According to a study by Ernst & Young, 53 companies filed paperwork to hold initial public offerings in Q4 2009 -- the highest number of new registrants in a single quarter since 2007. That means that there are more deals in the IPO pipeline than there have been for more than two years.

And a number of those IPOs happen to be high-profile offerings in the greentech sector.

For several years I've been predicting that 2010 would be the year of the Greentech IPO. Surprisingly, especially to me, I seem to have been right.

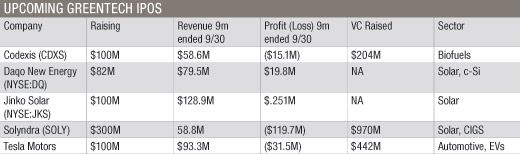

Some facts and figures on the greentech IPOs now on-deck:

Solyndra

Solyndra's innovative photovoltaic glass cylinders are full of it -- full of vacuum, silicone and thin-film CIGS in a relatively low-efficiency configuration. Several of Solyndra's VC investors have told me that the real value for Solyndra is in the cost savings in the Balance of System. Will the institutional investors who drive the success of an IPO buy the Solyndra BoS story? Especially when the cost per watt of c-Si and FSLR CdTe continues to fall? And the cost of Solyndra's product seems somewhat bloated?

A lot rests on the shoulders of Solyndra: the perception of the viability of CIGS technology, the perception of the viability of VC investment in solar manufacturing, and the skill of the DOE in picking technology winners.

We parsed the Solyndra S-1 here.

GTM Research analyst Shyam Mehta did a masterful job at dissecting the Solyndra situation here.

Here is the Solyndra S-1.

An exploration of Solyndra's price per watt.

Tesla Motors

Like Solyndra and A123, Tesla is a "story stock." And like A123 and Solyndra, Tesla anticipates "continuing losses for at least the foreseeable future." A123 and Telas stand as proxy for the EV vison, Solyndra for the promise of new solar technologies.

Tesla reports having sold 937 cars through December 2009 to customers in 18 countries.

The company has booked 2,000 reservations for the $57,400 Model S, the all-electric sedan that enters volume production in 2012. According to the SEC document, the Model S will offer a variety of range options, from 160 miles to 300 miles on a single charge.

Major investors in Tesla are Elon Musk, Al Wahada Capital, a fund owned by the power and water authority of Abu Dhabi and Blackstar Investco, an investment arm of Daimler.

Michael Kanellos reported on the Tesla IPO numbers here. Tesla's S-1.

Will institutional investors back a lossy luxury car vendor with an unhealthy dependence on government loan guarantees?

Codexis

Here's the Codexis S-1.

Codexis is funded by CMEA, Shell and CTTV, the investment arm of Chevron.

The firm's biocatalysts are used in the pharmaceutical industry, but the greentech angle is the deal that Codexis has with Shell to produce commercially viable biofuels from cellulosic biomass. Other green applications for their product include carbon management, water treatment and "green" chemicals.

Their advanced biofuels program focuses on: (1) developing biocatalysts to convert cellulosic biomass into sugars; and (2) converting these sugars into two advanced biofuels, cellulosic ethanol and biohydrocarbon diesel.

Codexis has the advantage of looking at several target markets and the luxury of some very large and important customers.

Jinko Solar Holdings

Jinko is a fast-growing, vertically integrated solar supplier with more than 400 customers and a deep relationship with troubled solar aspirant Hoku. Jinko Solar Holdings is first out of the gate and expected to begin trading on the NYSE on February 10.

Other greentech firms that have a chance at the public market in 2010 and 2011 are LED maker Bridgelux, biofuel producer Amyris, PV micro-inverter firm Enphase Energy, CIGS thin-film producer Nanosolar, and stealthy natural gas-powered fuel cell firm Bloom Energy.

It will be an interesting year.

41

41

15

15

9

9