The U.S. residential solar industry has continued to regain momentum after a challenging spring season due to the coronavirus crisis. On top of demand recovery, strong asset performance throughout the pandemic has proven that residential solar is primed for further investment from a variety of capital sources.

Attractive financing options — in particular, solar loans — have greatly contributed to the market recovery. Homeowners are looking to save money during this time of economic hardship. Purchasing a solar system through debt offers immediate bill savings and does not require customers to expend precious cash.

On Tuesday, Sunlight Financial announced that it has funded over $3 billion in loans for solar systems and home improvement projects, while Mosaic passed that mark back in January of this year. Loanpal, currently the industry’s largest financier, has funded over $4.5 billion in solar loans as of October, according to a report from Kroll Bond Rating Agency (KBRA).

These top three solar loan providers are among the fastest-growing private companies in the U.S. over the last few years. Aside from broad market contraction in Q2 due to the coronavirus, this growth trend has continued in 2020. Installers and loan companies have reported month-over-month increases in sales and loan approvals since state governments began easing lockdown restrictions. Many players have also achieved record sales volumes in recent months.

Solar loan portfolios have passed the COVID-19 stress test

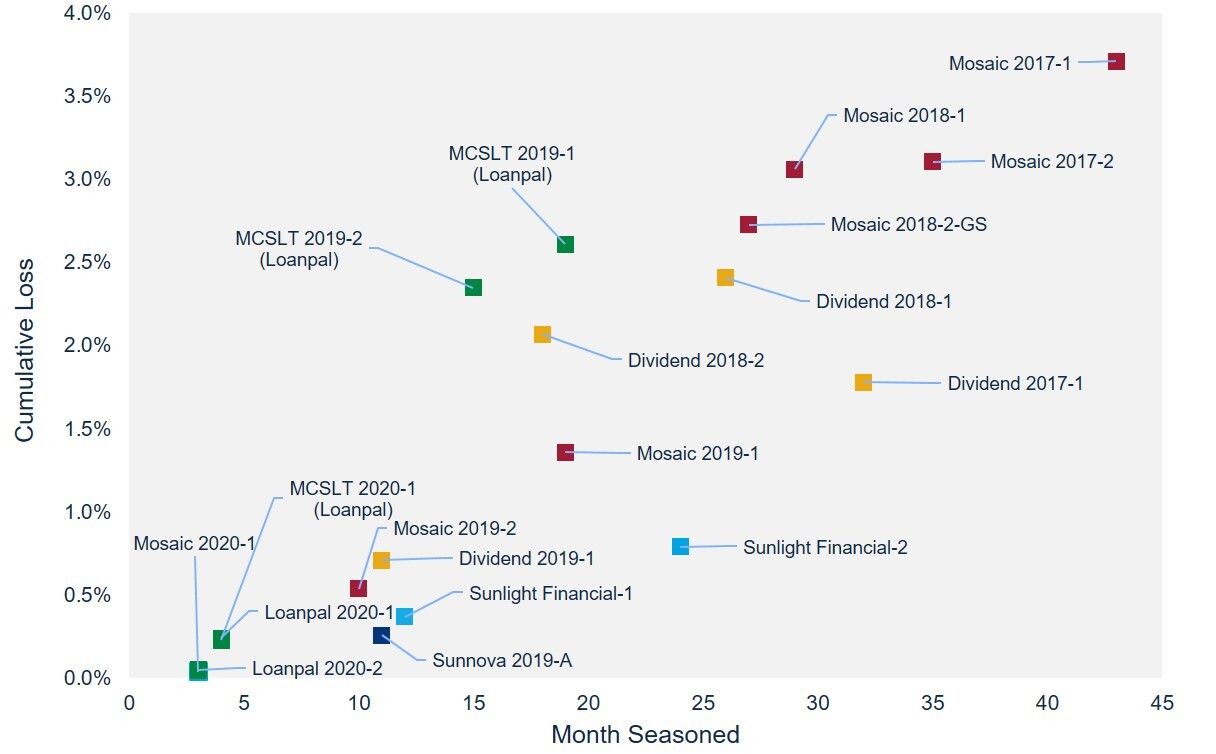

The proliferation of these financiers and the solar loan market more broadly is a well-documented trend in the industry. But the overall strong performance of the asset class is arguably an even more important metric of success.

Residential solar’s remarkable resiliency throughout the pandemic has provided evidence that these assets can hold up during a time of economic downturn and uncertainty. Positive news came in May when KBRA announced a comprehensive review of all outstanding ratings for solar loan asset-backed securitizations in response to the macroeconomic impacts of the COVID-19 pandemic. For all 17 securitizations that the agency had rated, KBRA did not issue any downgrades or watch placements.

Sources: Kroll Bond Rating Agency, Sunlight Financial, Wood Mackenzie. Loss rates for Mosaic, Sunnova, and Dividend are based on cumulative net loss. Rates for Loanpal and Sunlight Financial are based on cumulative gross loss.

Solar loan providers continue to report that their books of business have maintained healthy forbearance request levels and low delinquency rates. Several providers introduced payment-relief programs to assist customers through COVID-19. As documented by KBRA, these have gone mostly untouched. The loans to which Loanpal granted COVID-19 disaster forbearance topped off at just over 1 percent of its overall book back in June, and that rate declined to 0.38 percent as of October. Only 0.3% of Sunnova’s customers needed short-term payment assistance as of May. Mosaic had given extensions to 2% of its customer base, also as of May, and this figure declined to 0.29 percent in August.

The “hierarchy of bills” concept can help explain low delinquency rates for residential solar assets. Most solar customers enjoy somewhere between a bill swap and substantial monthly savings when compared to their utility bill prior to going solar. The alternative to paying a solar loan would likely be more expensive for the customer; therefore, there is a powerful incentive to remain current on the loan. This is especially true during a time of economic downturn when saving money is crucial.

It is time to pick industry winners

Securitization markets are just one glimpse into the investment landscape. For example, Sunlight Financial sources capital from forward-flow agreements and private portfolio transactions. Here, too, we see strong asset performance and some of the lowest loss rates out of all transactions.

Performance, of course, varies by transaction and by provider. Mosaic has the most-seasoned loan portfolios and thus the longest data trail. The company’s latest securitization, which was oversubscribed multiple times over, demonstrated the high demand for these assets as more historical loan performance data trickles in month by month. Investors looking to enter or expand their presence in this space will closely observe these loss rate developments for each provider. This will be an important step in investment due diligence going forward.

It is true that solar loan portfolios are still in their early days, and years of payments are yet to come. However, now that the industry has proven itself through a crisis, little doubt remains when it comes to assessing the merits of the asset class. Issuers are completing transactions more frequently, and a growing history of performance data provides more clarity and insight for investment decision-making.

Because of these factors, investors have grown more comfortable with the residential solar asset class over the last couple of years and have rewarded players with more capital at lower costs. Banks and credit unions have more cash on hand due to increased deposits as homeowners hold on to their savings. These organizations are looking for a place to soundly deploy their capital. Their question when it comes to residential solar is shifting from “Should we invest?” to “Which company should we put our money on?”

While the pandemic is not over, and the solar industry is still in the middle of battling a recession, one thing has become clear: As a maturing asset class, residential solar has passed its first true test, and there are many positive signs for the future. Institutional investors that have moved into this space are sure to be pleased with the results they have seen thus far.

***

Bryan White is a solar analyst at Wood Mackenzie and the author of the U.S. Residential Solar Finance Update report series. Look for the next report release in December at woodmac.com.

41

41

15

15

9

9