In the current political and economic environment, fossil fuel investments are looking much more risky than at any other time in history.

There are at least three good reasons why. First, as climate change worsens, policies are likely to be put in place to constrain emissions. We could see this begin domestically with strict enforcement of the Clean Air Act. Second, whether or not large-scale coal retirements happen, the capacity market isn’t particularly friendly to new fossil fuel generation. In fact, the U.S. has a surplus of generation and dramatically underutilizes existing capacity. And for the first time, fossil fuels have a host of increasingly competitive alternative investments that include efficiency, demand response, solar, and wind.

Let’s be clear: fossil fuels used to be great investments.

The utility business is a pretty sweet gig. The have a locked-in consumer base on the electricity grid, and a guaranteed annual rate-of-return from ratepayers. They just have to acquire and deliver the fuels, and coal and gas have offered the path of least resistance. Coal prices have been kept dirt-cheap through fire-sale approaches to federal lands, and natural gas is benefiting from decades of government investment in hydraulic fracturing technology that have unlocked huge reservoirs of cheap gas. Capital costs for investment have historically been relatively low. To top it off, there is a built-in steady revenue stream over 35 years from utility bills, which is great for leverage in the financial world.

And the dollars have flowed in. The massive build-out of natural gas infrastructure in the late 1990s and early 2000s, and the incredible amount of consistent investment in coal, shows that people have been all too willing to lay down their dollars on fossil fuels.

As climate change worsens, policies are likely to be put in place that will constrain emissions. This could start domestically with strict enforcement of the Clean Air Act.

Climate change is a compounding, progressive problem. While no one can argue that governments across the globe have endorsed anything like an actual solution, eventually something will have to change. A good near-term example of this in the U.S. is rigorous enforcement of the Clean Air Act. Finalizing the carbon pollution standard for new and existing power plants would make coal less economically viable.

This being the case, some are making the argument that fossil fuel assets are incredibly overvalued. The organization You Sow, for example, has an entire initiative devoted to discussing the financial risks of coal. They argue that we are seeing a “carbon bubble” in the industry that will eventually have to pop, leaving stranded assets. How big is this bubble? The Union of Concerned Scientists found that 18 percent of the nation’s coal stock, about 59 gigawatts, is “ripe for retirement,” and Deutsche Bank Climate Advisors found that up to 50 percent, or about 150 gigawatts, could go offline if the carbon pollution standards go through.

With or without these coal retirements, the capacity market doesn’t look great for fossil fuels. The U.S. has a surplus of generation and dramatically underutilizes existing capacity.

If EPA regulations on existing and new power plants go through and we see massive retirements in coal -- to the tune of 150 gigawatts or so -- doesn't that mean lots of new plants have to be built? Yes, some new plants will be built. But not nearly as many as you might think.

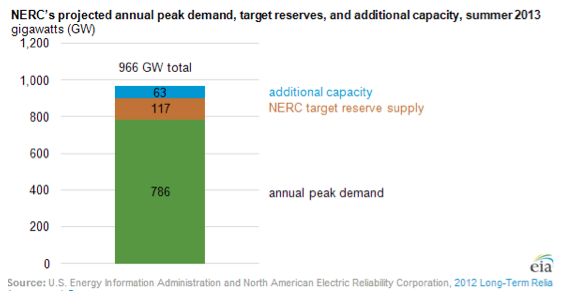

There is a surplus of generation already in the system, most of it new. The EIA notes that there is about 63 gigawatts of spare capacity above and beyond what is needed to meet both peak demand and our capacity margin. That 63 gigawatts of spare capacity could easily soak up some retirements, putting the maximum would need to be replaced closer to 90 gigawatts.

Second, it is much more economical to increase the utilization of existing plants than it is to build new ones. This is because putting new plants in the power pool means it will take longer to recover investments. Although where a plant is located can change how profitable it will be, this holds true as a general rule across the fleet.

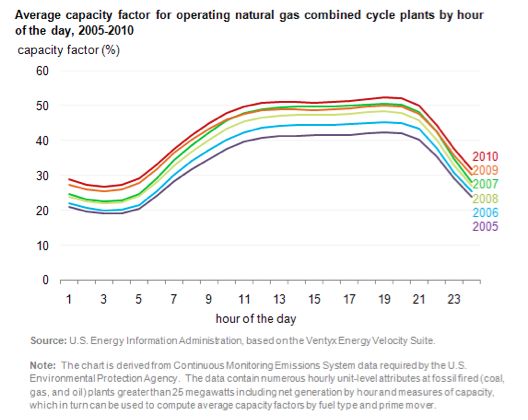

One way to understand this dynamic is by looking at capacity factors, roughly understood to be the rate at which plants are utilized. Coal is operating at a capacity factor of about 66 percent and natural gas plants have been operating barely at 50 percent.

This means that natural gas could easily increase its capacity utilization by eight percentage points to pick up the slack from coal retirements. And, this kind of increase in utilization would fit in with the trend that’s already underway: the upward pressure on their capacity utilization from 40 percent to 50 percent over the 2005 to 2010 time period (as shown by the neat rainbow of lines below) reflects a change from using natural gas primarily as peaker resource to using it more as a baseload resource. Basically, we would see this line getting pushed up even more as these natural gas plants meet new baseload power requirements. The remainder could be replaced by either 33.5 gigawatts of new natural gas capacity, or a combination of efficiency, demand response, solar, biomass, and wind.

Third, it must be said that peak demand could easily be much lower than currently projected. Demand response, aggressive efficiency investments, and solar deployment could all shave peak demand, lessening the need to build new plants.

Finally, for the first time in history, there are a host of increasingly competitive investment alternatives to fossil fuels.

When fossil fuels were the only game in town, they were a much safer bet. Now, there are a few different routes investors can take.

Increased investments in efficiency are much cheaper per kilowatt-hour than any investment in any resource, including fossil fuels. As is often said in the utility sector, the cheapest power plants are the ones you don’t have to build. With a variety of financing techniques that pay for the upfront capital costs in exchange for long-term repayment out of the utility bill, efficiency can lower demand and become a viable investment strategy. Investments in solar qualify too -- with solar panel prices at record lows and new financing models in place, it has never been easier for third-party investors or big utilities to get a piece of the action. Demand response can similarly benefit consumers and investors by aggregating reduced demand and dispatching it like a generation resource.

If the EPA rules do not go through, fossil fuel investments may still look attractive. But there is significant excess capacity (63 gigawatts) in the system operating at relatively low capacity factors. On the other hand, if the EPA rules on stationary sources do go through, there is an open market share of about 33.5 gigawatts. And those investments will be made in a policy environment where companies may be forced to internalize the costs of carbon. In that world, fossil fuel investments are far more risky -- particularly when efficiency, solar, and demand response are all options on the table.

***

Adam James is a Research Assistant for Energy Policy at the Center for American Progress and the Executive Director of the Clean Energy Leadership Institute. You can email him at [email protected] and follow him on Twitter @adam_s_james.

41

41

15

15

9

9