Money is available for utility-scale solar photovoltaic (PV) and concentrating solar power (CSP) projects, bank officers from CITI and Deutsche Bank said, but it is vital to know how to leverage every kind and source of financing.

It’s called financial engineering and it is the only way to fund big solar projects, CITI Managing Director and Alternative Energy Finance Head Marshal Salant insisted at the Smithers APEX solar event in San Diego last week.

The key differences between PV and CSP, Salant said, is that “PV can be done on a much smaller scale and be economic, and a large project can be done in phases. It’s a lot easier to finance $250 million or $500 million than it is to get $3 billion all at once.” CSP requires vital economies of scale “so you’ve got to raise $2 billion all at once. That’s a lot harder to do than to raise $500 million four times.”

For either technology, “the real mission is to obtain the lowest-cost capital,” Salant explained. That means “you want bank, bond, LOCs, fixed rate, floating rate, guaranteed, non-guaranteed loans,” he said. “You go wherever you have to go to find investors. It’s that simple.”

Things are more difficult now, he said. “1603 is gone -- that was the most successful program Washington ever came up with.” CITI’s deal makers, a big and dedicated team that covers every aspect of financial engineering, Salant said, are turning to any and all federal, state and local programs, and “the funky structures, the partnerships, leveraged leases and inverted leases,” as well as “tax equity and project level equity.”

And, Salant said, “financing is more than ever about serious corporate relationships.” Everybody involved has to be invested. CITI is “absolutely adamant about this,” because “the days of casual dating are over -- we’ve got to deal with people where it’s a serious relationship.”

It is vital, Salant warned, to “focus on interest rate risk, because if the Fed starts to tighten, the whole project can wither and die.” Commodities and foreign currency must be hedged, he added. And “on big solar projects, tax-exempt bonds are essential.”

“In this market," Salant said, “size matters. The way you’re going to do a small deal is very different than the way you’re going to do a big deal.” CITI focuses on “super-large deals,” which it defines as $1.5 billion and bigger. “In 2010, we did the two largest financings in alternative energy. They both were wind deals. In 2011, we did the largest deal, a solar deal -- Desert Sunlight. In 2012, we hope to again do the largest deal, which will again be a solar deal.”

Salant described the many parts of the 550-megawatt PV Desert Sunlight deal involving NextEra, GE and First Solar.

It was the “largest solar energy project financing to date, a $2.3 billion project with $1.7 billion of market financings.” CITI “locked in 4.27 percent as a blended cost, which I would argue for a long-term, non-recourse project financing is amazing, given that the Treasury, for most of the last twenty years, couldn’t finance at 4.27 percent.”

CITI has also “put over $200 million of our own money” in $100-million-or-less residential rooftop deals. “We’ve done five portfolio deals for SolarCity, Sungevity, Constellation Energy, SunEdison and SunPower,” said Salant. “We do stuff as principal. We also find investors. The long-term key is finding investors.”

The company's 2012 undertaking is the 550-megawatt, $1.2 billion Topaz Solar PV project, which has “$850 million in project bonds.” They are, Salant said, “ten-year Treasuries with basis points, 5.75 percent on a $2.4 billion project -- again, very large bond deals.”

The markets, Salant insisted, “are wide open. Deals are bankable. But they have to be well-structured.” Capital “in the bank market is relatively strong.” Though some institutions are reluctant, “the bond market side continues to grow.” And, he added, “long-term, the solution is not banks.” That is, he said, “an historical accident. The right source of long-term capital is equity capital. It’s bond and institutional investors.”

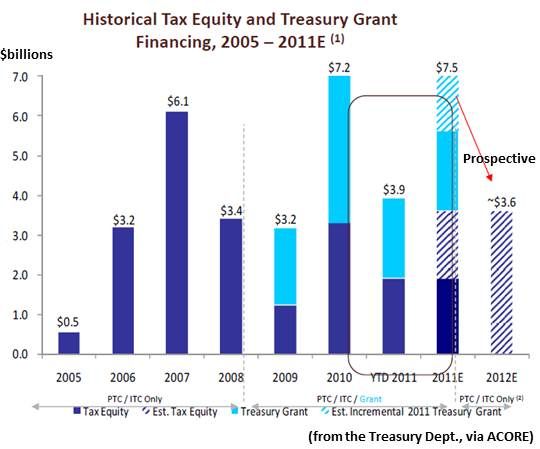

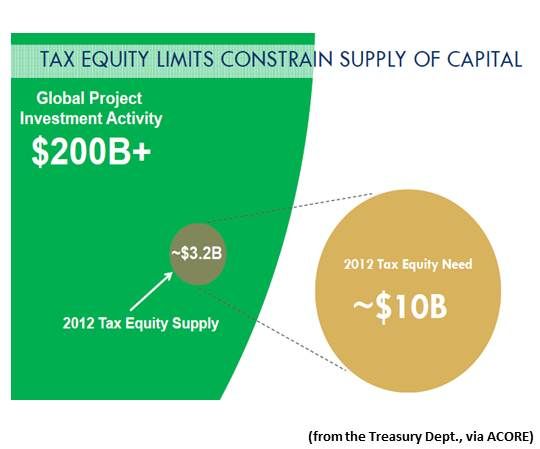

Right now, Salant said, “tax equity is available” but “there is a supply-demand imbalance.” CITI calculates there is a need in solar for $10 billion to $12 billion in tax equity for 2012 through 2014, but not more than $5 billion in tax equity is available. That, Salant said, is “a massive supply-demand imbalance” that is not “going away anytime soon.”

On policy, Salant said, “I personally am an optimist.” But, he added, “You better start prioritizing and focusing on legislative policy objectives because it is going to be a difficult fight in Washington for limited funds.”

Sitting in was Stoel Rives law firm partner Morten Lund. “I am a professional pessimist,” he explained. “There is lots of money available” and “projects are being financed,” he agreed, but “only the good guys are getting the money.”

Financing is hard, Lund insisted, because big projects come with big challenges, and “that’s not the kind of conversation you have with a bank.” What he does all day, Lund said, “is tell people it’s really hard.”

Money is available, Lund concluded, “if your project is good -- and only if your project is good. Therefore, be a good project. That is the very simple and straight road to financing.”

***

Coming in Part 2: the perspective of Deutsche Bank Director Vinod Mukani

41

41

15

15

9

9