Two weeks ago, utility Southern California Edison launched a real-world experiment in grid-edge economics, one that’s going to unfold in real time and at gigawatt scale.

In a first for the utility industry, SCE announced it would buy hundreds of megawatts of distributed solar, behind-the-meter batteries, automated demand response and targeted energy efficiency as part of its 2,200-megawatt Local Capacity Requirement (LCR) procurement for its grid-stressed West Los Angeles Basin region.

SCE had to come up with new ways to measure the cost-effectiveness of a wide variety of very different technologies and business models against one another in order to pick winners and losers from the dozens of proposals it received. It also had to measure the value of the location of these assets, since it’s trying to solve local transmission and distribution grid congestion problems with the same resources.

If this contracted mix of central power plants and distributed grid-edge assets can meet SCE’s long-term needs, it could serve as a model for other utilities around the world looking for ways to solve similar challenges. That makes the details of these contracts of great interest not only to the winning bidders, but also to the industry at large.

SCE didn’t reveal the financial details of its long-term power-purchase agreement contracts with winning companies including AES Energy Storage, Advanced Microgrid Solutions, Ice Energy, Stem, SunPower and NRG Energy. But it has talked to Greentech Media about how it went about crafting this unique, all-of-the-above procurement.

“This LCR procurement that we just announced is an effort that’s been underway for about two years,” Colin Cushnie, SCE’s vice president of energy procurement and management, said in an interview this week. The California Public Utilities Commission had ordered SCE to fill about one-third of its megawatts with “preferred resources” -- anything but fossil fuel, essentially -- to help replace the shuttered San Onofre nuclear power plant, as well as several once-through water-cooled natural gas-fired power plants set to close in the coming years. This map shows the regions being targeted, with green areas being the highest priority.

To measure these preferred resources against traditional central power plants, SCE first ran a quantitative analysis to model all the costs associated with each technology category, he said. That included the capital costs of the solar, batteries, or demand-side management technologies involved, as well as the costs associated with making them available for fast, reliable dispatch by utility grid operators, he added.

SCE primarily relied on existing energy markets to model the revenue streams that should be available to these different assets, he said. That’s tricky, because some of the values of these distributed, customer-owned assets don’t yet have regulatory or market mechanisms to allow them to capture those revenues, he noted.

“It’s a recognition that we have imperfect information at this time,” Cushnie said. “For the local capacity procurement, we were looking for some specific attributes.” For example, SCE put a lot of weight on projects that could locate resources close to certain overloaded or congested sections of the grid.

Location, location, location

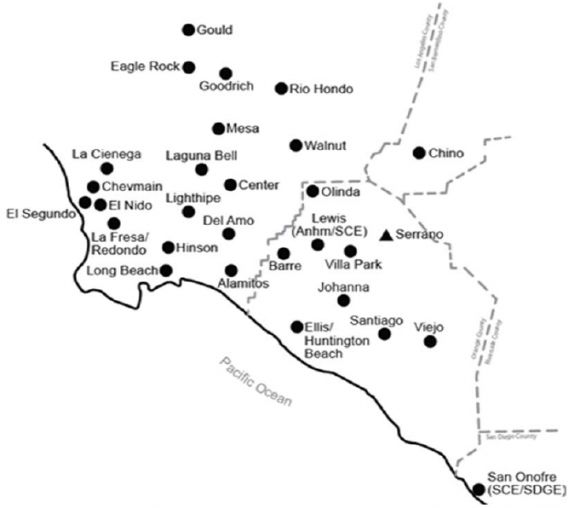

Cushnie said that SCE “looked closely at two substations in Orange County,” the Johanna and Santiago substations, which have been targeted as critical. The utility has launched a separate Preferred Resources Pilot (PDF), formerly known as its “living pilot,” to test the proposition that properly sited and connected distributed energy assets can meet both local and system-wide needs.

Here's a map of the substations SCE has ranked in terms of "locational effectiveness factors," based on their usefulness in mitigating grid constraints west of the Serrano substation, which is shown as the triangle on the map. (Also note the shuttered San Onofre nuclear power plant in the southeast corner of the map.)

“The procurement we ultimately landed on increased slightly as a result of our focus on the preferred resources pilot,” he noted. For projects in that area, including many of the largest distributed behind-the-meter battery, solar power and thermal energy storage deployments, “we were willing to pay a little bit more to get preferred resources in the pilot location.”

Still, “it wasn’t that much more in terms of incremental megawatts,” Cushnie said. In fact, all winning projects had to first surmount an “initial pass” cost-competitiveness stage that winnowed out a number of competing projects, he said.

Even more importantly, these projects are reducing load at thousands of customer sites, not adding new generation to the grid that supplies them, he said. For regions that are already facing overload conditions on certain circuits, this method of subtracting load can help solve problems that new generation would only exacerbate.

Then, of course, there are the siting and air-quality constraints that make new gas-fired power plants difficult, if not impossible, to site in the region, he said. Indeed, while SCE’s procurement is adding nearly 1,400 megawatts of natural gas generation, the vast majority of that is expanding existing power plants, with only one new 98-megawatt peaker plant slated to be built.

Energy storage, efficiency and DR: Turning grid customers into utility assets

Energy storage made up the second biggest category, with about 250 megawatts of large-scale and distributed battery and thermal storage project. That’s five times the 50 megawatts the CPUC had ordered the utility to procure -- but it’s just a fraction of the energy storage bids that SCE received, Cushnie said.

“A fair number of [energy storage] bids were cost-effective [compared] with our conventional resource bids,” but then again, some were wildly uncompetitive, he noted. ”Any emerging technology, you’ve got people all over the map in how they’re seeking to use the asset [and] the cost structure around it,” he said.

SCE also struggled with some as-yet-unanswered questions about how grid-connected energy storage projects will pay for, and get paid for, the grid-supplied energy they use to charge and discharge, he noted. That’s why the utility chose only one big grid-interconnected project -- AES Energy Storage’s 100-megawatt lithium-ion battery complex, which will be built alongside its Alamitos Power Center in Long Beach, Calif.

“The balance of the energy storage resources are what we call 'behind the meter,' located on the customer side of the grid,” he said. Those include projects from Stem and Advanced Microgrid Solutions that will put batteries at the service of the utility for fast-acting load reduction, as well as Ice Energy’s ice-making rooftop air conditioning units to permanently shift load from peak to off-peak times, he said.

This distinction between fast-acting and long-term demand management helps define the difference between the demand response and energy efficiency portions of its LCR procurement, Jesse Bryson, power origination manager at SCE, said. The utility awarded about 136 megawatts of energy efficiency contracts to companies including NRG, Onsite Energy Corp. and Sterling Analytics, along with 75 megawatts of demand response from NRG.

“In all of these contracts, there’s more skin in the game than you might see in a typical procurement,” Bryson noted. That includes surety payments, performance assessments, and some form of collateral to back up their promise of delivering staged increases in their resource over the next five years. For the energy efficiency projects, SCE is also making payments over four to six years after they’re implemented, rather than the typical method of paying when they’re installed, he said.

As for the demand response portion, all of the assets have to be able to respond within twenty minutes of being dispatched, he said. That’s a lot faster than the traditional day-ahead or hour-ahead programs that make up the bulk of utility demand response programs today, although SCE and other California utilities have also been rolling out automated demand response using OpenADR to bring demand-side resources into play for more lucrative energy and grid ancillary services markets. However, rules for how distributed energy players can participate in demand response are still being worked out by the state's regulators, utilities and grid operators.

A new model for utility-backed, distributed solar?

One of the most interesting contracts SCE awarded is for distributed solar power as a grid resource. SCE is asking solar giant SunPower to deploy about 50 megawatts of customer-sited solar that will look a lot like the rest of the rooftop solar PV in the region. But it will be compensated in a way that’s very different from the net metered or PPA-based solar systems out there to date.

SunPower plans to install solar in increments of roughly 500 kilowatts per site, and aggregate them into groups that will range from 4 megawatts to 12 megawatts, Bryson said. SunPower has preselected several sites that combine the key attributes of building owners willing to install solar and locations that SCE needs to bolster with some predictable amount of solar generation.

From the utility’s perspective, “it almost looks like an energy efficiency aggregator, where SunPower will commit to achieve savings through solar power, and go out and procure that, and it has to be in a targeted location,” Bryson said. “I’m not aware of a similar form of contract” between a utility and a solar power provider, he said.

Some key differences include the fact that SunPower’s distributed solar asset will not be exporting any power to the grid, Cushnie noted. “The energy price algorithms we used for our evaluation were developed with an assumption of what your ideal resource mix would be to serve the load,” he said. By adding solar in targeted spots, SCE is essentially reducing the need to serve those loads with additional generation, he said -- “It’s avoiding the cost of what would otherwise have happened.”

Expect these kinds of calculations to play an increasingly important role in states like California, New York, Hawaii and others where the merits and detriments of distributed, customer-owned solar and other grid-edge assets are being hotly debated. As GTM Research analyst Cory Honeyman commented, “While there have been broad procurement plans in the past, never before has a utility procured such a diverse cross-section of behind-the-meter and grid-scale solutions in one solicitation."

41

41

15

15

9

9