There is no sign that solar will boom anytime soon in Texas. That, according to SunEdison (NYSE:WFR) Government Affairs Director Maura Yates, is a market failure.

Though its energy entrepreneurs have built over 12 gigawatts of wind and pushed through massive new supporting transmission since the renewable portfolio standard (RPS) was passed in 1999, Texas has less than 140 megawatts of installed solar, among the lowest of Sunbelt states, according to the GTM Research/SEIA U.S. Solar Market Insight 2012 Year in Review.

Texas' solar irradiance and available acreage, according to Texas Renewable Energy Industries Association (TREIA) Executive Director Russel Smith, make for big solar potential.

“When the wind and transmission were being built to meet the RPS, wind was cheaper than solar. The installed cost for solar was $8 per watt,” Yates said, but the average price for a commercial solar system in Texas has fallen 20 percent in the last year to $4.14 per watt. The residential price has dropped 14 percent to $5.46 per watt.

Yet commercial and utility-scale solar still cannot compete because wind and natural gas are driving prices so low there is “a resource-adequacy challenge,” Yates said. “The market isn’t sending the right signals for investors to invest.”

This market distortion has left Texas dangerously close to peak period supply shortages. Solar could help meet those shortages. “On an LCOE basis, solar is competitive with peak power prices,” Yates said. “But solar is all upfront capital and no variable costs.”

The deregulated Texas “energy-only” market pays only the price of the supply at the point where it is delivered, Yates explained. What solar needs is a “capacity market.”

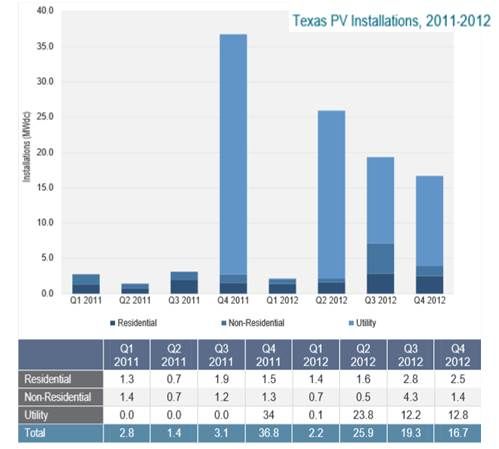

Source: U.S. Solar Market Insight 2012 Year-in-Review

The market is the way it is because, until a few years ago, conventional generation was the only energy being deployed, Yates said. SunEdison supports market-based pricing and a competitive marketplace. But new technologies need new grid and generation considerations.

In the Texas energy-only market, Yates explained, energy is traded on a real-time basis. The assumption is that the market will make its needs known.

For solar, variable costs are zero, but there is a multi-million-dollar upfront capital investment. Financing is particularly difficult with very low natural gas prices and already built wind sometimes selling at negative prices to recover its production tax credit (PTC).

Locational marginal pricing (LMP) allows some price consideration for solar’s ability to be where the demand is, Yates acknowledged. And there have been times, particularly in 2011, when the need for peak period electricity was so great that solar captured very high prices. But those moments were far less frequent in 2012.

In 2011, a solar generator bidding into the ERCOT real-time market would have received a market clearing price of roughly $70 per megawatt-hour instead of the market’s overall $40 per megawatt-hour average price because the generator sells during the highest demand periods, Yates said. "This is not equivalent to a PPA price and does not imply solar’s costs could have been financed at $70 per megawatt-hour," she exlplained. It just means that in a merchant market solar clears at a weighted LMP (about $70 per megawatt-hour in 2011), not an average LMP (about $40 in 2011).

But there is no certainty of how many peak demand megawatt-hours can be sold at the higher price. That variability makes it “nearly impossible to finance a solar plant in an energy-only market,” Yates said. “We have talked to our finance partners. It is too risky.”

Investors want a return on those upfront capital costs, Yates continued. “But in an energy-only market, there can't be twenty years of guaranteed revenue at the right IRR that would justify the investment.”

A capacity market gives value to having the capacity available, Yates explained. “It provides guaranteed payment streams for the reliability factor, for the certainty that kilowatt-hours are available when peak demand hits.”

Investors can then finance “off of the certainty that a solar project’s high upfront capital cost will be covered by a predictable revenue stream,” Yates said.

It is not a power purchase agreement (PPA), she noted. Such “bilateral agreements with utilities” remain possible, if difficult, at current prices.

But a capacity market allows a company like SunEdison “to work with the financial markets to determine if a one-year or three-year capacity payment is enough to get them to invest, especially if they know on the back-end there will continue to be a capacity market to bid into.”

SunEdison’s 75-megawatt installed capacity in Texas has been built with twenty-year utility PPAs from Austin Energy and CPS Energy, but, with a capacity market, Yates said, solar can deploy through both the merchant and utility models.

Along with TREIA and other solar advocates, Yates and her team are working toward a capacity market in Texas. But they are also working to develop new financial products “within the existing market rules and structures” to lure investors.

“We have to stay nimble,” Yates said. “I call my team 'The Mad Scientists.' We know the market. We understand our product’s risk. We have to innovate.”

41

41

15

15

9

9