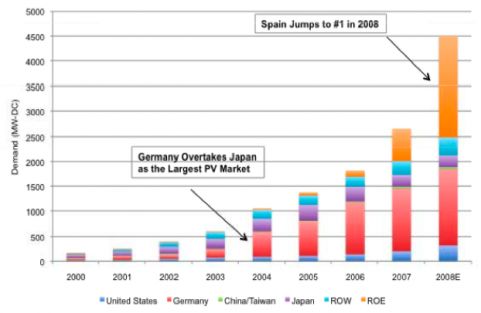

Japan was the largest solar market in 2003. Starting in 2004, because of a generous and well-administered feed-in tariff, Germany led the globe in solar demand and has remained the "savior market" for photovoltaic panel makers.

That would be with the exception of the Spanish solar debacle, whereby Spain went from global number one in 2008 to virtually no market in 2009 due to a poorly priced and administered feed-in tariff. Spain's tariff system had no mechanism to adjust rates as market conditions changed. Drastic measures to withdraw the feed-in tariffs plunged the market from more than two gigawatts in 2008 to about 100 megawatts in 2009.

The point is that planning and regulatory diligence can make or break a renewable energy policy. Germany seems to have done it right, while Spain and perhaps now Italy are examples of how to get it wrong.

The solar industry rested some of its hopes on the Italian market in 2010. Generous feed-in tariffs attracted investors and developers.

And that's worked out well, depending on which numbers you choose to believe. The 2010 Italian market is either 1.8 gigawatts according to analysts or 6 gigawatts if you have faith in the GSE, Italy's federal agency for energy services (Gestore dei Servizi Energetici).

Vishal Shah of Barclays Capital said in an investment note, "No one really knows how many megawatts were installed. Anyone claiming to know how many megawatts were installed with a high level of conviction is probably just guessing."

So -- there was an enormous surge of fourth-quarter solar applications in Italy and because the GSE does require good documentation, there is consensus that many of those applications were genuine.

The next shoe to drop is the action that the Italian government takes to fix the mess.

There were more than 50,000 applications, and if the government pays the 2010 incentives for the entire 4 gigawatts in applications pending grid connection, that would mean approximately $60 billion in incentive burden, according to Shah -- a figure "higher than the German/Spanish subsidy burden."

There remain a lot of questions about how the GSE will deal with this fiasco. They certainly are not equipped to inspect every one of the more than 50,000 applications in any efficient way. Again, according to Shah,"Most solar panel manufacturers and the Italian industry association believe that only 25 percent of the 4 gigawatts in reservations were complete."

The actual number is less important than whether Enel, the Italian electricity utility, can interconnect all of these projects and the effects this will have on the Italian solar market and on solar manufacturers in the second half of 2011. How widespread is the issue of project developers cheating? And how will the GSE deal with that -- criminal charges or just being put back into the 2011 queue?

Charges of "feed-in tariff fraud" are surfacing, with word of large megawatt-scale installations turning out to be just a few tens of kilowatts. "As we feared, cases of real fraud have emerged," Industry Minister Paolo Romani said in a letter to Corriere della Sera cited by Reuters. "It's an abnormal acceleration. Controls have started immediately."

Solar module suppliers such as Yingli, Trina, SunPower, Suntech and First Solar are some of the leading suppliers to Italy and their ASPs could be negatively affected in the second half of 2011 from this errore. This would also affect inverter suppliers overexposed in Italy like Power-One.

Shayle Kann, Greentech Media Research's Managing Director, sums it up: "There is a high probability that much of the 4 gigawatts announced by the GSE was not actually completed in 2010. But even 25 percent of that would result in a total 2.85-gigawatt Italian market in 2010 -- much higher than the Italian government expected or desired. Over the next few months, we will see Italy's response, potentially in the form of further FIT cuts or a hard cap on the market. Combined with mid-year cuts in Germany, this dims second half prospects for the global market. In the longer term, this supports our assertion that 2011 will mark the beginning of a global demand diffusion in which the industry becomes less reliant on a single market of last resort, but is instead supported by a class of markets expanding more steadily in tandem. Look for growth in long-term markets such as the U.S., China, and India as markers of this trend."

41

41

15

15

9

9