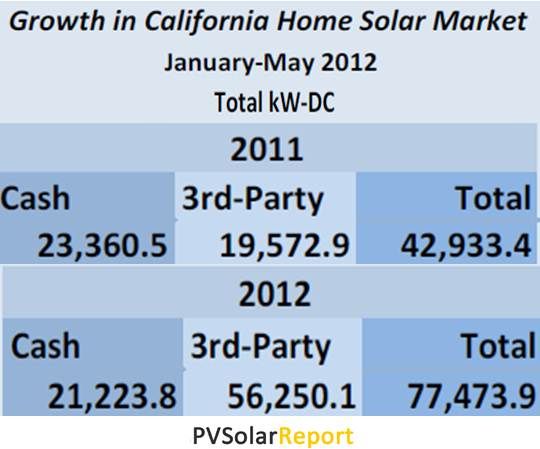

California, which represents 40 percent of U.S. solar, went from 42,933 total kilowatts installed in the first five months of 2011 to 77,473 in the same period of 2012. But kilowatts installed with cash went down from 23,360 to 21,223, while kilowatts installed using third-party financing nearly tripled from 19,572 to 56,250.

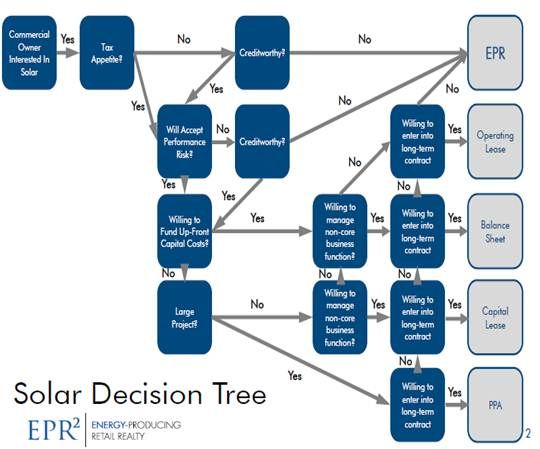

Yet 90 percent to 95 percent of commercial building rooftops remain essentially beyond the reach of third-party financing, according to real estate research firm data cited by Energy Producing Retail Realty, Inc. (EPR Squared, EPR^2) Founder/CEO Chris Pawlik.

“When you have a commercial building with multiple tenants,” Pawlik said, third parties “can’t technically finance those unless the owner takes it on, [and] commercial owners won’t do that.”

Third-party financiers, he explained, “can get an agreement signed or financing in place because they have the credit of the off-taker that takes care of the risk.” With a twenty-year commitment, third-party financiers have certainty that their loan will repaid.

But, Pawlik said, “owners typically own properties five to seven years and tenants are typically in properties five to ten years. You can’t have a ten- to twenty-year agreement in situations like that.”

Pawlik’s “real estate structure” resolves the impasse. “We develop a real estate interest on site and have that be separated from the land and the improvements, through a legal method that has precedent in real estate.” It is similar to agreements with property owners for cell tower and billboards, though, Pawlik stressed, the solar legal structure is not identical.

DLA Piper, which Pawlik called “the gold-standard, top-tier law firm” for commercial real estate, “has finalized the form documents we need to take to the owners to show them how this structure would work.”

EPR^2 has “a dozen or so deals in the pipeline with groups that have either portfolios of properties or single properties,” Pawlik said. The first deal, he explained, must be one that demonstrates to the 60,000 California real estate brokers, agents and mortgaging agents that “this is almost identical to a real estate transaction.” When they see commissions in it for themselves, he said, “we can really scale the idea and bring it to a size at which pension funds and insurance companies will start looking at it.”

Institutional investors, Pawlik said “love the fact that EPR is a hard asset and an inflation hedge linked to electricity prices.” But the opportunity, he explained, must be very large before it attracts investment from them.

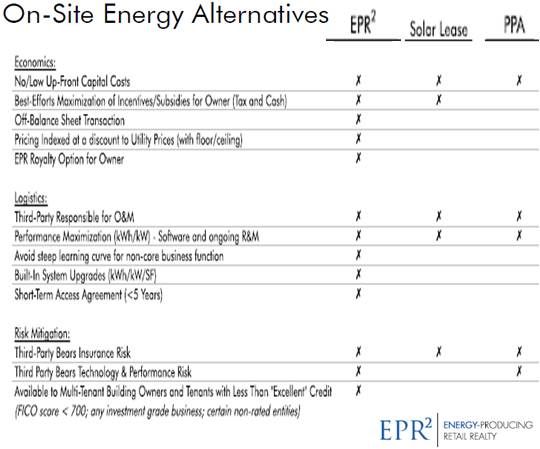

EPR^2 can take it there, Pawlik said, because the legal structure “gives the owner an operating expense reduction or a cash flow increase” and because investors’ returns “are on par with what real estate, infrastructure and renewable project investors are currently receiving but we’re providing them with a better risk profile.”

Pawlik is not a solar developer. EPR^2 will “work with the best-in-class EPCs [engineering, procurement and construction providers] and contractors that have much more experience” and will be only “the real estate and finance specialist in putting these transactions together.”

From preliminary discussions, there are “most likely” EPCs he could not yet name, Pawlik said, but “we can do more deals with others.”

The revenue stream that comes from tenants’ service payments, Pawlik said, “covers the returns demanded by our investors; it covers a spread for the owner of the property, and it covers the development costs and fees.”

According to Pawlik, solar’s obstacle has been, “How do we drive liquidity? How do we make people buy in?” The problem, he explained, is not returns or technology. “The real estate structure is not working.”

EPR^2 is “addressing the obstacles for owners and tenants and making sure the investors are getting a similar type of asset as they would if they were investing in a commercial building.”

Using “real estate structures that already exist, the revenue comes from either the owner or tenants paying for something they are already paying for, but at a discount. Those revenues are distributed to investors and the owner of the property.”

EPR^2 earns “the development fee for putting the deal together,” Pawlik said, but “we are working with our investors to provide them with a preferred return. We potentially participate on the up side, [and] if it works out as good or better than we expected, everybody makes more money.”

By properly sizing the system to its real estate setting, Pawlik said, the building needn’t stay atypically occupied or be in any way different from any commercial property. “We might be producing 10 percent to 50 percent of the load on the building. The building would have to go 50 percent to 90 percent vacant for us to have an issue.”

Pawlik mentioned he had pitched his concept to SunEdison founder and solar industry graybeard Jigar Shah. It is, Shah observed to GTM, an “interesting concept,” but, he said, he has “no idea if it will work. The concept is modeled on another effort he had previously undertaken that worked and is still working now.

“Our next step is to finish the development process with an owner to show how we intend to benefit the property and benefit them,” Pawlik said, “and then take it to other owners and take it across entire portfolios. We are at the edge making the leap.”

41

41

15

15

9

9