VC investment in solar power is still going strong, despite a dismal 2009 and an only slightly more heartening first quarter of 2010.

But the sub-sector of thin-film solar is a different story. In 2007 and 2008, almost every energy and greentech investor invested in a thin-film firm. In fact, they did so in a big way -- with $100 million plus funding rounds going to Nanosolar, HelioVolt, AVA Solar, MiaSole, Sulfurcell, SoloPower, etc.

Here's a quick (non-exhaustive) list of thin-film PV firms funded by VCs over the last few years.

All told, more than $2.5 billion went into thin-film solar over the last few years.

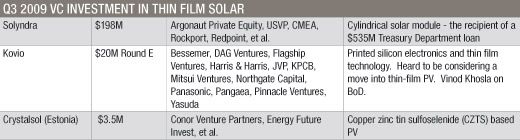

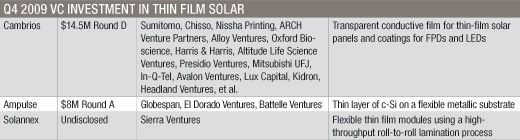

However, investment activity slowed down considerably in 2009 and early 2010. Here are the thin-film solar firms that were funded in 2009:

What does this mean if you're a thin-film PV entrepreneur in 2010? For one, it means the days of $300 million factory-building funding rounds are pretty much over. Two, you're going to have to come up with a new way of doing business. One startup that gets this message is AQT, a CIGS developer that has made enormous technical progress on a shoestring budget with a business plan that doesn't require half a billion dollars to get to market. We've written about them here.

A few of the things that AQT has chosen to do differently are:

- Focusing on building solar cells, not manufacturing equipment

- Using pre-existing high-volume manufacturing equipment

- Starting with CIS2 (Copper Indium Sulfide), a relatively less complex materials system before they tackle CIGS

- Ramping up in 15-megawatt to 20-megawatt modular increments, not biting off 50MW-100MW chunks like other CIGS players

Call it CIGS or Thin Film 2.0.

On the other hand, the companies that ramped-up and staffed-up hard in 2008 have bloated headcounts and a rapidly contracting runway on which to get to market. Their burn rates are either going to get them to commercialization -- or consume them.

41

41

15

15

9

9