The secret behind the latest numbers from the wind industry is that developers, their turbine suppliers and the entire supply chain are running on all cylinders and yet are desperately worried about the cliff out in front of them.

The new numbers from the American Wind Energy Association (AWEA) are impressive. U.S. cumulative installed capacity is at 46,919 megawatts, second only to China (where government support is so good their turbine tower manufacturers stand accused by a U.S. tower maker coalition of unfair trade practices).

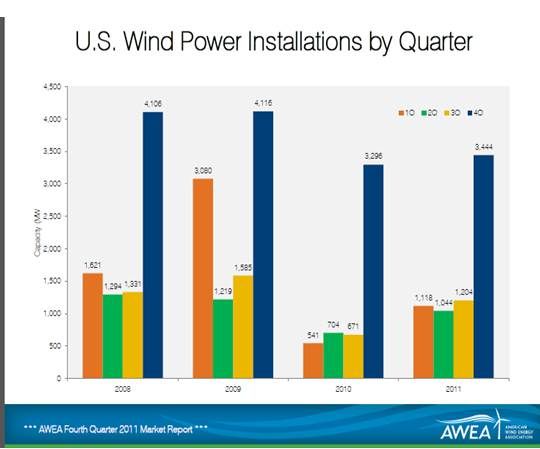

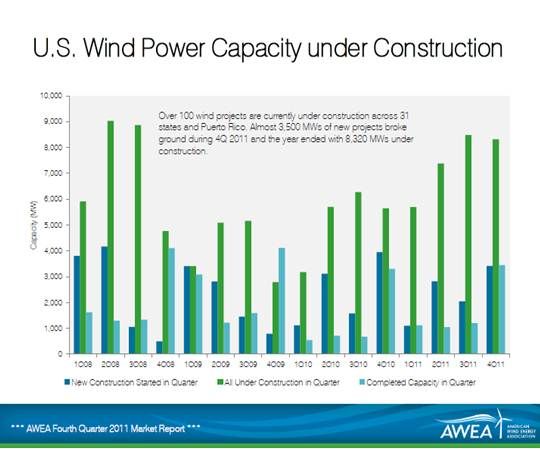

2011’s total of 6,810 megawatts installed was 31 percent higher than the 2010 total. Q4’s 3,444 megawatts beat 2010’s Q4 (3,296 megawatts). And there hasn’t been so much wind capacity under construction since the middle two quarters of 2008, just before the recession hit. This time, however, it is not ambition but desperation that is driving growth.

“This tremendous activity is being driven by the federal Production Tax Credit (PTC), which leveraged an average of more than $16 billion a year in private investment over the last several years and supported tens of thousands of manufacturing jobs,” AWEA CEO Denise Bode observed.

The wind industry’s PTC expires on December 31, 2012. Hopes are high it will be preserved in a tax extenders package due before Congress at the end of February. The 2.2 cents per kilowatt-hour tax credit draws financing to developers from those with big income in search of a tax shelter.

Only financial institutions and other highly capitalized entities have the leverage required for large wind projects that cost an estimated $2 million dollars per megawatt and can run to the hundreds of megawatts.

Congress watchers are split on whether an extension of the PTC will get into -- and stay in -- the tax extenders package primarily intended to address the payroll tax. Side issues in this partisan Congress only make for further contention and gridlock.

Bode stressed the bipartisan support wind has in both houses of Congress, as well as among governors around the country. But, as Jonathan Weisgall, Vice President for federal policy at MidAmerican Energy Holdings (the Midwestern utility subsidiary of Warren Buffett’s Bershire Hathaway) recently told GTM, “deficit reduction has now become a more potent political issue,” adding, “the banner of tax reform does give you a terrific fig leaf behind which to hide.”

President/CEO Richard Morrison of Molded Fiberglass and CEO Terry Royer of Winergy Drive Systems, two prominent wind industry suppliers, sat in on the unveiling of the AWEA numbers. Both said their companies are as busy as they can be right now because developers are working frantically to finish projects by the end of this year (in order to be eligible for the PTC). And both said there is little scheduled beyond this year.

Morrison expressed concern for the jobs of 800 people at his own firm and among the other businesses he deals with. “It’s already very late,” he explained. “We like to take orders for 2013 by the last quarter of 2011.” But the orders, he said, are not there.

Royster said his company has to plan eight to 10 months out. They are planning now for the last quarter of this year. If the PTC is not extended in February, he said, he expects few, if any, orders for Q1 2013 or afterwards.

Wind’s 2011 growth was in traditional wind powerhouse states (Texas, Iowa, California) and in states just emerging as players (Minnesota, Oregon, Washington, Colorado, Illinois). States with strong wind manufacturing bases joined the ranks of the wind building states and showed the promise of more to come (Ohio, Michigan).

Kansas presently has more wind under construction than any other state and looks to be on the list of major players by next year. Developers there also opened up relatively new territory by securing a pair of power purchase agreements (PPAs) to deliver Kansas wind to Southeastern U.S. states where there is practically no wind capacity.

2011’s 79 percent of wind developed under PPAs or owned by utilities was little changed from 2010’s 76 percent. Some predict that number may drop if the PTC is not extended, leaving a perception that wind is less price-competitive than natural gas.

Developers who choose to continue building under those circumstances may “go merchant,” meaning they would test wind’s unsubsidized competitiveness in electricity spot markets.

41

41

15

15

9

9