It's the first day of Greentech Media's biggest solar event, U.S. Solar Market Insight, and more than 400 executives from the solar industry are gathered in San Diego, Calif. to look at 2015 and figure out what's ahead in 2016, 2017 and beyond. We'll be reporting from the event all week (and live-streaming the action to our growing group of GTM Squared members).

Shayle Kann, GTM's VP of research, kicked off the festivities this morning with a look at how soon the U.S. solar market might grow another order of magnitude -- from about 25 gigawatts to 250 gigawatts installed.

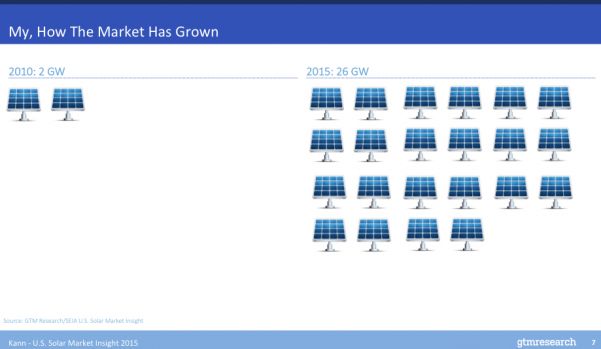

There were 2.5 gigawatts of solar cumulatively installed in the U.S. in 2012. In 2015, the U.S. will install over 7 gigawatts and hit a cumulative 26 gigawatts. That's "a full order of magnitude in five years," said Kann.

Can the U.S. grow the solar market another order of magnitude? What will it take to get the U.S. to 250 gigawatts of installed solar capacity?

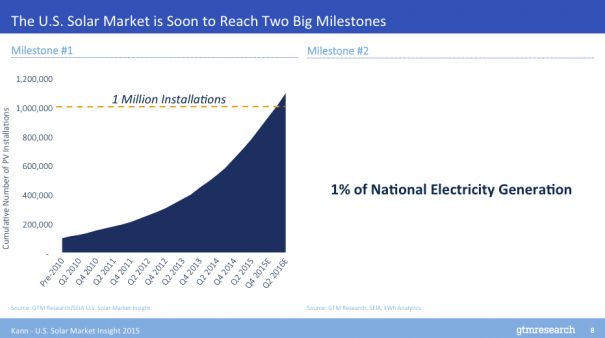

From a milestone standpoint, Kann points out that the U.S. will energize its millionth PV system sometime in early 2016. He notes that solar now makes up 1.6 percent of U.S. generating capacity and will soon will hit 1 percent of total generation.

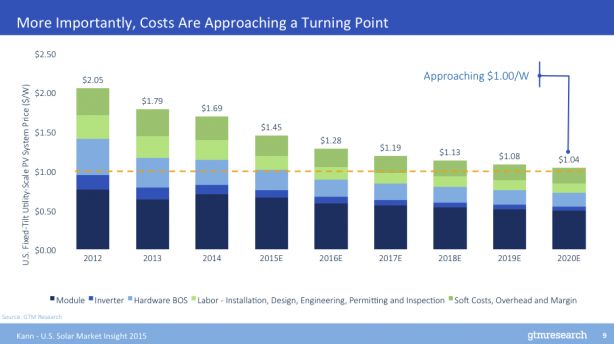

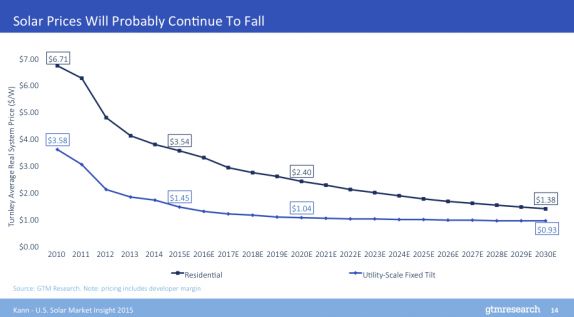

As for the $1.00-per-watt DOE SunShot goal for fixed-tilt utility solar set in 2012, "the reality is we're going to get very close," said Kann, adding, "We're hearing about systems in the Southeast [that are] already approaching $1.00 per watt."

"There was a period when I think you could make a pretty cogent and well-supported argument that solar was going to be a temporary phenomenon in the U.S. that was driven by incentives, and a polysilicon glut drove prices down...I think we're past that now, and part of what that means, ultimately, is that the solar industry should be thinking in slightly longer terms than it's used to. I think we spend a lot of time, particularly in the U.S. solar market, thinking about the next quarter, or the next year, or the next incentive reduction, and indeed, we need to do that."

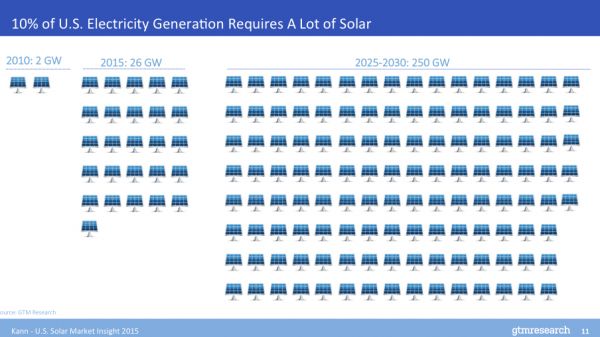

But Kann suggests, "I think it is time to think about the next order of magnitude." He said that if the market installs, on average, 15 gigawatts per year, the U.S. will hit 250 gigawatts in 2030. At an average of 22 gigawatts per year, "We'll hit it in 2025."

That 250 gigawatts could be roughly 10 percent of total U.S. generation. "What is it going to take to get to 10 percent?" asked Kann.

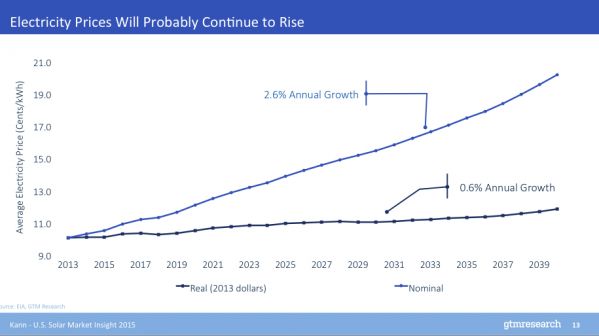

Kann points out some of the tailwinds for this growth, the first being that "electricity prices tend to rise." He notes that electricity prices have risen faster than the rate of inflation in the U.S. The Energy Information Administration expects a 2.6 percent increase in utility price costs through 2040.

That "will make solar look more and more attractive," according to Kann.

Solar costs will likely continue to behave as they have in the past. GTM Research looks far out into the future to estimate residential solar costs of $1.38 per watt in 2030 and $0.93 per watt for utility solar.

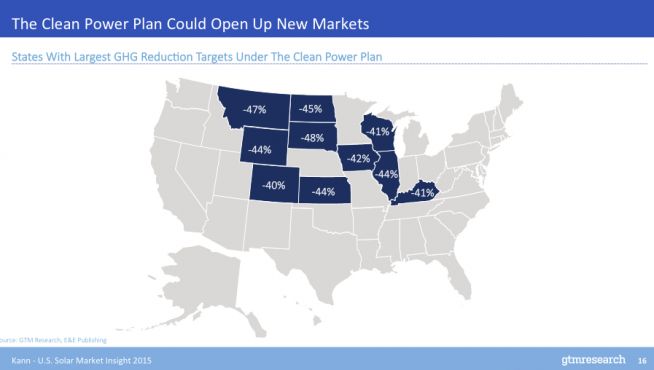

The Obama Clean Power Plan (CPP) could help open up new state solar markets.

The federal effort enlists the states to craft their own implementation plans. And the 10 states with the highest CPP targets (except for Colorado) are also the states that have no solar market to speak of -- accounting for a total of just 1.4 percent of U.S. solar capacity. Kann said, "The states that have to make the most drastic changes are those that haven't had a traditional solar market."

Kann points out that the U.S. market is still geographically concentrated -- with California holding 50 percent of the market and 10 states installing 90 percent of all solar. Kann contends that the U.S. cannot reach 250 gigawatts if the market remains concentrated in just a few states.

The structure of the CPP could also act as an obstacle to solar growth by delaying plan-compliant installation of solar until after 2020.

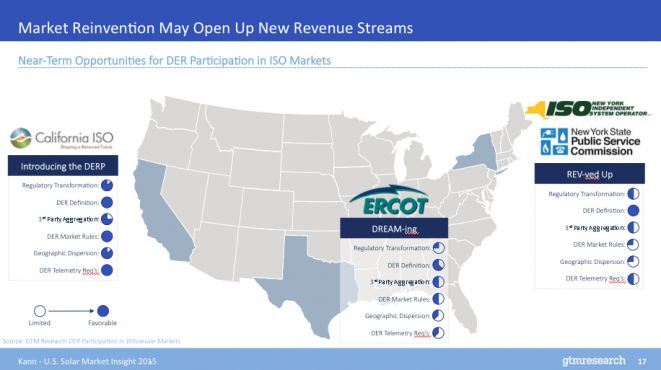

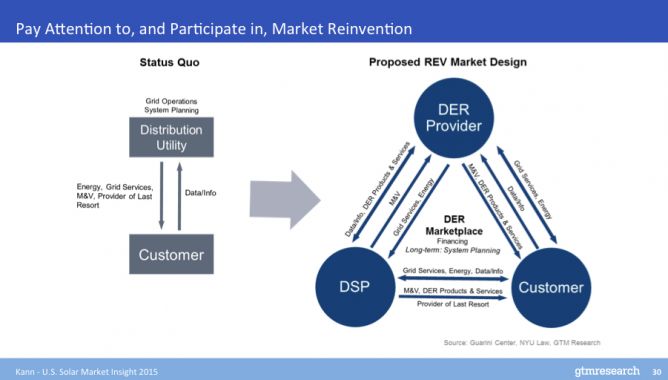

Another positive factor that could impact solar growth is what Kann called "market reinvention." Already happening in New York, California and Hawaii, and to a lesser extent in Minnesota and Texas, regulatory proceedings across the U.S. are looking hard at the edge of the grid where the customer meets the utility. "Largely, what these proceedings are trying to do is figure out ways to make distributed energy resources, which includes solar, fully valued and monetized within the electricity market, so that it can be sited where it's the most valuable, and so it can get value out of that and provide services to the grid."

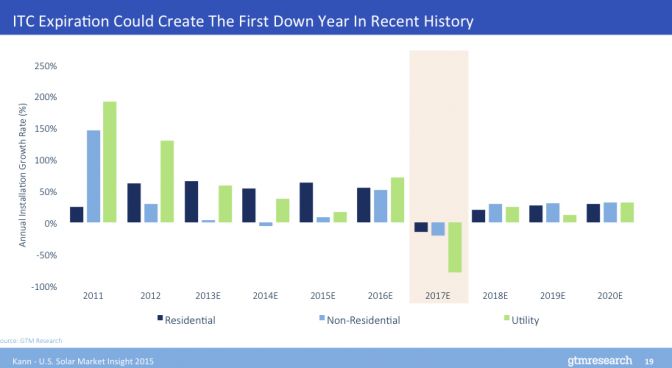

As for the sunsetting federal Investment Tax Credit, the GTM Research VP said, "The reality is, nobody knows what it's going to do to the market. We spent so much time forecasting this, and running project models, and trying to figure out exactly how it's going to impact the market."

"The economics in 2017, unless everything goes right, are going to be worse than they are in 2016, which is something that we basically haven't seen in the solar industry in the U.S. in 15 or 20 years. The result of that is likely to be the first down year for solar that we've seen in the last 15 to 20 years in the U.S. It may not be the end of the market. Growth may continue thereafter, but a down year is something we're very much not accustomed to, and it's going to be particularly painful in states, markets and utility areas that are...on the margin of profitability."

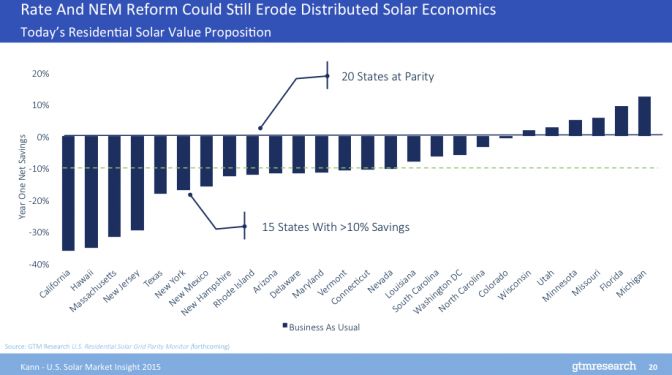

"You can't talk about potential barriers to solar, particular distributed solar and particularly residential solar, without talking about reform to rate structures and reform to net energy metering. We've been covering this and paying attention to it for years now, and largely speaking, the solar industry has come out mostly unscathed thus far, in the many, many regulatory venues where there has been some proposed reform to rates or net energy metering," Kann said.

He continued, "If you model out projects, and we're looking at a project that has a real customer load profile, real electricity rate structure in the largest utility territory in each state, and we model it out for 50 states, we're basically trying to say, 'Given a 20-year customer contract, can you offer a customer a year-one net savings?' Which is the equivalent of saying, 'Are you at grid parity?' This includes all state-level incentives and all federal incentives."

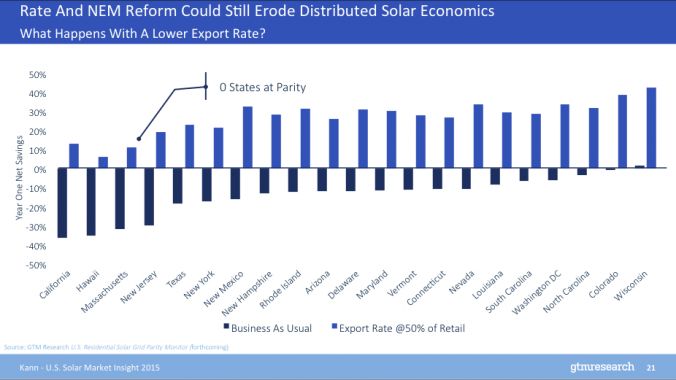

But, asked Kann, "What happens if you change the economics by changing net energy metering?"

He continued: "Hawaii is the first example of this. It's changing the net-metering rules so that the export, when you generate power that's fed back into the grid, is compensated at something less than the retail price.

In Hawaii, it ends up being about half of the retail price, closer to the wholesale and the generation price."

"What happens if you take all those states, then you change the export rate to make it about 50 percent of retail? Again, this is basically what's been implemented already in Hawaii with a grid supply tariff. It's also more or less in line with what the IOUs have proposed in California in the NEM 2.0 proceeding. What does that do to the economics in all of these places?" Kann asked.

"The answer is that it basically takes every single state out of parity. Hawaii is close, and I think in reality, the Hawaiian market is not going to disappear tomorrow as a result of this, but it's hard to make the economics work today anywhere else. In reality, it won't go quite this drastically," he said.

Kann gave another example playing out in the Salt River Project utility territory in Arizona. "SRP introduced a higher fixed charge and a demand charge, one of the first residential demand charges in the country. SRP was running at about a pretty consistent 10- to 12-megawatt per quarter clip for residential solar, right up until those charges started to take hold...at which point we drop to 3 megawatts of residential solar installations, about a 75 percent decline quarter-over-quarter. These things do matter, and over time, can still erode the economics of residential solar."

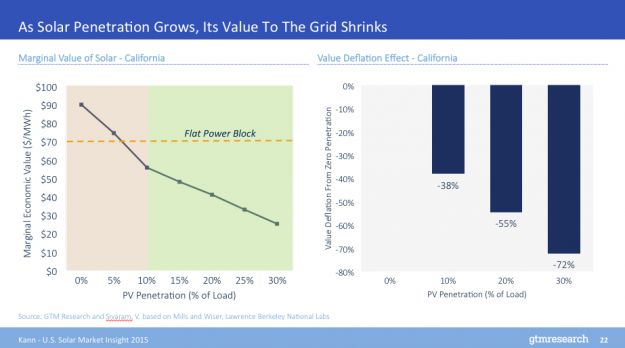

Kann described a process he calls "value deflation" and its effect of solar at higher penetration. "Basically, it's a pretty simple concept. As solar penetration grows, the next kilowatt-hour of solar that you put on the grid becomes less valuable than the one before it."

"The other way to look at this is value to the grid. When you have more solar penetration, you don't need as much generation at the times when solar is generating: the middle of the day," he continued.

Kann went deeper. "A Lawrence Berkeley National Lab study [focused on] modeling out a grid that's supposed to look like California, and then taking solar at various levels of penetration and looking at the marginal value that it provides to the grid. It starts out more valuable than a flat power block. In other words, the first bunch of kilowatt-hours of solar, megawatt-hours that are generating, are more valuable than just something that is generating a fixed amount all the time. It starts out really high, but very quickly, as you get to higher levels of penetration, it falls below the flat power block, and then continues to fall, and you get to this point where relative to zero penetration, the value of solar is down something like 40 percent at 10 percent penetration, and as much as 72 percent at 30 percent penetration. As solar's penetration grows, it's going to become less valuable to the grid. There's basically no way to avoid that."

Kann added, "Grid parity for solar is a moving target, and it may not move in the direction you want it to move over time."

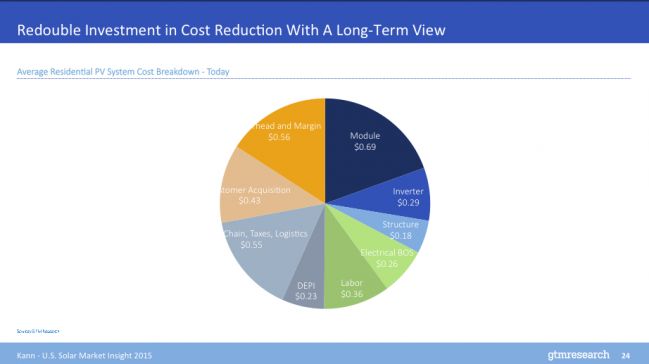

Kann showed an average $3.50 per watt costs for residential systems, broken down into its composite parts. He said, "There are some pieces of this that are sort of ridiculous. The soft costs in particular are completely crazy for solar in the U.S. We're still at over $2.00 a watt on average for soft costs for residential solar, and particularly, customer-acquisition costs, which on average are [around] 43 cents a watt. (Actually, if you look at SolarCity's earnings, they're at something like 60 cents a watt and flat.) It's not falling. Those are crazy-high customer-acquisition costs. The customer-acquisition cost for competitive retail electricity is the equivalent of 2 or 3 cents a watt. It's nothing compared to this, so the first thing we can do is figure out radical ways to get soft costs down."

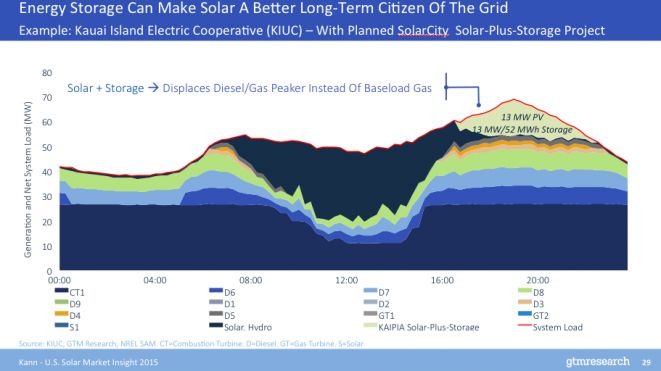

"The solar industry is and should be excited about the long-term prospects for energy storage, and I can give you a very real-world example. We're going to look at a typical day's generation in Kauai. The island of Kauai in Hawaii is run by Kauai Island Utility Cooperative. This is how the generation mix looks over the course of one day [October 14 of this year]," he said. "It starts out where there's basically one baseload gas plant that's operating pretty much all day, and then a bunch of smaller diesel plants."

There are about 21 megawatts of solar in KIUC territory.

"Already, you can...see the impact that all of this solar and hydro is having on the market. It's pushing down in the middle, and you're slightly under-utilizing the baseload gas already, today. A couple of months ago, KIUC announced a contract...with SolarCity to build a 13-megawatt solar project attached to a 13-megawatt, 52-megawatt-hour lithium-ion storage project. Why did they do that? Imagine first if KIUC had just contracted for 13 megawatts of solar alone? It just pushes down in the middle of the day. That means you end up under-utilizing the baseload plant even further. That's expensive. It's also not optimal from a greenhouse-gas-reduction standpoint. It doesn't actually take away that much of the diesel, which is really what you want to be getting rid of. It just doesn't provide that much value, and it doesn't help you in the evening, when you need it. In reality, had it not been for the possibility of storage, I think you can pretty safely say KIUC wasn't going to contract for any more solar, so we would have hit the penetration limit in KIUC territory, or at least very close to it. Instead, they get the solar-plus-storage project," Kann said.

He continued: "Basically, what they're going to do is they're going to take all of the solar generation in the middle of the day, they're going to charge the battery, and they're going to shift it all out into the evening peak, from about 5 p.m. to 10 p.m., and put all that generation there. Instead of stressing that baseload plant, it ends up generating right when you would have had the expensive peak in resources, and a lot more diesel use, so it's good from a greenhouse-gas-reduction standpoint, and it saves you a lot more money."

"This is...a micro-example of what's going to be a macro-trend here, which is that as solar grows in penetration, you're going to see more places that start to look closer to Kauai. We're not going to get anywhere on the mainland that looks like Kauai tomorrow, but if you're treating Hawaii, as a lot of people like to call it, as a postcard from the future, this is a real fact here. At the end of the day, storage is probably the primary mechanism to mitigate the value-deflation effect on its own."

"It's important for the solar industry to pay serious attention to energy storage, even if you don't think you need to do it today, just because of the value it will have in the long term. Finally, I think it's important for the solar industry to recognize how transformative some of this market reinvention that we're starting to see in places like New York can be for distributed solar. New York is, under the Reforming the Energy Vision initiative...trying to completely re-envision the way that electricity is delivered and the role that the customer plays," Kann said.

"I think this world of, we sell solar to a customer [and] the customer gets bill savings based purely on the rates and full retail of net energy metering, in 10 years from now, that's going to look unfamiliar to us. I think the way it's going to look then, is you may still be able to offer a customer savings, but you're also going to have the option to add on [other] technologies to make their generation more controllable. You may be able to change their load as a result of all of those things. You may be able to be aggregated with a bunch of other homes, businesses or buildings that are bid into a market and get additional value. That may be revenue shared with the customer. It may be revenue that's just passed through to the customer in the form of a lower bill. I don't really know how it's going to play out, but I do know that these markets are actually changing in a meaningful fashion, in a way that will impact solar, [not only in] terms of the economics, but also where it's deployed," he continued.

"At the end of the day, a lot of these things are about providing data to third parties so that they can make smarter decisions about where to site things like solar where they will have the highest value to the grid and the highest value to the system. That's going to change the paradigm of how we acquire customers, and find them, and what we offer them, so it's important to pay attention to those markets, because they will dictate the way in which solar is deployed over the longer term," Kann said.

"We already know that there are 13 gigawatts of solar ready to come on-line [in the U.S.] next year, maybe even more. There are still new PPAs getting signed for 2016 right now. This is an enormous amount of solar we're going to be building out next year, completely unprecedented in this country's history," he said.

Kann noted, "There may be a shortage of EPCs. There are people talking about an EPC bottleneck. There may be a run-up in prices for some components. There may be interconnection delays that could cause some projects not to qualify for the ITC, where they would have otherwise, so we have 14 months ahead of us that are just utter craziness, unless the ITC gets extended before then."

"Then, assuming the ITC doesn't get extended, we have a weird period for 2017 to 2019, when we're going to be trying to figure out how to make this market work, potentially in the absence of a 30 percent ITC. There's going to be a heavy focus on cost reduction to make sure the economics still pan out, and the need for a lot of smart strategy to figure out exactly how to right-size your operation, how to right-size your business, and where to be playing strategically so that you can still get these projects done," he said.

Kann spoke of a "next phase" starting in 2020, "one that gets really exciting." He suggests that many of these forces will "come to fruition" during that period and "will change the nature of the electricity market" with "new opportunities for solar providers to introduce new technologies, new deployment mechanisms, new financing mechanisms to make that market work."

41

41

15

15

9

9