There are various companies large and small that are eyeing the smart building market. A handful of them are the international incumbents that serve the bulk of the market, with a myriad of startups at their heels.

But what sort of market are all of these companies serving? It depends on what you mean by "smart buildings," and it depends where on the globe you’re sitting.

According to a new report about smart buildings and the smart grid by Memoori, a market research firm based in the U.K., a smart building is “one that will create the greatest synergies between energy efficiency, comfort, safety and security, which turn buildings almost into living organisms: networked, intelligent, sensitive and adaptable.”

That’s a high bar for smart buildings, but the report goes further to specify that a smart building in the commercial sector will need “Direct Digital (DDC) fully automatic controls for the monitoring and control of the environment in the building.”

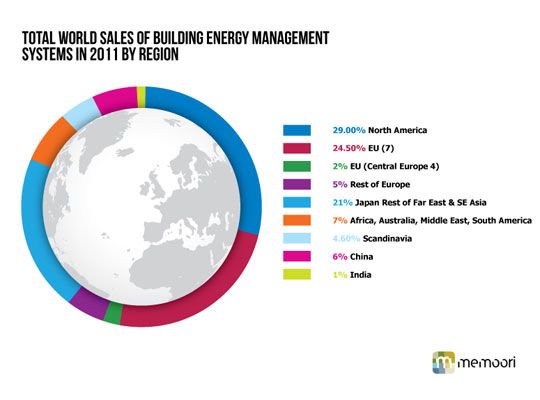

The market for smart buildings, as defined as the market for energy management systems and DDC controls in industrial and commercial facilities, is largely in North America and the European Union at this time.

Looking at the market for smart buildings and grid-side connections, the report estimated that the current spend is not likely to exceed $100 million. That echoes the sentiment of many others in the industry who see a disconnect between the millions being spent in smart grid, only to interface with 'dumb' buildings.

The average spend on both the building management systems and any grid-side updates that allow for two-way communication is expected to be about $1.5 billion in 2017 and peak in 2020 at $2.2 billion.

The EU market is primarily in western Europe, according to the report, including Belgium, the Netherlands, France, Germany, Italy, Spain and the U.K. The EU and Scandinavia already have a higher penetration of BMS than North America, which is why the market opportunity is greater in North America.

As with every other market, China and India are growing the fastest, and are expected to sustain 15 percent to 20 percent growth rates through this decade.

Although China is growing the fastest, Japan, Korea and the rest of Southeast Asia are projected to have far higher rates of sales of building energy management systems in the next five years. China currently has 6 percent of the world market, compared to 21 percent of Japan and Southeast Asia.

The report also broke down BMS sales by building types worldwide. Offices, education facilities and healthcare facilities made up nearly half of the total sales, with government and financial buildings coming in after that. Although many companies tout the need for sensors in hotels, where guests are prone to just leave everything on when they walk out of the room, hotels and catering made up only 4 percent of the market as of 2010.

It was more difficult to find regions where there are significant numbers of smart grids and smart buildings. However, many northern European countries have relatively broad smart grid goals and are further along than North America with penetration of BMS in commercial buildings. In the U.S., the authors estimated that there are at least 40,000 commercial buildings that would be a prime target, given that they’re in an area with a lot of smart grid activity.

There are dozens of startups looking to get into this slowly expanding market, but that has also compelled the incumbents to pick up M&A activity in this space. With emerging communications standards for activities like demand response, and a growing focus on energy benchmarking, the market is changing. Just maybe not as quick as some would like it to.

“The smart buildings technology landscape is getting more competitive by the day,” the authors conclude. “This is good news for end users as vendors compete to bring the most productive and cost-effective solutions to the market.”

41

41

15

15

9

9