Electric vehicle infrastructure companies have come a long way in the last decade, but they're still just a small slice of the grid edge investment pie.

That’s the upshot of a new study from Wood Mackenzie Power & Renewables that tracks all known investments in companies building out the charging infrastructure and controls to enable a society-wide shift to electric transportation.

EV deployment itself has a robust growth story to tell. The global population of battery-powered passenger cars on the roads, including plug-in hybrids, passed 5 million last year. It has grown at more than 50 percent annually since 2013.

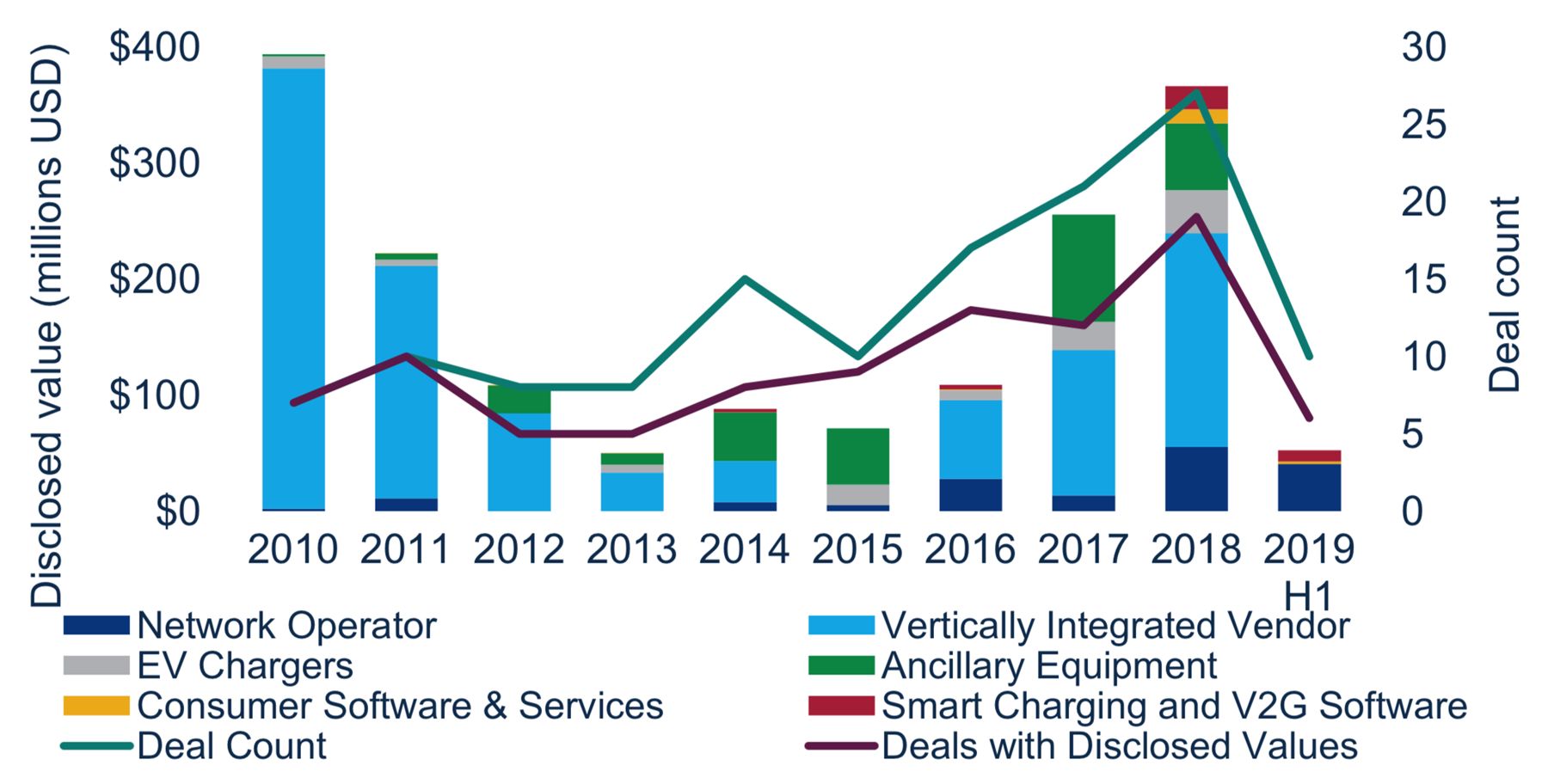

But investments in charging companies have not followed as consistent a trajectory, according to WoodMac’s analysis of disclosed deals. Big years in 2010 and 2011 petered out into several years of doldrums, with deals picking up again in 2017 and 2018.

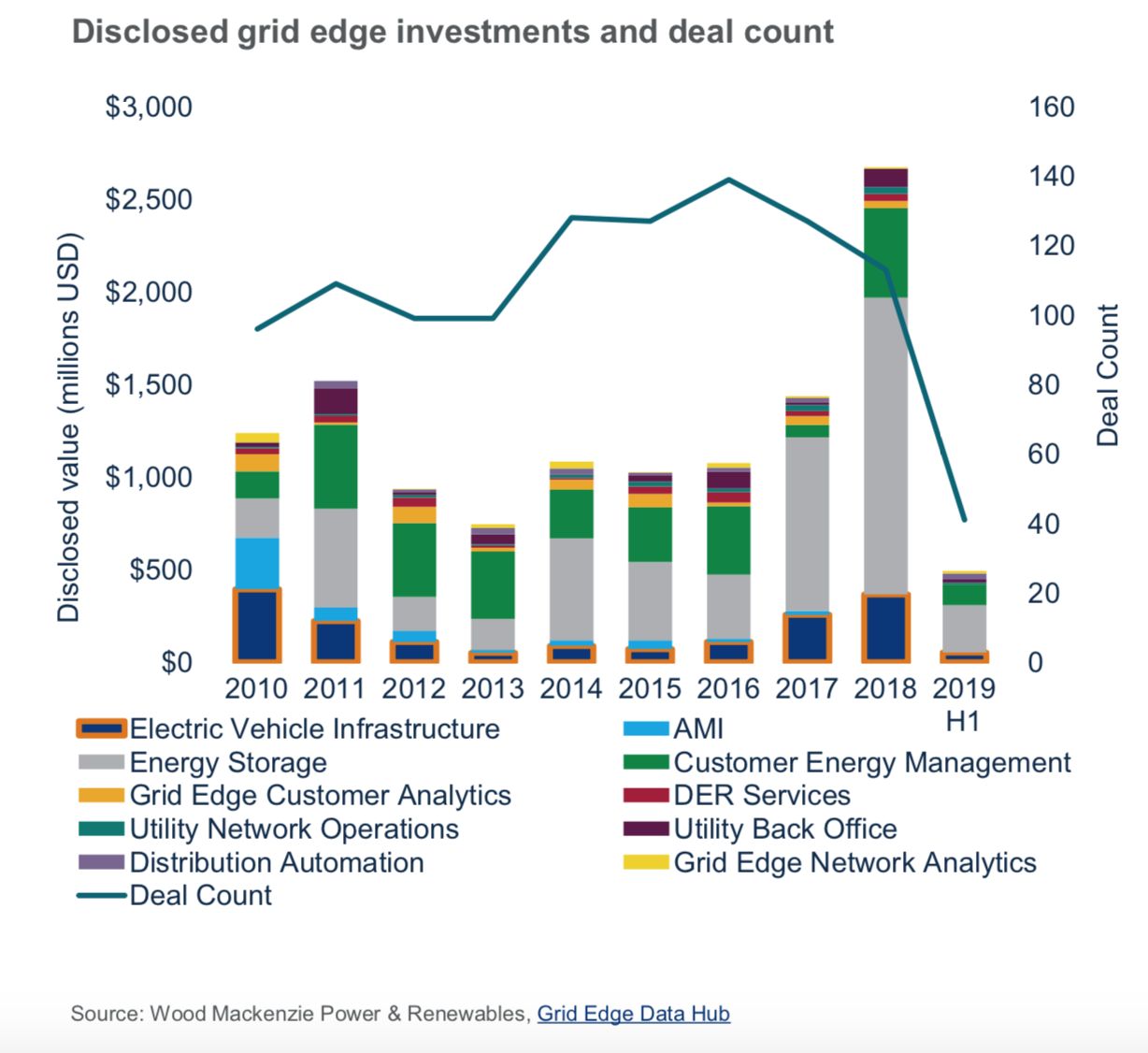

In sum, venture investments in EV infrastructure companies totaled $1.7 billion from 2010 through the first half of 2019, accounting for just 14 percent of all disclosed grid edge investments.

M&A activity was also erratic, with relatively big years in 2013, 2017 and 2018 and very quiet years otherwise.

“EV infrastructure accounted for only 8 percent of [grid edge] M&A deals, but the market is expected to play an increasingly important role in the emerging flexibility practices offered by energy majors,” authors Kelly McCoy and Paulina Tarrant write.

The hope for entrepreneurs in this space is that an increasing market value for grid flexibility will create renewed interest in smart charging technologies. The rise of intermittent wind and solar power drives a need for flexible power consumption, just as consumers are increasingly choosing electric cars. Charging infrastructure forms the link between the EV world and the grid.

Investments into EV infrastructure companies have been dwarfed by energy storage.

By the numbers

Some 61 charging infrastructure startups raised 133 investment rounds over the last decade, according to WoodMac’s database.

The key caveat here is that 29 percent of those rounds did not disclose the amount raised, so the total is definitely higher than the confirmed tally of $1.7 billion.

The M&A history is even more shrouded in mystery. Of the 32 acquisitions in the last decade, only 25 percent disclosed the price paid. Those deals add up to $489 million.

About two-thirds of the acquisitions were charger manufacturers, charging network operators, or vertically integrated vendors, which make chargers and operate them. All of these types of companies work on the physical expansion of charging infrastructure.

The vertically integrated companies dominated the fundraising game: The five companies in that category raked in $1.1 billion of the $1.7 billion.

Really just two companies drove that success. Israeli startup Better Place raised $616 million during the decade for its vertically integrated battery-swapping station concept. The company built stations across Israel and entered several international markets before collapsing in 2013.

ChargePoint brought in the next highest amount, $475 million; it operates the largest network of public chargers, with more than 99,000 units in the fleet.

Outlier charging company investments in 2010 made the rest of the decade look pretty uneventful.

Changing investor makeup and interest

"Non-strategic" investors, like venture capital firms and private equity, led more charging infrastructure investment rounds than any type of investor. That category is followed by “undisclosed investor,” but the second most active known category is strategic vendors, namely car companies. They are followed by strategic utilities and strategic oil and gas investors.

Utility involvement has a lot to do with the regulatory landscape those companies operate in, said McCoy, a research associate on the EV infrastructure beat.

In the U.S., regulated utilities typically cannot own chargers outright. Some U.S. utilities have invested in charging companies through venture arms. European utilities can compete in the charging arena, and thus have outpaced their American counterparts in acquiring companies.

Oil and gas companies joined the party in 2017, when Shell acquired European charging network NewMotion. Since then, oil majors have led six investments in the sector, with BP leading four of them.

Hardware to software

Over the years, the focus of investor dollars has shifted from the capital-intensive network deployment that brought in boatloads of cash at the start of the decade, to a more diverse ecosystem of smaller but more numerous investments.

"At the beginning, it was about getting more chargers out there so people could have access to the chargers," McCoy said. "Now you see other services that companies can provide through software. It’s cheaper to deploy, it’s easier, and there's a lot of revenue that can be unlocked through these companies."

Greenlots exemplifies that shift. The software-focused network operator raised less than $15 million, but proved itself valuable enough that Shell acquired it this year. Now the startup will spearhead Shell's electric mobility offerings in North America, with an emphasis on winning contracts with commercial fleets.

“Smart charging and vehicle-to-grid software markets are probably going to be more attractive to investors in the future,” said McCoy. “Utilities and vendors alike can use that technology to help their bottom lines.”

Utilities can use managed charging to react to demand response events, or soak up excess renewable generation that they would otherwise have to curtail. Vehicle or fleet owners stand to earn revenue for participating in grid flexibility services, as well as avoiding excessive demand charges.

Outside of China, fleet electrification is at a very early stage, and medium- and heavy-duty electrification has barely begun. But as more buses and trucks consume electricity instead of gas, the impact on the grid will expand significantly, creating additional venture opportunities, McCoy noted.

***

Learn more about Wood Mackenzie's new EV infrastructure report here.

41

41

15

15

9

9