In 2014, the U.S. commercial market segment was surpassed by the residential segment for the first time in decades. According to the most recent U.S. Solar Market Insight report, the commercial segment saw 1,036 megawatts come on-line in 2014, down 6 percent year-over-year. However, GTM Research sees this as just another dip in the tracks of the commercial market roller coaster.

Source: GTM Research Solar Executive Briefing, Q1 2015

GTM Research forecasts the market to rebound in 2015, growing 40 percent over its 2014 total. In the latest Executive Briefing for subscribing solar clients, Senior Analyst Cory Honeyman outlines three growth opportunities for the commercial segment that he is watching closely.

Before we dive into the opportunities, here are some of the challenges facing commercial installations.

What’s holding commercial solar back?

While residential solar can leverage FICO scores to assess customer risk, the commercial market lacks an industry-wide metric to reference in evaluating the risk of customer default.

Second, commercial projects are not easily replicable. Onerous site-specific requirements for distinct rooftop and ground-mount projects spur lumpy, unpredictable installation timelines.

In addition, there are limited opportunities for portfolio project finance. The transaction cost of small-scale (< 1 megawatt), one-off projects are often comparable to those of much larger deals. Deal timeline with pools of small-scale projects are inevitably dragged out and face extraneous transaction costs.

These challenges are not insurmountable, as demonstrated by the more than 3.2 gigawatts of commercial PV that have been installed in the U.S. since the beginning of 2012.

Here are the opportunities that Honeyman identified.

Cracking the code on small-scale commercial

As Shayle Kann, senior vice president of GTM Research, pointed out last year, PV systems below 1 megawatt have dipped in national market share of commercial installations for the last five years.

In an interview about the new briefing, Honeyman said GTM Research views opportunities for smaller systems as the most challenging to scale, given many of the issues discussed above. However, he notes that this opportunity has more potential upside than any other strategy being tracked given the thousands of rooftops.

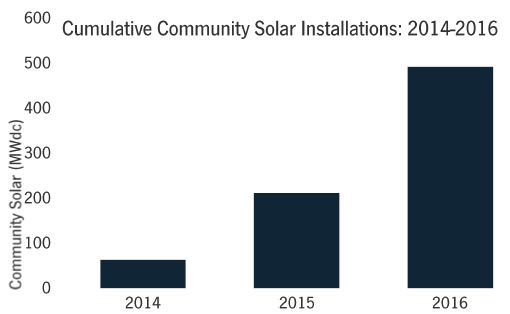

Community solar

GTM Research identified four states where community solar projects are beginning to take hold: California, Colorado, Massachusetts and Minnesota. The latter two present the greatest opportunity due to a combination of net savings on energy bills and uncapped development.

To date, there are more than 50 community solar programs in operation or in planning stages. By the end of 2016, GTM Research expects nearly 500 megawatts of community solar installations to come on-line.

Source: GTM Research Solar Executive Briefing, Q1 2015

Fortune 500 partnerships

Honeyman described Fortune 500 partnerships as the longstanding low-hanging fruit of the commercial solar market. Projects benefit from economies of scale with large installations, and they address some of commercial solar’s biggest bottlenecks like prolonged contractual due diligence and other extraneous transaction costs.

The briefing cites Target’s recent signing of a portfolio-wide PPA arrangement with Greenskies for a 122-megawatt rooftop solar project.

"At the top level, the non-residential market’s struggle to scale can be partly attributed to the segment remaining a few steps behind residential solar, in terms of tackling soft costs and improving the customer acquisition process," said Honeyman. "But at the same time, the solutions to scaling up non-residential solar will only to an extent come from strategies deployed in the residential market, given the non-residential market‘s inherently heterogeneous customer base and project profiles."

"So what’s perhaps most encouraging about the non-residential market in 2015 is increased efforts to provide standardized customer product offerings tailored to individual segments within the non-residential market, be it Clean Energy Collective or SunShare’s community solar deals or Greenskies’ PPA offering to big-box retail outlets," added Honeyman.

"These business models point to a growing number of companies that can provide replicable development and sales strategies to distinct but large pockets of the broader non-residential market, yielding new opportunities to lower soft costs and subsequently increase the velocity of non-residential megawatts deployed in the next two years."

***

The Solar Executive Briefing is delivered quarterly to GTM Research solar subscribers. The most recent edition contains updates on the PV supply chain, PV systems and technologies, global demand, U.S. installations, and U.S. PV market leaders.

For more information, download the brochure here or contact GTM's Matt Casey at [email protected]

41

41

15

15

9

9