First Solar is the largest solar module firm by market capitalization, the largest thin-film solar firm, and one of the largest solar firms by capacity, shipments, and certainly by cumulative profits. The company is in the cross hairs of every other solar firm and continues to set the bar in terms of solar panel value and corporate performance.

What first Solar does in the next few years is important.

Which is why more than 200 people showed up last week to attend a presentation by Alex Panchula, First Solar's Manager of Performance Analysis, presented by the Silicon Valley PV Society chapter of the IEEE.

First Solar shared its slides with GTM, and we'll pass on the more interesting of the bunch.

In First Solar's view, the future of photovoltaics is at the utility scale, but the innovation is "beyond the module." And it's not just power plants or even systems, according to Panchula -- but rather about solving problems and providing solutions.

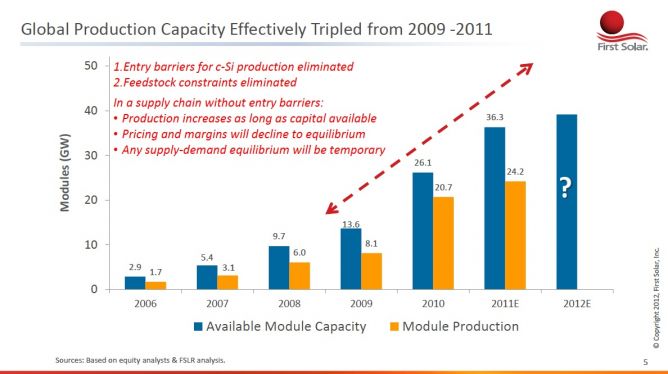

First Solar notes that global capacity has effectively tripled since 2009 in a supply chain without any barriers to entry in c-Si and a situation where supply oscillates between constrained and oversupply.

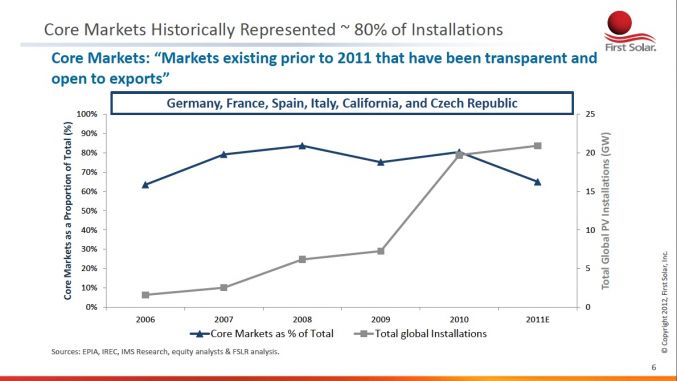

The core markets for photovoltaics -- Germany, France, Spain, Italy, California, and Czech Republic -- are just a small slice of the world. Still, these core markets, which were 15.8 gigawatts in 2010, dropped to 13.6 gigawatts in 2011. Panchula asked, "Are the wheels going to fall off in 2012?"

And here's the problem with those core markets (which GTM has dubbed 'savior markets'): the subsidy regime has a tendency to peak and fall, or in many cases, crash, as shown in the following slides. First, the Spanish crash of 2008:

_682_388_80.jpg)

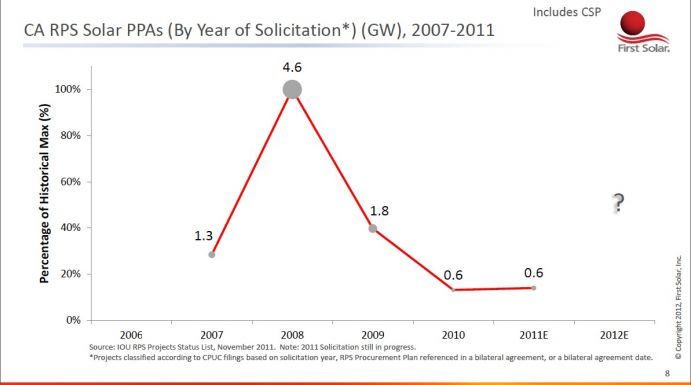

Here's the California renewable Portfolio Standard PPA collapse:

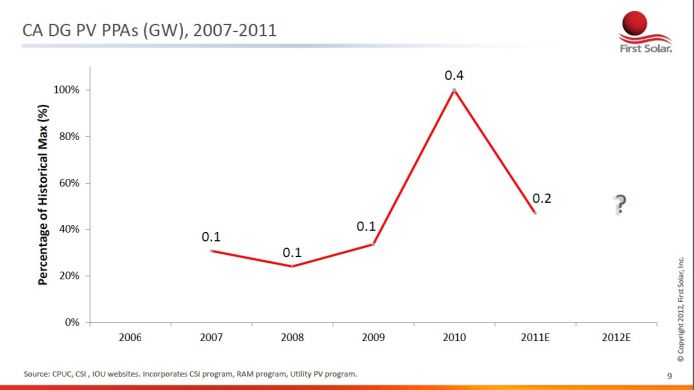

And likewise, distributed generation PPAs in California:

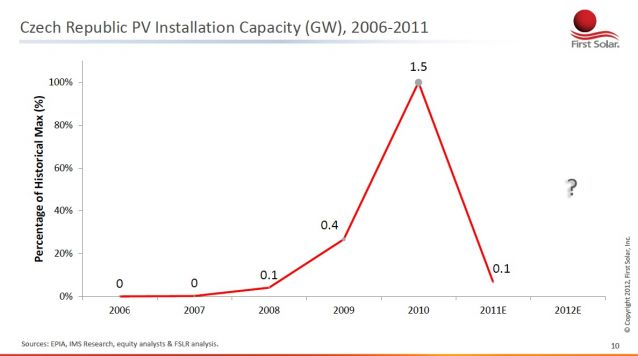

Here's the ugly picture for the Czech Republic:

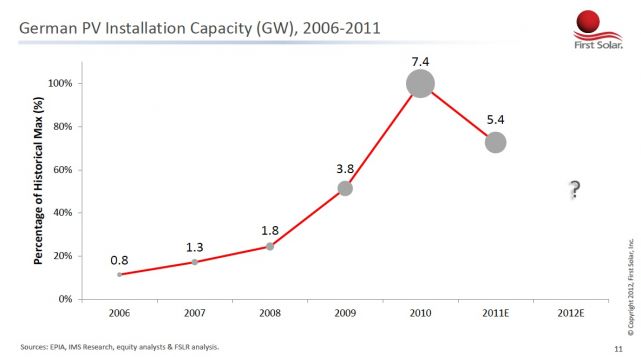

And the German situation (although those estimates of 2011 seem a bit low. We've seen estimates that show 2011 finishing at closer to 7 gigawatts). So perhaps not a crash, but definitely not the growth that First Solar or the solar industry needs to thrive.

Panchula sees it as unlikely that new markets like India will repeat this again, saying, "Countries in the developing world cannot afford subsidies."

So the question that First Solar confronts is: does the firm continue to play 'whack-a-mole' and pursue the less-than-rational subsidy markets? Or do they pick a different game to play?

According to Panchula, First Solar must deploy 65 gigawatts over the next 10 years in order to thrive, instead of playing whack-a-mole. First Solar's goal is to get new sales from sustainable markets by 2014. That means eliminating the dependency on subsidies and getting the price of solar down to levels where it is genuinely at grid-parity at utility scale in developing nations.

We'll look at how First Solar intends to do that in Part 2 of this series next week.

41

41

15

15

9

9