for how storage can fulfill that role elsewhere.

Meanwhile, energy storage advocates last month proposed a model (PDF) for including energy storage in PJM’s own capacity market, known as its Reliability Pricing Model (RPM) -- the same market that demand response providers have been bidding into for more than a decade. While PJM’s capacity mechanism require participants to contribute hours of energy at a time, and pay far less per megawatt, it’s roughly 150 times the size of its frequency regulation market.

“From our perspective, it’s about leveling the playing field, opening up all the markets that generators can currently participate in to energy storage resources -- and maintaining flexibility for allowing new technologies into these markets,” explained Janette Kessler, senior vice president of development and regulatory affairs for Demansys, the startup that submitted the PJM proposal.

Finding a way to value flexibility will be critical for energy storage projects to compete in markets like these -- and California and PJM could be the settings for creating models to follow elsewhere. For example, Ontario’s recently released Long-Term Energy Plan will require the region to include 50 megawatts of energy storage in its energy procurement plans starting next year.

Creating new market mechanisms doesn’t just affect regions where ISOs and RTOs set the rules. As Sandia Labs’ report notes:

“Many developers are not willing to take the risk of deploying a relatively new technology without financing from the marketplace. This financing is difficult to acquire for resources participating in the ISO/RTO marketplace, as revenue is not predictable. It is also difficult to acquire in the non-ISO/RTO marketplace as rate base approval from regulators is unlikely due to the uncertainty regulators see with a relatively new technology unnecessarily increasing ratepayer price risk.”

That’s why vertically integrated utilities are eager for markets to establish pricing models for them to follow. If they’re going to ask regulators to approve rate increases for storage, they’re going to need someone to set the rules.

"If you need to have multiple value streams, markets may not have that today," said Jeff Gates, managing director of commercial transmission at Duke Energy, the giant U.S. utility that has does business in both regulated and competitive markets. "Vertically integrated utilities could capture that full spectrum of values, but within the utility, there’s no price signal. How do you put a value on what those benefits are? Part of it is going to be an educational process on the regulator front, sharing the benefits with commissions, and needing some forward-thinking commissions to push storage to be adopted," as is taking place in California, he said.

41

41

15

15

9

9