U.S. utilities can’t reach their ambitious decarbonization goals unless they reduce their planned reliance on natural gas, find ways to “baseload” solar and wind power with long-duration storage or substitute zero-carbon fuels, and radically expand energy efficiency, demand response and the power and flexibility of customer-owned distributed energy resources.

So says a new report from Deloitte highlighting the known, yet often underappreciated, challenges faced by utilities across the country promising to zero out their carbon impact by midcentury. “The math doesn’t yet add up,” the report finds, citing “significant gaps” between the decarbonization targets of major utilities and their current plans for retiring fossil-fuel plants.

That’s not news to those who’ve been closely tracking plans to reach net-zero carbon from major U.S. utilities such as Duke Energy, Dominion Energy, Southern Company and Xcel Energy. Each still plans to build new natural-gas power plants in the near term, despite the additional emissions they will cause. And each relies on as-yet-uneconomical technologies, such as long-duration energy storage, net-carbon-neutral fuels to replace fossil natural gas, and carbon capture and storage, to reach the final goal.

The U.S. electric grid relies on fossil fuels for 63 percent of its generation, and according to the U.S. Energy Information Administration, current trends will reduce but not eliminate those emissions by 2050, the report states.

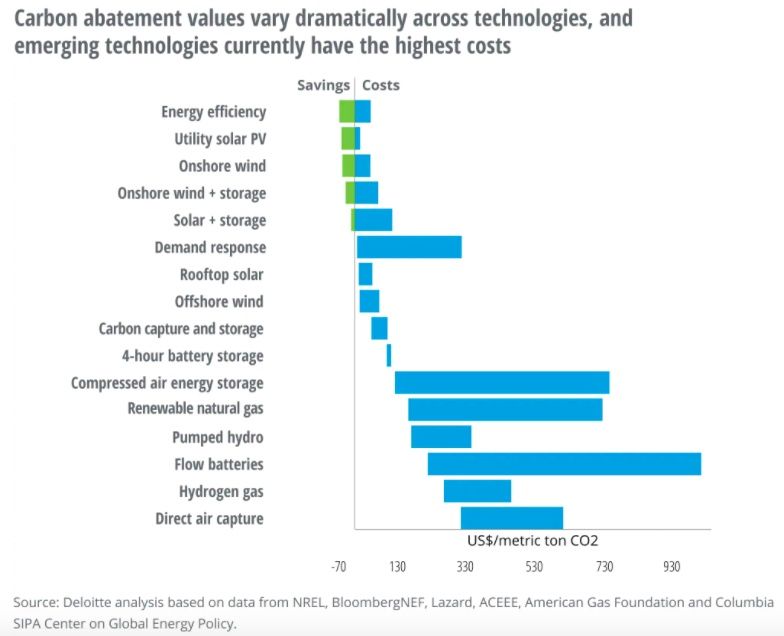

To fix this, Deloitte suggests a three-stage approach, centered on technologies and approaches that will be cost-effective for the decade they’re targeted for — a vital consideration if decarbonization isn’t to lead to skyrocketing electricity costs and popular backlash. This chart indicates the carbon-abatement values of different technologies compared to replacing coal plants, indicating how utilities might want to stage their deployment over the next 30 years.

Stage 1: "Renew" fossil fuels with renewables and storage

The first stage, dubbed “renew,” concentrates on replacing coal and natural gas with renewables and energy storage. All utilities with zero-carbon goals have pledged to do this — but not at the pace and scale required, Deloitte says.

For example, 87 percent of the coal-fired generation controlled by “zero-percenters” lacks a specified retirement date. That’s largely because of the costs of early retirement of still-productive power plants. To solve for this cost problem, utilities and state regulators could issue ratepayer-backed bonds to cover un-depreciated coal plant balances, which can also help secure funds to help communities recover from the loss of jobs associated with early closures.

Natural-gas plants are a trickier prospect since many still have years of profitable operation ahead of them. They’re also a key dispatchable asset to help meet peak grid demand. Yet falling costs for renewables and batteries threaten to leave some of the $70 billion in natural-gas capacity planned over the next decade as “stranded assets” unable to earn back their costs, leading more state regulators to demand their replacement with renewables and storage in long-term resource plans.

Renewables and storage growth would have to break all existing records to replace new natural gas with clean energy while maintaining grid reliability, however. A recent study charting a cost-effective pathway to 90 percent clean energy by 2035 found that it would require 1,100 gigawatts of new wind and solar, or about 70 gigawatts per year, more than triple the additions completed in any one year to date.

Likewise, the need for enough storage to replace existing natural-gas peaker capacity exceeds that called for in “zero-percenter” utilities’ plans. While lithium-ion batteries paired with new solar and wind is a cost-effective solution in many markets today, closing the remaining storage capacity gap will require “additional revenue streams,” from wholesale market participation to tighter integration of behind-the-meter batteries.

Stage 2: "Reshape" the demand side of the grid

Deloitte’s second stage, dubbed “reshape,” concentrates on the demand side of the equation, namely shifting electricity loads to match a primarily renewable-powered grid. That’s going to require a massive growth in energy efficiency and demand response, as well as retooling approaches to tap the flexibility of digitally controlled loads and the value of behind-the-meter solar, batteries and plug-in electric vehicles.

Combining these largely separate utility programs into “clean energy portfolios” will help align customer incentives with grid needs, the report notes. So will smart inverter standards that allow utilities to communicate with and manage behind-the-meter solar and storage, and new regulatory mechanisms that could allow utilities to invest in or earn returns on investment into demand-side capacity.

Recent regulatory actions such as the Federal Energy Regulatory Commission's Order 2222 are opening up opportunities for distributed energy resources to participate more fully as grid resources, Kate Hardin, executive director of Deloitte's Research Center for Energy, Resources and Industrials, said in a Monday interview. But Deloitte has pushed these demand-side efforts into the 2030-2040 timeframe due to the complexity of enabling them at scale, "even if you assume you’re able to get the regulatory support you need to allow [distributed energy resources] to play the role [they] can."

Stage 3: "Refuel" the electricity-fossil fuel

Deloitte’s final stage, dubbed “refuel,” takes on the looming challenge of replacing fossil fuels not just for generating electricity but also to power transportation, building heating and other key human needs. In terms of greening the power grid, the report focuses on the potential to convert excess renewable energy to carbon-neutral fuels such as methane or hydrogen for use in remaining natural-gas-fired power plants, and as “seasonal storage” to cover the gaps between supply and demand from summer to winter.

These technologies are furthest away from commercial viability at present, but they’ll “have some runway to mature by 2040-2050 when they are expected to be most needed to close the last 20 percent gap,” the Deloitte report states. Without them, utilities may face the need to overbuild wind and solar to cover gaps between supply and demand, or to build transmission at a scale the country hasn’t yet seen to transport available clean energy to where it’s lacking.

These kinds of tradeoffs are already part of zero-percenters’ long-range visions, as with Duke Energy’s latest integrated resource plan, which identifies a mix of “zero-emitting load-following resources” to replace its gas-fired capacity. Options include net-zero carbon fuels, cost-effective carbon capture, utilization and storage, small modular nuclear reactors, or long-duration storage technologies such as molten salt, compressed/liquefied air, sub-surface pumped hydro and advanced battery chemistries.

“Financial constraints and [research and development] investments are major hurdles, but a U.S. clean energy stimulus package and carbon tax could also quickly change the pace of development and deployment of technologies and their costs,” Deloitte’s report notes.

If Joe Biden is elected president in November and the U.S. Congress enacts his clean energy plan, the country will have both a much faster timeline to decarbonization by 2035 and $2 trillion in spending to boost those efforts.

41

41

15

15

9

9