The U.S. energy storage sector may be booming, but it’s still far from mature. Developers of grid-scale battery projects remain dependent on a handful of markets that offer the right economics and incentives. And when one of those key markets undergoes a significant change in how it values energy storage, that can lead to some outsized impacts to short-term growth.

In the past few months, we’ve seen just this kind of thing happen with mid-Atlantic grid operator PJM and its frequency regulation market. Over the past few years, many of the utility-scale battery projects built in the United States to date have been built to provide fast regulation services in PJM’s territory, stretching from the East Coast to Illinois.

But starting in December, PJM has imposed some interim changes to its regulation markets that limit how much energy storage, as well as other fast-responding regulation resources such as pumped hydro and demand response, can be called upon from day to day, hour to hour, and in 15-minute increments. That means that individual providers in the market will have fewer opportunities to earn money -- although they’ll still be paid the same, generally higher, amount for serving that need.

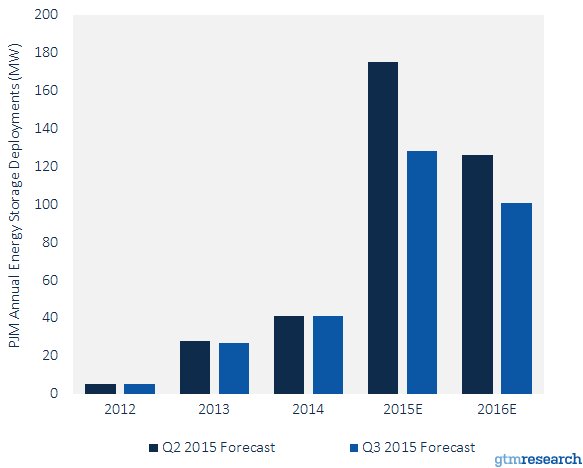

GTM Research took these changes into account this fall, when it lowered its 2015-2016 cumulative U.S. energy storage deployment forecast by 72 megawatts, from 301 megawatt to 229 megawatts, as indicated in the chart below. That’s a testament to how important this market has been for utility-scale storage to date, and how the interim changes are expected to reduce its economic opportunities.

At the same time, PJM is working on longer-term changes to its frequency regulation rules that could help better-performing storage assets win more market share, compared to poorer-performing rivals. Among these changes is dealing with the tricky problem of how to rank lots of resources that are being offered at a clearing price of $0, as energy storage, hydropower and other resources that don't need to burn fuel to operate are priced in today’s market.

In the long run, there are constraints to how much regulation service PJM needs, which will limit the prospects for future growth. GTM Research has been tracking this maturation for some time, as well as charting the next growth areas beyond this early-stage opportunity.

This friction with energy storage at PJM shows the challenge of incorporating technologies that don’t fit into the fossil-fuel-fired system paradigm. And while PJM’s problems and solutions are uniquely its own, they do have significant implications for how different markets in the U.S. and abroad will develop -- which makes them worth breaking down in deeper detail.

The problems that can come with too much of a good thing

We'll start by taking a look at why batteries have been good for PJM’s fast-responding frequency regulation needs until recently -- and how they’re now starting to become too much of a good thing.

PJM, like every grid operator, calls on frequency regulation resources to increase and reduce generation, or inject and absorb energy, to help keep grid frequencies at a steady state, and avoid the “excursions” that can destabilize or even bring down the grid. Traditionally, this has been provided by fossil-fuel-fired generators ramping up and down -- a slow and inefficient resource, compared to the near-instantaneous action of batteries and other fast-responding assets.

In 2011, the Federal Energy Regulatory Commission issued FERC Order 755, which directed grid operators to create a mechanism to provide these fast responders a financial premium over their slower-moving rivals. This led to a boom in energy storage in PJM, which offers the largest market and highest prices for the “RegD” service it created to meet this mandate, as opposed to the slower-reacting “RegA” for traditional resources.

By 2013, one year after PJM implemented FERC Order 755, the amount of RegD resources had tripled, along with a near-tripling of market clearing prices. That helped further encourage development, with 44 megawatts of storage deployed in 2014 and 140 megawatts deployed in the first three quarters of last year, according to GTM Research data.

But in the latter half of 2015, PJM started detecting problems with its frequency regulation operations. As Eric Hsia, PJM’s performance compliance manager, put it, “We saw that at times, the RegD resources and the RegD control signal were moving in the same direction as ACE,” or area control error. ACE is the signal created by sensor data that tells PJM what’s actually happening with grid frequency and interchange, and regulation is supposed to move in ways that help bring it back into balance, not push it out of whack.

Why was this happening? In simple terms, it’s because PJM’s RegD signal includes an “energy neutrality reset” -- a function that allows the batteries and other limited-energy assets that serve the market to recharge. This recharge time is built into the RegD signal, with the goal of achieving an aggregate balance -- no energy lost, no energy gained -- over the course of its dispatch period.

But this means that, at some point during these periods, some resources that would otherwise be asked to discharge energy are actually absorbing it -- the exact opposite of what the grid needs at the time. That wasn’t such a problem when the number of RegD assets was smaller. But in 2015, when some large-scale hydropower and new battery resources came on-line as RegD assets, it became a much bigger issue.

“The RegD signal was designed for energy storage-type resources,” Hsia said. “It never accounted for resources like hydro.” Batteries, which come in smaller megawatt increments, tend to balance out their charge-discharge patterns over time. But individual hydropower units in the hundreds of megawatts, responding to a signal that’s going the wrong way, can cause much bigger problems, he said.

A task force formed in October is working on this problem, which will require some adjustments to how things like signal tuning, benefits factor curve and recharge requirements are dealt with. That task force is expected to have some solutions identified by mid-2016, he said.

But in the meantime, PJM had to figure out a short-term fix to its problems, and came up with this set of adjustments (PDF), which went into effect last month.

The ‘Benefits Factor Curve’ fix -- and its limitations

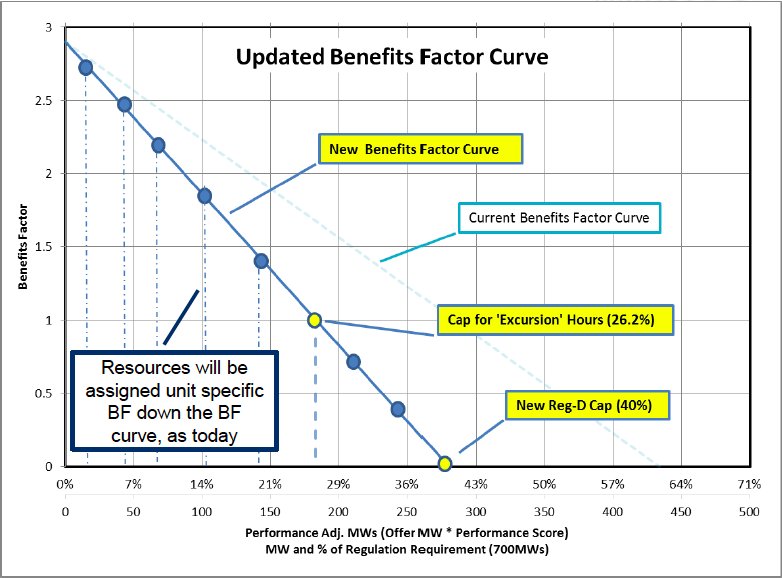

The first part of this interim solution focused on something called the benefits factor curve -- a critical part of how PJM values fast-responding assets, compared to the slower-acting generators that still make up most of its frequency regulation needs. In simple terms, the benefits factor curve determines how much RegD assets it needs in proportion to RegA resources -- and how much better that fast-acting resource is than the slower alternative.

On this curve, anything above a benefits factor rating of 1 indicates that the RegD resource is better than a RegA resource to solve the problem. Anything below 1 means that RegD is actually worse -- mainly, because it adds instability to the outcome.

Back when PJM was first implementing FERC Order 755, it ran a host of simulations to determine how to set the benefits factor curve, explained Sudipta Lahiri, a consultant with DNV GL. “On the earliest simulations, what they determined was that if you had more than 42 percent RegD penetration, there was a negative impact on stability. And at 60+ percent, it was really bad,” he said.

Those findings led to PJM setting its benefits factor curve to 1 at 42 percent and to 0 at 62 percent. In practical terms, that meant that for every 15-minute period it bid frequency regulation, it would seek to acquire at least 42 percent of it from RegD resources, rather than their slower counterparts. For PJM’s on-peak needs, that equated to roughly 434 megawatts of RegD resource with a factor of at least 0, which could technically participate, and about 280 megawatts with a factor of 1 or better that would receive preference in the market.

But with the interim fix that went into effect last month, “They’re moving the curve to the left,” Lahiri said, with 0 set at 40 percent, and 1 set at 26.2 percent. With that change, “They’re effectively reducing the amount of RegD in the system,” he said.

While the exact number will depend on the amount of RegA as a reference point, the new on-peak 0 target would add up to about 280 megawatts, and the 1 target would add up to about 183 megawatts -- quite a bit less than before.

What’s more, PJM has picked several “excursion hours” -- 7 a.m. to 8 a.m. and 6 p.m. to 9 p.m. -- when the system is peaking the hardest, and which showed the most troublesome excursions over the latter half of 2015. During those hours, PJM will limit the amount of participating RegD resources to no more than 183 megawatts or so, or specifically, the amount that has a benefits factor greater than 1.

How this will affect existing battery projects bidding into PJM’s market is hard to predict, according to Kiran Kumaraswamy, U.S. market director for AES Energy Storage, the U.S. market leader in battery-based grid storage projects. “It’s a little early to tell what the changes will mean. PJM is watching the changes to observe how they affect price formation,” he said. He declined to comment on how his company might be adjusting its plans to take the changes into account.

“The key thing to know is that the benefits factor is not used in the settlement process,” he added. In other words, nothing that PJM has done will alter the amount that RegD resources get paid for the services they do provide when they win bids. “All it did was to restrict the number of megawatts.”

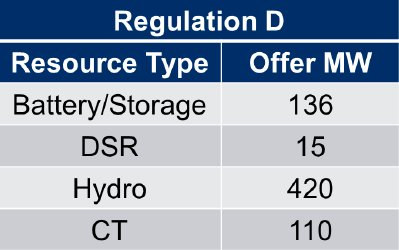

But as DNV’s Lahiri noted, considering that there are about 700 megawatts of RegD-qualified resources competing for a smaller share of megawatts, “If you are participating in the market, you might expect your resource to be dispatched less often than it was earlier."

Using performance to pick the better ‘zero-cost’ resources

Amidst this bad news for energy storage players in this interim market construct, there are other changes that could bring advantages to fast-responding resources like grid batteries -- or at least those that perform well.

That’s because PJM’s other big interim change will begin to assign values to resources that have otherwise looked about the same to its market engines, because they’re all priced at zero cost.

How can a grid resource come with no price tag? Simply put, PJM’s market systems, like those of other grid operators, were designed to manage power plants and other resources that carry a marginal cost, based on the cost of fuel required to generate that megawatt. These units still bid into PJM’s regulation market with prices attached, and those prices help determine how much every market participant ends up getting paid for what they do.

In PJM’s frequency regulation market, things like batteries, hydropower and fast-acting demand response are called “self-scheduled” or “$0 cost offer” resources. Under the previous rules, “When we have resources that offer into the market that self-schedule or have the total cost at zero, the engine would just assign a block benefits factor to them -- it just assumes they’re all equal value,” PJM’s Hsia explained.

That was not an issue in years past, when relatively few zero-cost-offer resources were available. But with the rise in storage and hydropower, “That causes a problem, because if you’re assigning a benefits factor to everything that has a zero cost, you could overvalue resources that have a lower performance score,” he said.

To solve this problem, PJM has decided to use these performance scores to differentiate one zero-cost resource from another. PJM already collects data on how closely different resources follow dispatch signals, and how completely they’re able to fulfill the services they’re called on to provide.

Now, with what it calls a “tie-breaker logic” addition to its software, it will use these performance scores to decide which bidding resources get picked first. “Obviously, the better you perform, the more valuable you are to us,” Hsia said. “We use that as a differentiator to rank the resources and assign the right benefits factor.”

This, in turn, could help battery-based resources gain an edge, since they tend to have a higher performance score than competing natural-gas-fired power plants, AES’ Kumaraswamy noted. “In our view, it’s a good thing -- it’s a reflection of the fact that you’re delivering a lot more value.”

AES research shows that for frequency regulation, battery-based systems offer about three times the benefit of combustion turbine (CT)-based natural-gas power plants, even though those still make up the majority of RegD resources in PJM. AES would like to see that value reflected in the market mechanisms at PJM and other grid operators.

The interim “tie-breaker logic” partly addresses that issue, he said. But a more complete reckoning will come as part of the PJM task force’s work on a longer-term solution, he said -- “They will have to ensure that the full value of these flexible resources will be represented in the markets.”

Moving away from single markets and single applications

It’s important to remember that PJM’s frequency regulation market has already started to approach its limits for new energy storage entrants. After all, the grid operator only needs so much regulation to accomplish its goals, whether from batteries or other resources -- and it’s getting close to reaching a saturation point.

That’s why GTM Research had already projected a slowdown in utility-scale storage projects starting in 2016. Chief energy storage analyst Ravi Manghani noted, “The rule changes in October 2015 put the slowdown on a fast track,” but didn’t change the overall trend.

That’s a predictable outcome, and for AES, it’s been part of how it has approached the PJM markets for some time, Kumaraswamy said. “You’re constantly calibrating yourself with market conditions as you see them,” he said. “When you hit the point where you satisfy the demand, the saturation phase begins.”

“That’s where you start thinking about other high-value services that energy storage can provide,” he said. In PJM specifically, there are emerging “opportunities to participate in the PJM capacity market and serve the capacity needs of the system.”

The same dynamic is likely to play out in other parts of the country. Grid operators only need resources that add up to about 1 percent of their peak loads to meet their frequency regulation needs -- although this figure, like many other grid metrics, may start to grow as more intermittent wind and solar power resources come on-line.

As PJM’s frequency regulation opportunities are waning, however, new opportunities are opening up for energy storage elsewhere. “We're already heading into a market that is larger,” GTM Research Senior VP Shayle Kann said in a presentation at last month’s Energy Storage Summit in San Francisco. “What's changing about that market is that it's shifting from a frequency regulation market, PJM, which means fast-acting [and] low-duration, to a market that is largely dominated by California, where the value proposition is more around capacity value.”

The changes in PJM also highlight an important trend in the energy storage field: a shift from single-purpose projects to those that can tackle multiple propositions. “I think the time of standalone, one-application storage is on the ebb,” DNV’s Lahiri said. “What I think will happen is that more and more storage will be equipped to manage more and more complicated applications.”