New York regulators took a step forward this week in properly valuing distributed energy resources (DERs) on the state's power grid — mainly by postponing any big changes for another year.

On Dec. 9, the New York Department of Public Service staff released a white paper, expected to guide a long-awaited decision on the state’s Value of Distributed Energy Resources (VDER) tariff. Created as part of New York’s Reforming the Energy Vision proceeding, VDER is meant to replace solar net metering with a new rate that takes DERs' locational and time-based value into account — at first for larger-scale solar projects but eventually for mass-market solar as well.

But according to the white paper, mass-market solar customers aren’t ready to take that step — at least, not by next year.

In a move being hailed by solar advocates, the Department of Public Service (DPS) staff’s primary recommendation was to extend the deadline for shifting mass-market residential and small commercial solar customers from the existing net metering regime to the new VDER rates from Jan. 1, 2020, as is now the plan, to a year later.

The other option would have been new rates proposed by New York’s utilities, using a combination of demand charges, direct customer charges and time-of-use rates.

As with similar efforts in states like California and Hawaii, the ultimate goal is a system that avoids net metering’s effect of shifting fixed costs onto non-solar customers, while also taking DERs’ positive impacts into account — and, most importantly, doing so transparently and with real data.

But despite New York’s VDER ambitions, most of its utilities — Con Edison, Central Hudson, National Grid, Orange and Rockland, NYSEG and Rochester Gas & Electric — haven’t deployed smart meters yet. That means they don’t have the 15-minute interval data needed to accurately forecast and analyze just how new rates would affect customers in the real world, the white paper notes.

This “lack of existing customer interval data presents a barrier to sizing DER solutions and estimating adopting customer economics,” DPS staff wrote. Indeed, this lack has plagued many of the Reforming the Energy Vision (REV) effort's more ambitious plans to measure, monitor and reward DERs for their value to the distribution grids they’re connected to, as we’ve highlighted in past coverage.

And while New York’s utilities are deploying advanced metering infrastructure, until those meters have been in place for at least a year to establish that interval data set, “more time is needed to unlock the full suite of rate designs envisioned,” the white paper notes.

That’s why Monday’s white paper suggests extending old-fashioned net metering for mass-market customers, but with a small monthly charge as “a fair and simple way” to “reduce the identified cost shifts” from net-metered customers to all others. This Customer Benefit Contribution could range from 70 cents to $1.10 per kilowatt of installed solar capacity, or about $4.40 to $6.60 per month.

This new cost is bound to be opposed by solar customers and advocates on some level, but according to the white paper, it will have only a slight negative effect on solar economics, at most lengthening the payback time on a system by about 8 percent. The new fee is also smaller than the cost shifts of about $19 to $44 per month that came out of the DPS’ VDER Working Group Regarding Rate Design — although it’s important to note that those costs don’t include the value of distributed solar for carbon reduction, or the broad set of social benefits to come from that.

In that light, the proposed monthly charge received a relatively neutral reception from the Solar Energy Industries Association. In a Tuesday press release, Dave Gahl, senior director of state affairs for the Northeast, stated that “SEIA is still analyzing how the charge will impact New Yorkers’ ability to choose solar and will submit comments in advance of the final decision in early 2020.”

More importantly, however, Gahl praised DPS staff for “rejecting more complicated rate design changes that would not have been workable at this point in time.” Instead, the white paper suggests “modest changes to solar rate designs and recommends an extension of net metering until 2021, both of which will provide certainty to solar companies in the state.”

Looking back at VDER’s evolution and breakdown

To understand this state of affairs, we must look back at how New York’s efforts at creating a VDER tariff have been plagued from the near-inception by conflicts between solar industry and utilities over the true value of DERs.

These struggles aren’t unique to New York, of course. California has faced similar challenges, as have states like Hawaii, Arizona, Massachusetts and others seeking to integrate DERs at scale. But in New York, the lack of smart meter data has led to a fundamental disconnect between REV’s ambitions to measure every aspect of DERs' value to the grid and society at large, and the ability to achieve them.

This reality has pushed regulators and utilities to create VDER rates largely aimed at larger commercial and industrial customers that already have interval meters. These have resulted in what New York calls the “value stack” for DERs, which “provides monetary crediting for net hourly injections based on the actual values created, including the energy, capacity, environmental, and distribution system values.”

There’s no love lost between the solar industry and New York regulators and utilities on this new VDER rate, which has applied to all large-scale commercial and community solar projects since the end of 2017. New York’s first rollout of VDER early that year was warily welcomed by the solar industry, largely because, once again, it extended net metering for mass-market residential customers, instead of subjecting them to the new rates.

But solar groups reacted with alarm in September 2017, when DPS issued its final order for VDER rates. This order exposed commercial and community solar developers to new values such as marginal cost of service, demand reduction value, and locational system relief value, that varied widely from utility to utility, shifted from hour to hour, and were otherwise difficult or impossible to accurately model for would-be investors in projects.

The effect was to stall community solar in New York. “Because the underlying value components are variable and include differing term lengths, investors have remained skeptical about financing projects with such volatile revenue streams, and consequently very few on-site projects are being built,” Wood Mackenzie Power & Renewables stated in a summer 2019 research note.

Community solar fixes are possible — but DERs are a different challenge

Things have gotten better for community solar in New York. In April, DPS issued revisions to its VDER tariff that made several changes welcomed by the solar industry, including a new “community credit” that enables large commercial customers to act as an anchor tenant for community solar projects otherwise serving residential customers.

The April revision also made changes to how demand reduction, locational system relief and capacity value are measured and calculated as part of the value stack, to make them “more predictable and transparent through changes to performance windows and term lengths,” WoodMac wrote. While the details are complex, the result has been a much easier pathway to financing and an increase in forecasts for New York’s C&I solar market.

Even with these changes, the "value stack" model could prove daunting for solar investment planning, and it is unlikely to appeal to all but the most sophisticated solar customers.

In fact, this week’s white paper proposes that net-metered customers have the option to choose these value stack rates instead of being grandfathered into the old system, and they can avoid Customer Benefit Contribution charges as a result. But this “may require the installation of more advanced meters and concomitant fees” to support the vastly more complex billing required.

At the level of mass-market rate policy, back in 2017, groups including SEIA, the Natural Resources Defense Council, Vote Solar and the Acadia Center protested that the DPS’ plans could allow “flawed utility proposals that undercount the value of solar resources” to become part of ongoing plans replace net metering. But as the white paper makes clear, the rate designs that emerged from this process over the course of 2018 and 2019 have yet to meet REV’s standards.

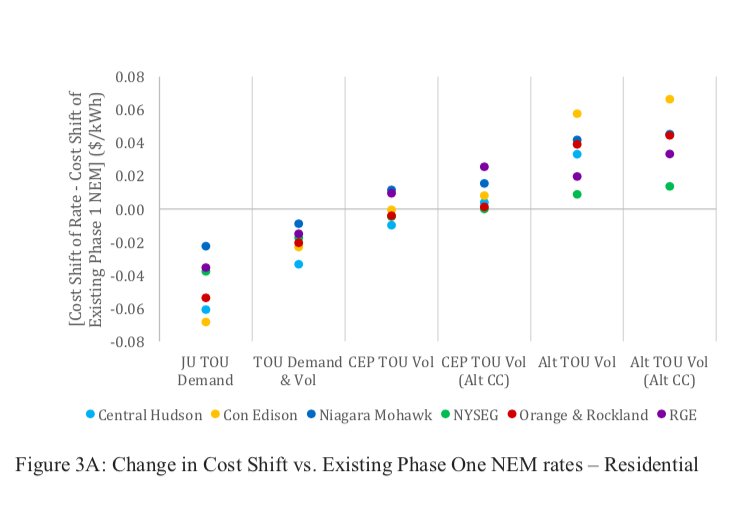

The white paper provides a detailed analysis of the rates proposed by utilities, clean energy parties and DPS-staff-offered alternatives. While the results are too complex to summarize in print, this chart indicates that plans reliant on demand charges tended to shift more costs onto solar customers, while those that rely on time-of-use rates tend toward rewarding them.

Whatever their potential impact, all of these rates are built on systemwide data, estimates and averages, and other workarounds to the fact that New York simply doesn’t have the interval data required to make more informed analyses and decisions.

This doesn’t bar net-metered customers from signing up for new rates being made available by New York’s utilities, the white paper emphasizes. Mass-market customers may be interested in signing up for existing time-of-use plans or the “standby” rates for on-site generators now being revised by the New York Public Service Commission.

But for more complicated tariffs, “REV principles call for customer choice and technology-neutral rates,” the DPS staff stated. “Meeting these principles requires access to data to enable customers and vendors to make economically efficient choices.”

For now, at least, New York’s mass-market customers — and the regulators tasked with protecting their interests — don’t have that.