The U.S. renewables industry was left out of the $2.2 trillion coronavirus stimulus bill passed last week, but the battle is far from over.

Congress is already considering further legislation to rescue the economy from the ravages of the COVID-19 pandemic, and renewable energy groups are ready to bring their proposals back to the table.

As with the last stimulus bill, the industry's plans center on securing changes to two federal policies: the Investment Tax Credit (ITC) for solar power and the Production Tax Credit (PTC) for wind power.

Renewables groups have a powerful claim to make as they push for those changes: Unlike many of the industries seeking hundreds of billions of dollars in collective aid, the desired tweaks to the renewable tax credits would not add significantly to the federal government's costs. The government would not be adding any new payments to solar and wind companies or increasing the scope of the tax credits already set to expire under current law, advocates say.

Instead, they’re focusing on two key concepts. The first is extending "safe-harbor" deadlines for receiving the credits that may be thrown off track by the pandemic’s economic disruptions. The safe-harbor fix could potentially be made by the Treasury Department, without a need for congressional action.

The second is allowing renewable projects to receive some of their tax credit value back as refundable credits or via "direct pay" provisions. This is meant to counteract the fact that tax equity investors are likely to have lower tax liabilities amid an economic downturn and thus less “tax appetite."

The ostensibly revenue-neutral aspect of these two requests could help differentiate solar and wind from requests for support in other areas like energy storage, and energy efficiency and electric vehicles. President Donald Trump and Senate Majority Leader Mitch McConnell (R-Kentucky) opposed efforts to put clean energy support into the last stimulus package, incorrectly conflating them with the Green New Deal and other proposals from House Democrats.

“Making these adjustments to existing tax credits would provide the industry the flexibility needed to accommodate COVID-19 delays, without costing the federal government any additional money,” Tom Kiernan, CEO of the American Wind Energy Association, said in a statement last week after the first stimulus package passed.

Not taking these steps, by contrast, could lead to significantly greater economic and job losses in two industries that have been growing faster than most other sectors of the economy, Abigail Ross Hopper, president and CEO of the Solar Energy Industries Association (SEIA), said in an interview this week.

"This is not a theoretical threat. This is happening now," Hopper said, pointing to a recent survey showing significant sales declines and layoffs in an industry that employs about 250,000 in the country.

The safe-harbor fix

The pandemic has disrupted manufacturing and shipping, slowed progress on meeting permitting and other regulatory hurdles, and forced many employees to stay away from work to honor government stay-at-home orders. All of these delays are “having the effect of calling the 'safe harbor' into question,” Hopper said.

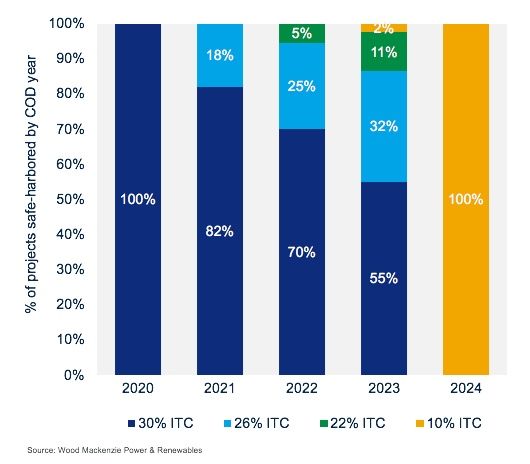

According to the currently scheduled phase-down of the solar ITC, developers can claim the full 30 percent ITC available for 2019 if they incurred at least 5 percent of a project’s cost by year-end 2019. Many developers achieved this by procuring equipment by the end of last year. To fully qualify, the taxpayer must either transfer title of the equipment or take physical possession within three and a half months of payment, or by mid-April.

“This is causing both uncertainty and potential cancellation of projects,” Hopper said. “We did ask Congress to legislatively extend the amount of time you would have to qualify for safe harbor,” which would provide breathing room for under-the-gun projects.

In the absence of congressional action, “alternatively we think that Treasury could issue some clear guidance that the coronavirus affirmatively qualifies as an excusable disruption” to meeting that deadline, she said. This step could be accomplished through guidance from the U.S. Treasury Department, bypassing the need for legislation. "We continue to be in conversation with Treasury about it," Hopper said.

Such a move by the Treasury Department “would be a huge source of relief for any projects that safe-harbored modules last year but haven't yet transferred title or taken physical possession,” said Michelle Davis, senior solar analyst for Wood Mackenzie Power & Renewables. According to WoodMac data, almost all utility-scale solar projects set to be built this year, and a majority of projects planned through 2023, have used the safe-harbor provision.

The country’s biggest residential solar companies that operate under third-party ownership models, such as Sunrun, Vivint, Tesla and SunPower, have also safe-harbored a large portion of modules for installation over the next three years. Now, both solar markets may face challenges in ensuring that each project retains the 5 percent share of solar modules or other equipment required to meet the safe-harbor provision’s legal terms.

For wind power, the term "safe harbor" applies not to when projects are started but when they’re completed. To be able to earn the full 100 percent PTC for the power those wind farms generate, worth roughly $24 per megawatt-hour over 10 years, projects begun by the end of 2016 must show “completion of construction” by the end of 2020.

For its part, then, the wind industry is seeking a two-year extension for projects facing coronavirus-related delays to forestall even more from failing to meet it. Wood Mackenzie has already warned that many U.S. wind projects are at risk of missing the 2020 deadline.

The tax-equity fix

Tax credits for the wind PTC are based on how much power those wind turbines generate and are paid out over 10 years, while those for the solar ITC are based on the upfront cost of installations and are paid based on the year those solar systems are placed into active service.

But both are reliant on a key source of investment that may be harder to come by in a time of economic downturn: the banks and financial institutions that provide the tax equity investments needed to turn those credits into project finance.

“As the economy is challenged, and as there’s a tightening of the tax equity market, there are concerns whether there is going to be adequate tax equity to finance these projects,” SEIA’s Hopper said. The renewable energy industry saw a similar problem emerge during the Great Recession of 2007-2009 when appetite for credits to offset tax liabilities among would-be investors dried up. That led the federal government to launch the Section 1603 grant program to cover the difference.

Today’s renewable energy sector is much larger and stronger than 10 years ago, and the solar and wind industries aren’t asking for another grant program for help. Instead, they have "asked Congress to make that tax credit either refundable or direct-pay,” Hopper said.

While each of these methods would work slightly differently, both would have the effect of allowing projects to claim credits in excess of tax liability, she said. But either one would require legislation to enact.

While converting tax credits to direct payments or refundable credits would lead to checks being mailed to companies approved to receive them, those payments wouldn’t be any larger than the tax credits that would have otherwise been claimed, Hopper said. In that sense, moving to direct payments should be relatively revenue-neutral, Hopper said.

WoodMac’s Davis noted that tax-equity investments make up roughly one-third of the “capital stack” of typical utility-scale solar projects, with debt and equity from long-term project owners making up the remaining share. The relatively small pool of tax equity investors in U.S. solar projects has grown modestly over the past few years, with more financial institutions seeking the increasingly lucrative returns available in the sector — a trend that’s also brought down the costs of tax equity financing from the perspective of solar developers.

At the same time, solar tax equity investors are “in this business because it’s lucrative, it gets high returns and it doesn’t take very long,” she said. Investors receive their full tax credit in the first year and typically remain for another five or six years to capture accelerated depreciation benefits before transferring their ownership to other parties.

How the broader economic problems caused by the global coronavirus pandemic alter this equation is hard to predict. “Obviously we’re in a recessionary period right now,” David said. WoodMac is projecting a 2 percent decline in U.S. gross domestic product for 2020.

“There’s no doubt that this will lead to less tax equity being available in the market,” she said. But, she added, “I don’t think tax equity will disappear. In the shorter term, it will probably mean that tax equity gets more expensive. Investors will be more cautious; they might not want to do deals that are on the fringe — and they might try to demand higher returns.”

***

Two new research insights from Wood Mackenzie outline how U.S. residential solar and utility-scale solar will be impacted by the coronavirus pandemic.

41

41

15

15

9

9