I have a confession to make.

In 2011 I became involved, in a small way, in a multi-billion-dollar scheme to buy out HECO, Hawaii's electric utility, and take it private. The plan was to shift HECO from its reliance on fossil fuels and allow the island to instead be powered by its natural gifts of geothermal, solar and wind resources.

The crazy part of this story is that the deal came pretty close to actually getting done.

I'll make a long story short.

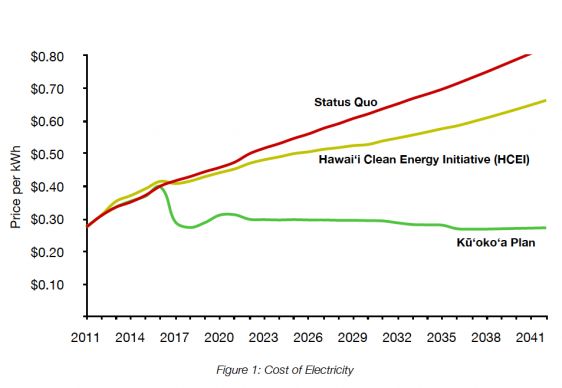

Hawaii has the nation's highest electricity prices, and the situation will only get worse in the years to come. Roughly 75 percent of the island's electrical power comes from imported oil. A solution HECO developed back in 2011, The Hawaii Clean Energy Initiative, allowed the utility to continue its tradition of burning stuff such as uneconomical biofuels.

Kuokoa, the group I worked with, proposed a solution that would transition the island away from its petroleum habit toward baseload geothermal along with solar and wind on a modernized grid. Our analysis showed that the cost of green electricity could be kept flat and was certainly lower than anything HECO could offer over the next 50 years.

Like many investor-owned utilities, HECO is boxed in. Making any significant grid overhaul requires enormous capital outlays -- which is at odds with quarterly expectations or raising already high retail rates. Additionally, HECO's fleet of legacy generation units will require billions in clean air standards upgrades. At the same time, deep PV penetration is reversing load growth and destabilizing the grid.

The new plan:

- Take HEI, HECO's parent company, private and sell off the HEI-owned American Savings Bank

- Use the utility dividend stream to help support financing costs

- Invest private funds in an accelerated and transformed capital program

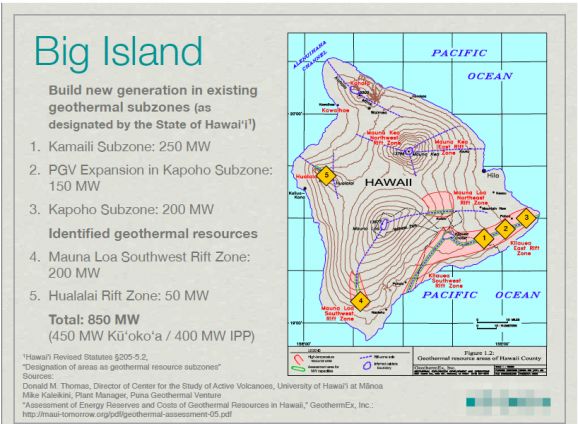

- Build geothermal plants, especially on Hawaii

- Install an undersea inter-island cable system to deliver power to Oahu

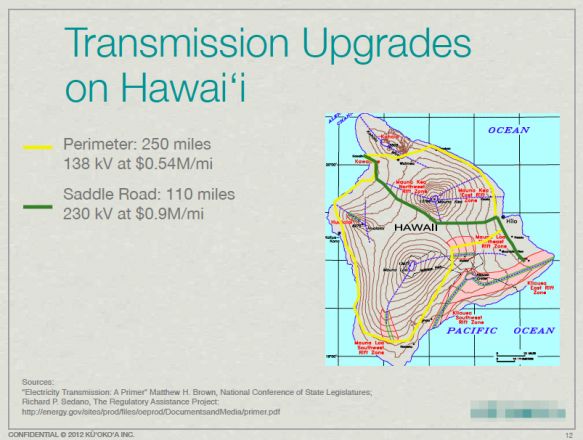

- Upgrade the T&D system to handle renewables

- IPO the radically different utility for long-term growth and financing

The entire island chain of Hawaii has just 2,400 megawatts of generating capacity with 95 percent of the population served by a single utility. It's feasible that a willing utility and a team of entrepreneurs could effect some real change on a grid of this scale.

You would think that a utility blessed with significant solar, wind, ocean, and geothermal energy resources would already be leading that transformation today. But a certain amount of institutional inertia, aggravated by decades of dependence on oil, is delaying an epochal opportunity.

A certain amount of cultural inertia is at play as well. In past decades, local Hawaiians might have taken a dim view of using the island's geothermal resources. That stance has softened, however. The plan would have taken advantage of the Big Island's geothermal resources to provide baseload power to Oahu.

The plan factored in the grid upgrades necessary to support the shift to renewables.

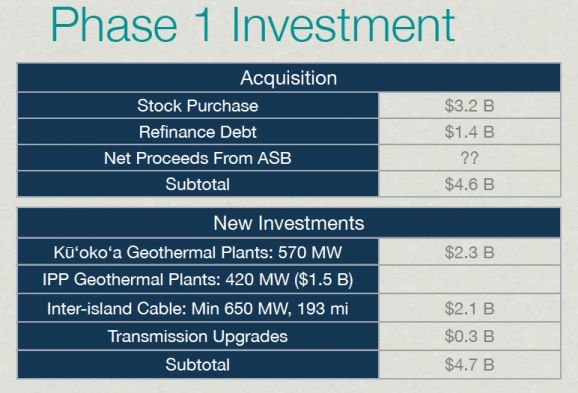

It was an audacious $6 billion showcase deal that meant going after a regulated utility in one of the more idiosyncratic U.S. states. Still, private equity firms and banks buy and sell utilities and power firms every week -- deal sizes in this range are not out of the ordinary.

That was the plan.

The Kuokoa team had utility, community, regulatory and finance experience and put together extensive and convincing financial models that made sense and had a much better outcome than HECO's 75-cent-per-kilowatt-hour power.

An energy transformation could occur in Hawaii if HECO was institutionally able to look beyond short-term profit and embrace distributed generation rather than inhibiting it.

Don't just take my word for it.

In fact, Hawaii's PUC, backed by the state's governor, just issued a harsh rebuke to HECO regarding its flawed integrated resource plan. As GTM's Bentham Paulos reported, the Public Utilities Commission issued regulatory orders calling for HECO to implement a distribution circuit monitoring program and establish a more transparent interconnection queue. HECO must also submit a plan to “expeditiously retire older, less-efficient fossil generation, reduce must-run generation, increase generation flexibility, and adopt new technologies such as demand response and energy storage for ancillary services and institute operational practice changes.”

Paulos adds, "Even if Hawaiian power providers aren't ready to embrace distributed generation, regulators clearly are."

The acquisition offer

Anyway, we had a real plan that penciled out -- and all we needed to do was to track down $6 billion in debt and equity.

Over the next few months, we spoke with large lending institutions, investment banks, private equity firms, wealthy people, venture capital firms, family offices, angel groups and grid and finance experts. I don't believe a single person that saw the plan didn't acknowledge the obvious logic of the proposal.

(Recall that this article is the short version of events.)

We eventually connected with a banking behemoth that found the proposed deal credible enough to study further. And curiously enough, after a lot more analysis, the bank gave the nod to provide the debt for a slightly scaled down version of the project.

I'll repeat that: the big bank with a name you'd recognize said it was in for several billion dollars.

It gets weirder.

The transaction would require an equity piece as well. A few stellar introductions and some skillful analysis later, and we had a global private equity firm known for leveraged buyouts that was also in for several billion dollars. The PE firm's analysis was detailed, deliberate and thorough. I read through the financial analysis again last night, and it's hard to find a stone left unturned.

To recap, we had just sourced the debt and equity needed to make an offer to acquire HECO at a strong premium over its share price at the time.

All that remained was to make an offer (something these equity folks do every day), negotiate with Hawaii's regulators and politicians, and liberate the Hawaiian islands from their burden of oil. Cue rainbows and unicorns.

So what are the mechanics of an acquisition? How did Apple formally approach Jimmy and Dr. Dre with an offer for Beats? How does Facebook reach out to WhatsApp?

In the case of HECO and the offer, our top-tier private equity entity had longstanding back-channel relationships with members of the board of HECO. Our rockstar private equity representative made the dramatic, multi-billion-dollar, transformative offer to HECO's decision-makers.

And was promptly turned down.

End of story.

What's the next step? For a private equity firm not willing to go the hostile-takeover route, the "no" answer from HECO meant "no" and signaled that it was time for them to look for their next deal.

As for the utility irritants at Kuokoa, the Honolulu Star-Advertiser reported, "Kuokoa dropped its bid to take over HEI in early 2013."

So, the story of Kuokoa is over. The effort went further than almost any of us expected, and we emerged with a mammoth story of "the one that got away."

But Hawaii's utility story is still very much being written. Despite earning profits in its recent quarter, HECO faces an existential threat from the price of oil, the price of renewables, the intervention of the PUC and its own lack of proactive solutions. And the buyout story is not necessarily over either. A smarter takeover crew, armed with more experienced personnel and a stronger succession plan, could really make a run at this utility. Last week, HECO announced that Richard Rosenblum, its CEO since 2009, looks to retire within a year.

HECO still has the choice of acting as a model for utility transformation or serving as the poster child for utility paralysis in the face of change.

***

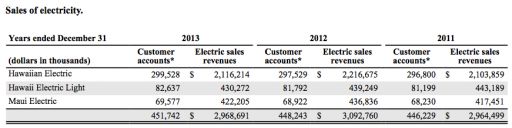

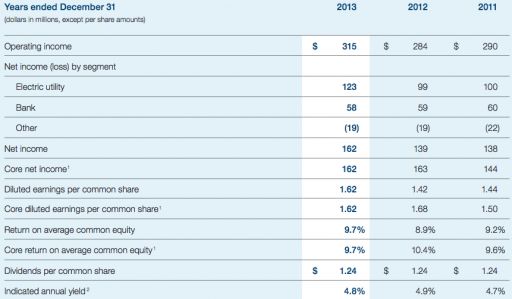

2013 HEI electricity sales and financials

Revenue for the utility portion of HEI, Hawaiian Electric Industries:

Other recent GTM articles covering renewable energy in Hawaii

***

Affiliations: I was an investor in this effort and a consultant to Kuokoa from July to October 2011.

41

41

15

15

9

9