As is well known by now, this year is likely to go down as one of the PV industry’s finest. After growing “just” 25% to 7.1 GW in 2009, 2010 should witness least 14 GW of installations (possibly as high as 16 GW, depending on how good greed gets in Germany) -- a year-on-year increase of 93% to 125%. This has meant rosy days for most suppliers for the better part of the year; almost all bankable module producers have been sold out for 2010 as early as the first quarter. Consequently, wafer, cell, and module prices, which had been in free-fall for much of 2009, have stabilized across the value chain, and actually experienced a slight increase mid-way through 2010.

Beyond 2010, however, things get murky -- every pundit, market researcher, hedge fund, and European Photovoltaic Industry Association on the planet has their own view on demand, and the variance is quite significant: forecasts for 2011 installations range from slightly down, to flat, to another 2010-like doubling. Our internal view at GTM Research is that demand for PV over the next two years will indeed continue to grow, but at a significantly slower pace, as large subsidy cuts in 2011 and 2012 will cause Germany to lose much of its luster as an attractive PV market. At the same time, Germany should still be a 5-GW-plus market in these years, and strong growth in the U.S., Italy, France, Canada, China, and Japan (as well as secondary markets such as Bulgaria and Belgium) will in part make up for this. Net-net: 2011 demand is currently forecasted at 15 GW in 2011, only 6% higher than 2010, stepping up into 17% to 19% from 2012 onwards. As demand growth slows and low-cost, bankable producers continue to announce large capacity expansions (e.g., First Solar, Solarfun, and you can bet that Trina, Yingli, and Suntech will be doing the same on their upcoming earnings calls), the next few years are likely to see looser supply-demand dynamics (although nothing as extreme as Q1 2009), and more heated competition between suppliers (for a more detailed exposition of why 2011 is likely to be different from 2010, see this article).

To gauge competitive dynamics, one needs to develop a quantifiable metric that incorporates all the relevant factors that come into play when a prospective module buyer makes his or her decision. At the first order, these are (i) cost, (ii) efficiency, (iii) bankability, and (iv) performance, or kWh/kW yield (not always necessarily in that order). In other words, you need to estimate module manufacturing costs by company, and then adjust these for differences in the other three areas. You also need to know how much available module supply each company is capable of contributing. In other words, you need to construct an efficiency/bankability/performance-adjusted supply stack (or bid stack) for module suppliers. In GTM Research’s latest annual report on the global PV supply chain, this is exactly what we set out to do.

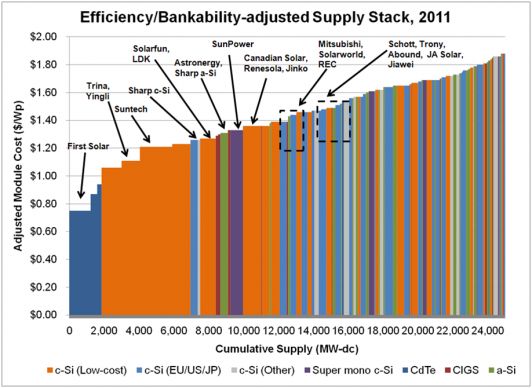

The figure below presents the supply stack for 2011: it shows how much cumulative module supply (X-axis) comes in at or under a specific adjusted cost (Y-axis). As seen, the most competitive firms are the low-cost, bankable players such as First Solar, Trina, Yingli, and Suntech. In all, these suppliers will account for about 6 GW of supply in 2011, leaving the remaining 9 GW of the projected 15 GW to be competed for by the likes of the medium-cost but eminently bankable Sharp; SunPower; Tier 2 Chinese supply (Canadian Solar, LDK, Solarfun, and Jinko); higher-cost c-Si firms such as SunPower, Mitsubishi, Solarworld, and REC; and thin film firms such as Astronergy, Sharp (a-Si), Trony, and Abound. Some CIGS firms, as indicated by the red blocks, will be competitive (e.g., Solibro, Solar Frontier), but still will not be at sufficient scale to pose a competitive threat in 2011.

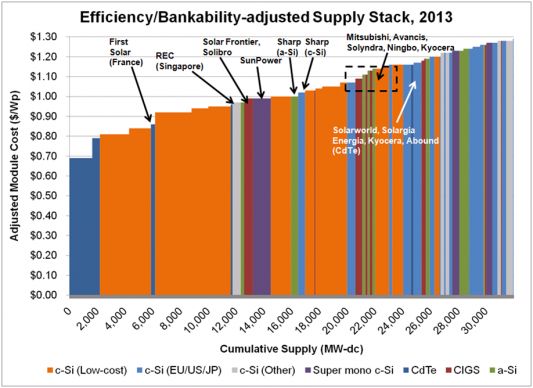

The 2013 supply stack, shown below, illustrates the evolution in competitive positioning of firms. More bankable low-cost Chinese c-Si supply moves to the front of the stack, given the disproportionately higher capacity ramps of players in this class. This, along with First Solar, makes up about 8 GW, or 38%, of the expected 2013 demand of 21 GW. The composition of the stack from 8 GW to 24 GW (the firms that will compete for most of the remaining demand) has notably more CIGS and c-Si supply from ROW locations (such as REC’s Singapore facility, shown in grey), as well as tandem-junction supply (Astronergy, Sharp, Mitsubishi Heavy, Auria Solar). Only a few developed-world c-Si producers (Sharp, Solarworld, Mitsubishi, Kyocera) are positioned competitively. Interestingly, SunPower’s position remains largely unchanged over time, due in no small part to continuing advancements in module efficiency.

The improving competitive positioning of alternatives to developed-world (EU/US/JP) c-Si is substantiated by their share of non Chinese c-Si/First Solar production, which is shown in the figure below. From making up 53% of total non-Chinese c-Si/First Solar production in 2009, developed-world c-Si share is expected to fall to only 32% in 2013. It is displaced primarily by CIGS (3% to 18%) and tandem-junction Si (5% to 11%), while c-Si production in the rest of the world remains flat at about 1 GW throughout. It will thus be a combination of the best European and Japanese c-Si firms, CIGS players, and tandem-Si players that will compete for the limited demand that low-cost, bankable Chinese firms and First Solar cannot satisfy over the next few years. The characteristics of the successful firms point to strategies and business models that will drive competitiveness in PV manufacturing over the next half-decade. For the firms projected to be less than successful, the question is what they can do to prove these forecasts wrong. More on that next week.

This is an excerpt from GTM Research's recently published global PV supply chain report, PV Technology, Production and Cost Outlook: 2010 - 2015. The report addresses technical characteristics, production/capacity volumes, facility-specific manufacturing costs, supply-demand dynamics, and competitive positioning across all relevant PV technologies and nearly 200 wafer, cell, and module firms. For more on the report, go here.

41

41

15

15

9

9