Have we already won?

Could we have already reached a point where current trajectories for renewable energy, energy efficiency and alternative transportation are clear enough that we can reasonably suggest that a revolution has occurred?

Yes. For the most part, the game is indeed won. We are on the path to renewable energy ubiquity -- and it’s unlikely to be derailed even if policy support falters for these technologies.

There are still some uncertainties, but let’s start by examining the clearer trajectories.

Renewable energy is trending rapidly toward ubiquity

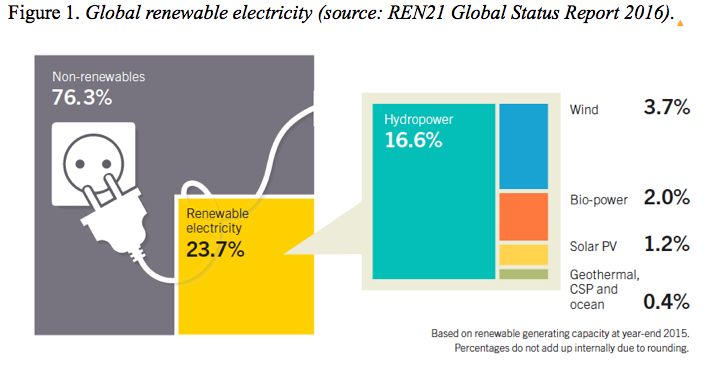

Excluding large hydro, renewable electricity is still only at about 7 percent globally, and about the same in the U.S. Even at 7 percent globally, however, we can see the future fairly clearly because of the long-established relationship between installations and the falling price of renewable energy.

Swanson’s law describes this relationship with respect to solar power, the renewable energy technology with the most promise. This “law” suggests, based on the last few decades of evidence, that the cost of solar power drops by about 20 percent with every doubling of installations. I’ve addressed this in detail in this article. And it’s described in this podcast by Dick Swanson himself.

If history is any guide -- and we have some very solid historical data in this case -- then we can be fairly sure that this cost-reduction trend will persist as installations continue to increase, in a tight virtuous cycle of ever-decreasing prices that trend asymptotically to zero.

According to GTM Research, global installations are on track to hit 73 gigawatts in 2016, up from 55 gigawatts in 2015. By 2021, the yearly global installations are expected to hit 105 gigawatts. The price of solar has indeed continued to fall as solar installations have ramped up dramatically in recent years. I’ve discussed this trend in previous articles, describing it as the “solar singularity,” which I define as the point where a majority of countries begin installing solar power as the default power source.

We are currently facing a glut of solar panel production, primarily from China, so we can expect even more robust cost declines in the next year or so than would normally be expected.

Given this multi-decade trend in solar power -- and similar cost declines in wind and other renewables -- we can reasonably expect that solar power and other renewables will trend toward ubiquity in the next two to three decades (80 percent penetration is my rough threshold for ubiquity, since we’ll very likely maintain some fossil plants for a few decades to come as backup power sources). When it comes to electricity, then, we have valid reasons to think that, yes, the revolution has indeed already been won.

The world is inevitably becoming more energy-efficient

We see similarly encouraging trends toward increased energy efficiency, both here in the U.S. and globally. There is no named “law” for energy efficiency to improve as economies develop technologically, but there is a clear trend here too: as nations develop economically, they become more energy-efficient.

The usual trend for nations climbing the ladder of economic development is to see less energy required for each unit of economic activity. The result of this trend is, of course, that energy becomes less costly (in absolute terms; in unit terms it can become more costly, but because greater efficiency means less is used, the net result is lower cost for energy), and this is another virtuous cycle for economic development: The more developed an economy becomes, the cheaper energy becomes, and so on.

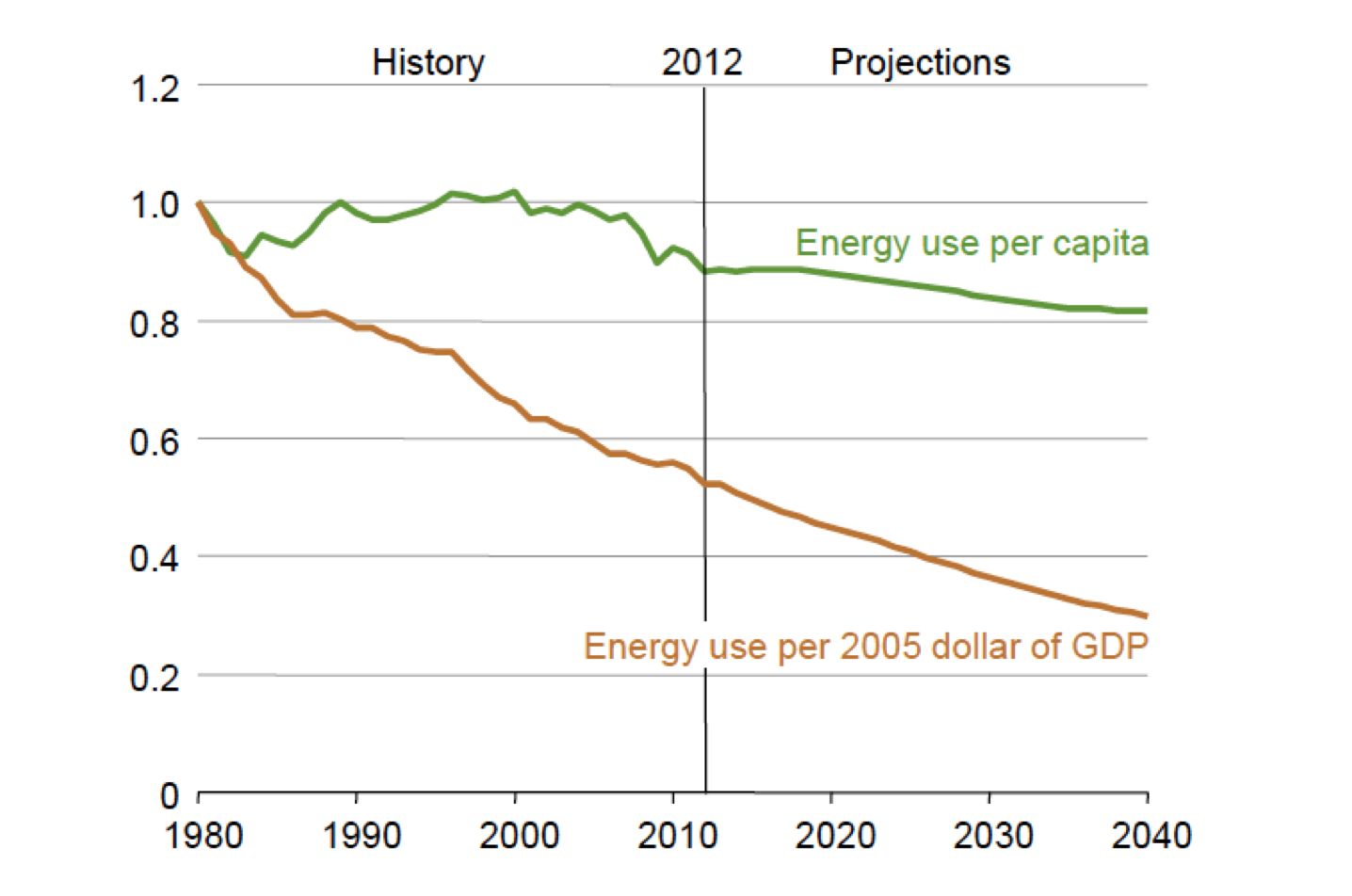

The U.S. has become far more efficient in recent decades, and the Energy Information Administration projects a 2 percent annual improvement in energy intensity (energy per dollar of GDP) through 2040, allowing us to achieve a massive 50 percent improvement in overall efficiency by 2040.

FIGURE 2: EIA’s Energy Intensity Projections

Source: EIA AEO 2014

As economies develop into more trade-based and technology-based economic sectors, less energy is required. Additionally, as nations develop they upgrade older equipment and we see a very steady trend toward steadily improving energy efficiency in electronics and other power-using devices.

The International Energy Agency recently estimated that improving energy efficiency saves developed countries $540 billion each year. That’s real money. Interestingly, the total energy consumed by developed nations appears to have peaked in 2007, and ongoing efficiency and conservation improvements may continue the downward trend.

A clear standout in the energy-efficiency field is the lightning-fast development and cost declines for LED light bulbs, which have quickly surpassed CFLs as the go-to environmental lighting option. Costs for LEDs have come down 94 percent since 2009 and are poised to continue to decline. Goldman Sachs projects that LEDs will account for nearly 100 percent of new lighting sales by 2025 in the U.S. -- which means that by around 2030, the vast majority of the U.S. will be lit by LEDs. And it’s just a matter of time before other countries also quickly transition over to LEDs.

An obvious benefit of LEDs over CFLs is the broader color and dimming options. Combined with ongoing cost declines and better durability, it is abundantly clear that LEDs are quickly taking over the world of lighting.

There is no clear endpoint for possible energy-efficiency improvements (as there is for renewables, which can “only" reach ubiquity and must stop there), so we can’t declare victory in the energy-efficiency revolution in the same way that we can for renewables. However, we can rely on the long-term trend toward ever-improved energy efficiency as a highly important component for reaching a fully renewable energy future.

Electric car adoption is growing rapidly, but still not trending toward ubiquity

Alternative transportation is the sector that holds the most uncertainty. EVs, clearly the most promising alternative to fossil-based transportation, currently account for about 1 percent in global sales. This is low, but, as with renewable energy, a steadily doubling of sales quickly leads to ubiquity. It takes just seven doublings to get from 1 percent to 100 percent. To what degree will the recent rapid pace of sales growth continue?

A recent Goldman Sachs report estimates that about 50 percent of all new car sales will be EVs by 2025. Under this trend, we’ll see almost all new cars become electric by around 2030. With an average vehicle lifetime of 10 to 15 years, it is possible that our entire passenger car fleet will become electric by around 2045 or so. This is encouraging.

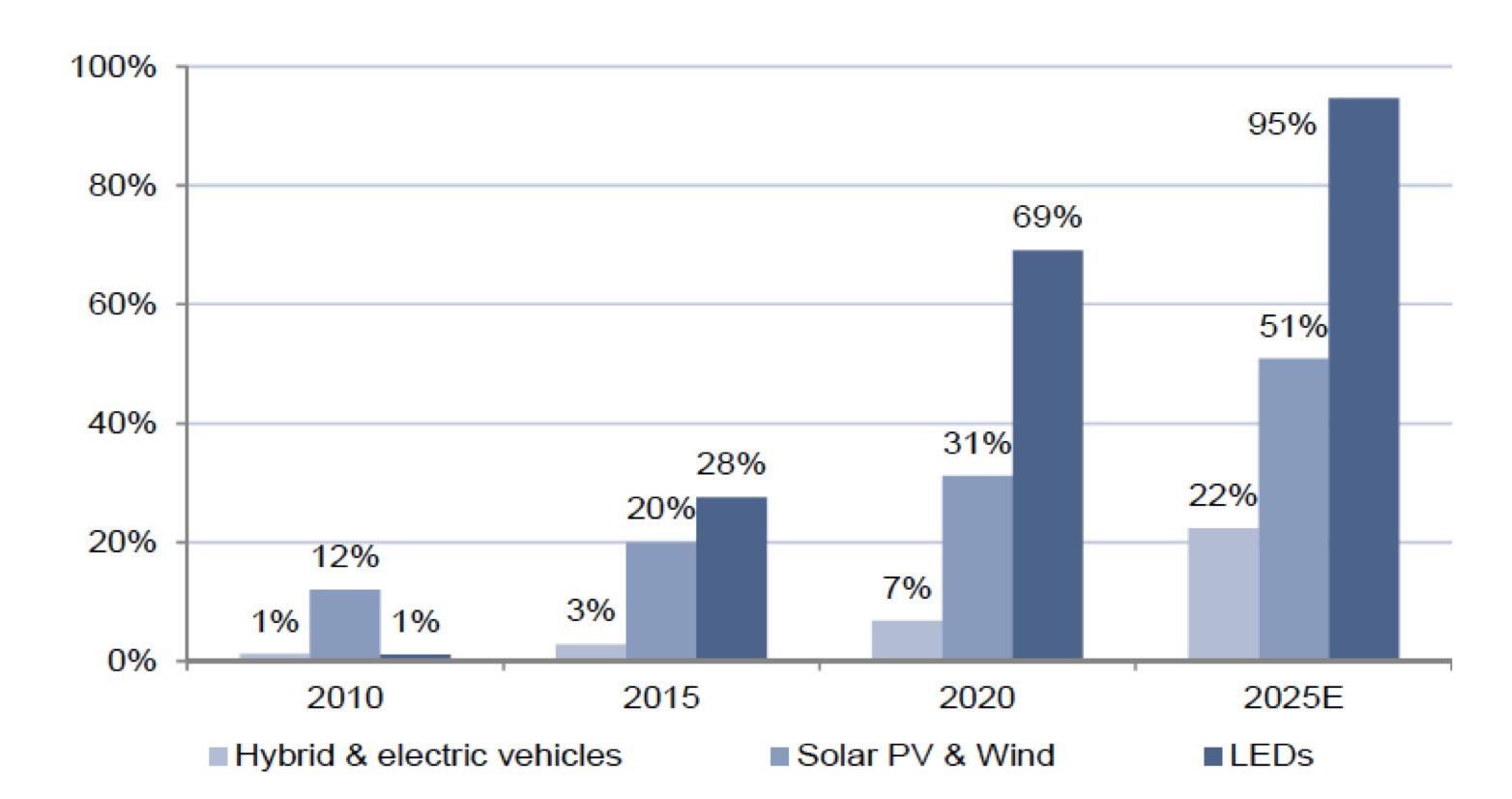

FIGURE 3: EV, Solar and LED Sales Estimates for 2025

Source: Goldman Sachs

We’re also seeing dramatic progress in the number of EV charger installations. The U.S. has gone from almost zero chargers in 2000 to 14,576 chargers and 36,810 outlets now, according to the U.S. Department of Energy’s website.

China, however, is leading the way now, with 31,000 charges installed in the first half of 2016 alone, bringing the current total in China to 81,000. This is an average of 170 new EV charging stations every day. A 2015 IHS report projects that about 13 million EV charging stations will be installed globally by 2020.

However, it’s not entirely clear yet if sales will continue to double quickly enough to reach ubiquity in a reasonable timeframe.

Hybrid cars have been around for 20 years and have not surpassed about 3 percent of total sales in the U.S. EVs, whether plug-in hybrids or pure EVs, have more promise than regular hybrids because of the many obvious advantages that EVs offer -- including all-electric drive, rapid acceleration, smooth drive, great handling, and being able to literally drive on sunshine from solar panels on your own roof.

The key downside, and the main source of uncertainty for EVs, is their higher cost. Even though we are already seeing very positive trends in cost reductions for batteries and EVs more generally, we have nowhere near as long a track record for EVs as we do for solar, for example. So it’s not possible to offer strong predictions about whether or when EVs will reach ubiquity. If costs don’t continue to decline and if range doesn’t continue to increase, it’s unlikely that EVs will reach much higher than traditional hybrid sales figures.

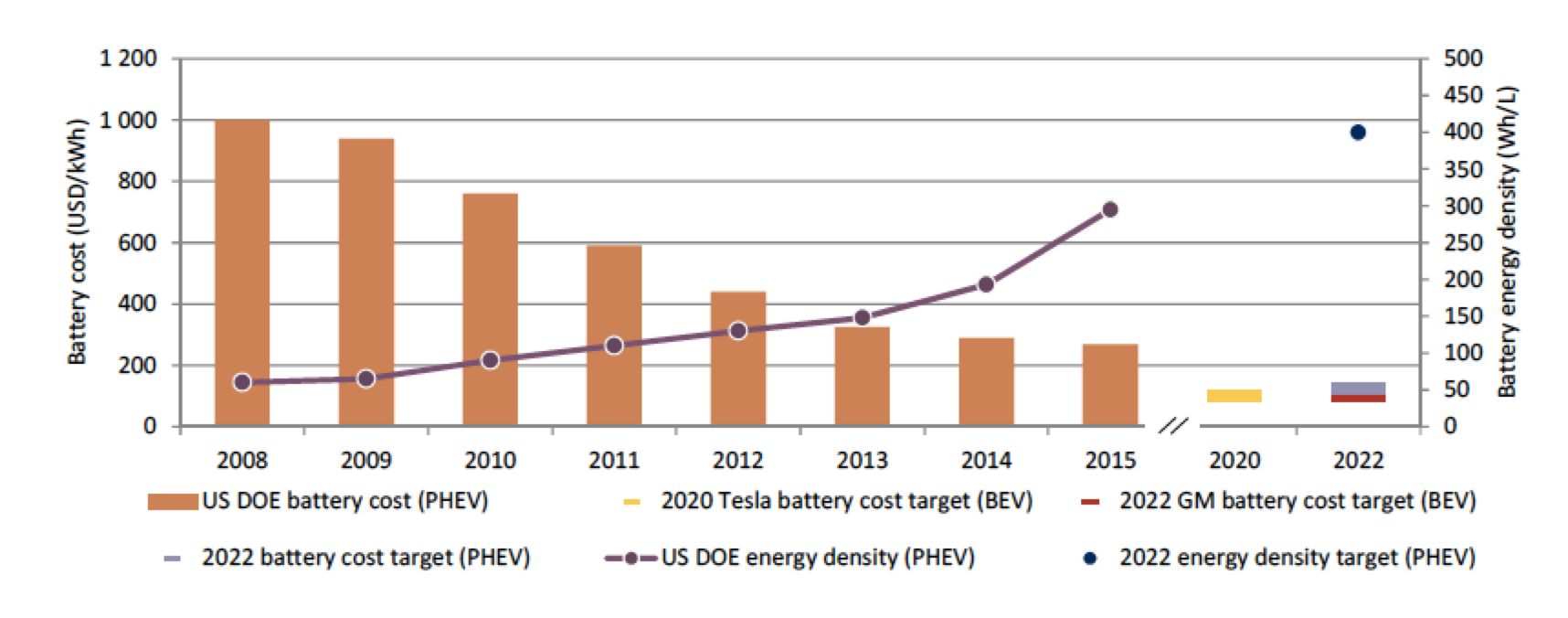

FIGURE 4: Battery Energy Density and Costs, Historical and Targeted

Source: IEA Global EV Outlook 2016

In the next few years, however, we should have better clarity on this issue, as GM, Tesla, and other manufacturers that are targeting the affordable 200+ mile vehicle segment introduce new models. The Chevy Bolt is now available for purchase, and deliveries will start later this year. The Tesla Model 3 has famously achieved about 400,000 preorders (I’m one of them), and deliveries are slated to begin late next year.

A number of other manufacturers have announced plans for similar long-range affordable EVs, but it’s too early to say yet whether these prices will actually be achieved and whether the quality and durability of these vehicles will be sufficient to sway mainstream consumers away from traditional vehicles.

I’m optimistic. But we’ve got to wait a few more years before we can achieve more confidence in the EV revolution. A 2016 Bloomberg New Energy Finance report suggests that EVs will account for only 35 percent of new light-duty vehicle sales by 2040. I think this forecast will change rapidly as new and better EVs come to the market.

What could derail the revolution?

Many were surprised by the fracking revolution for natural gas and oil. As I wrote in a piece last year, the Peak Oil crowd (of which I count myself a member) was left looking a bit silly in light of dramatically lower prices as U.S. production has increased. It’s a complex issue, but my view is that we’re still likely to see another large price spike before 2020 as U.S. production falls back down the curve. With almost all global net gains in oil production coming from U.S. fields, there is still massive risk for price spikes and even short-term shortages.

But with new technologies leading to higher production of oil and gas in the U.S. -- and to a much lesser extent, in other countries -- there is certainly some long-term risk for the renewables revolution in terms of chronically low fossil-fuel prices. The virtuous cycle for lower renewable energy costs has a similar effect on fossil-fuel prices: As renewables gain more market share, demand for fossil fuels diminishes and prices diminish along with demand.

At the least, this dynamic could slow down the renewables revolution. It could particularly hinder the EV revolution, because the cost of fuel will always be a strong factor in consumer purchase decisions. It’s a real testament to the quality and appeal of EVs that sales have grown in the last two years even in a relatively low-price fossil fuel environment.

Even if fossil fuel prices do stay low, however, my intuition (and that is really all I can offer here) is that the cost curves and improvement curves for EVs are sufficiently well established that we’ll see steady growth, even in the worst-case scenario. But steady growth could still take a very long time to reach ubiquity.

To reach ubiquity in a reasonable timeframe -- by 2040 or so -- we’ll need to see continued annual growth rates in sales of 30 percent or so. We’ve seen much higher growth rates than this in the U.S. and globally in recent years, but all growth rates slow eventually. The question here is how much they will slow down.

Another source of risk is the degree to which countries maintain incentives for renewable energy, energy efficiency and EVs. However, even if nations start to phase out incentives in the next few years, we’re probably far enough along in the renewable energy revolution to continue progress. If incentives are cut, we’ll see a slowdown in the revolution, but not a halt.

In sum, the renewables revolution is probably already won for renewable electricity and improving energy efficiency -- but it’s less clear that we’re over the hump for the EV and transportation revolution. The Energy Information Administration thinks the U.S. has already achieved significant progress in this ongoing revolution, as described in a recent GTM article.

The U.S. is doing great and has returned to the top of the Ernst & Young Renewable Energy Country Attractiveness Index, so we are no laggard in this space. That said, it’s not time just yet to relax and rest on our achievements -- but in a few years, perhaps, we can all take a much-needed extended vacation.

***

This story was updated with correct global renewable energy figures.

41

41

15

15

9

9