Veteran venture capitalists like Josh Green, General Partner at Mohr Davidow Ventures, have had their usually optimistic views tempered by painful lessons of the cleantech past. Green presented on "The View From Sand Hill Road" at Greentech Media's NextWave Greentech Investing event in Menlo Park last week.

How can a "multifaceted" venture capital firm find its way back to the cleantech sector?

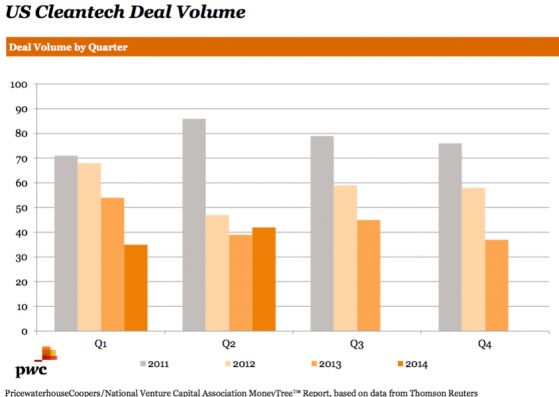

Green likened the following data "as the opening scene of Saving Private Ryan." He assured the crowd that "it gets better" and that cleantech is a great investment opportunity when it's done right.

Cleantech investment is barely perceptible on VC radar

| 2014 Q2 national VC investments | 2014 Q2 national VC cleantech investments |

| 1,114 deals | 42 deals |

| $13 billion invested | $600 million invested |

Cleantech accounted for 3.7 percent of all VC deals and 4.6 percent of all VC money.

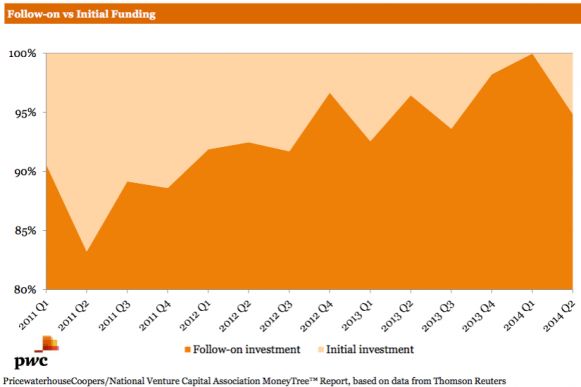

Green introduced the follow-on funding vs. new funding slide "as the most important slide."

Initial investment actually hit zero in Q1 of 2014 and a paltry 5 percent in Q2 when only $30 million went into "a small handful of deals." In other words, no investors are investing in early-stage cleantech.

Cleantech was first purpose-driven investment category

Green contended that this was the first time in venture that a "category had a purpose." He suggested that no previous category in VC focused on purpose rather than technology, saying it was "a simple, innocent mistake with large implications." It created tremendous category risk, political risk, unrelated technology risk and capital intensity risk

No other category had grouped unrelated technologies that made them dependent on each other. Biofuels and solar don't have a lot in common, but if one of the sectors starts to fail, "it stigmatizes the other sectors," according to Green.

Green suggested that capital intensity "was a bit of a ruse." He pointed out capital-intensive cleantech successes like Tesla, as well as IT startups like Twitter that require $400 million.

The pendulum will swing again

Green acknowledged that most mainstream VC firms have dismantled their cleantech groups. And despite "the lean startup" having become part of the Sand Hill Road lexicon, "the pendulum will swing again," according to Green, "but not for the next few years." He added, "When the pendulum swings, it will be at shocking velocity," and the "large majority of winners come from being early in a pendulum swing."

He suggested that "cleantech as a VC investment category is being reinvented with different labeling."

Broadcast live streaming video on Ustream

41

41

15

15

9

9