Three battle-scarred renewable energy veterans, now deep in the energy storage industry, confronted the challenges of getting energy storage projects financed in 2015 during a panel discussion at the recent Grid Edge Live conference. The panel paid repeated tribute to the "solar/energy storage parallel" narrative.

When it comes to solar project finance, the PV market is in the midst of a small golden age of sorts. Tax equity funds and PPAs are now joined by asset-backed securities, the potential for MLP status, loans, community solar, PACE financing, and solar bonds as some of the tools that can back solar projects.

Energy storage can only hope for a similarly robust investment environment in its near future. Right now, energy storage really only has project-finance funding totaling a few tens of millions (USD).

Paul Detering, CEO of Coda Energy, noted, "As solar matured, it bifurcated to [investors] who wanted to own assets and people investing in a corporation. In energy storage, it's still very early, and we still see a blending of the two. At Coda, we have investors in corporate purposes, as well as in projects. We currently own the projects on our balance sheet." Detering expects to see new and "interesting models" emerge in terms of how energy storage revenue streams are shared.

Coda has teamed with Fortress Investment Group to launch a no-money-down financing program for demand-charge reduction for commercial and industrial customers. It’s the same approach taken by startups like Stem, Green Charge Networks, and SolarCity with its partner Tesla.

Tom Leyden, another panelist with decades of experience in solar, was asked if the pitfalls for energy storage are the same as for solar. Leyden said that when he was at PowerLight, a 50-kilowatt project was the biggest in the country at the time. He said it was hard to get financed then, but now Warren Buffett is making $2 billion investments in solar. Leyden added, "Energy storage is new and anything new has risk. It's kind of hard to monetize the benefits that energy storage provides."

SunEdison acquired Leyden's company, Solar Grid Storage, to beef up its storage offering, in turn allowing SGS to gain access to SunEdison’s financing and reach. Leyden suggested in a previous interview that SunEdison would be looking to co-locate storage with solar or wind projects.

"Storage doesn't have long contracted revenues; we can't go into the YieldCo." He also noted that SGS was big in PJM's frequency regulation market, "but it's not contracted revenue." He added, "My job at SunEdison is to get the YieldCo comfortable with energy storage. When we do, it will be groundbreaking."

Gerrit Nicholas, president of K Road DG, said, "Storage really is taking a similar pattern to solar. The difference is that you don't have the same contractual structures that will evolve as technology and the market evolves." He added, "In the 2010 solar market, the worry was construction risk. Today, nobody thinks about construction risk in PV."

Leyden said, "We're going to add the ability to communicate with energy storage systems around the world." He suggested that a small and large system in Illinois or Maryland could "act as one asset," identifying this approach as "the evolution of the grid."

Moderator Ravi Manghani, senior analyst of energy storage at GTM Research, summed up the panel this way: "A recurring theme was that advances in storage financing are going to come more quickly, taking advantage of financing innovations (and mistakes) on the solar side. Second, while these comparisons between solar and storage are interesting conversation points, it is important to note that value streams provided by storage differ from traditional solar PPAs. What makes storage financing interesting and challenging at the same time are the different value streams that can be accrued along the grid, and by different participants."

He added, "In many cases, these value streams are yet to be monetized, so unlike solar PPAs that are expected to stay flat (or grow per some set escalator), storage assets financed today for a particular use case such as demand-charge reduction could be used for other applications such as frequency regulation or capacity performance in the future. But figuring out the right financing vehicle for those assets today still remains a challenge."

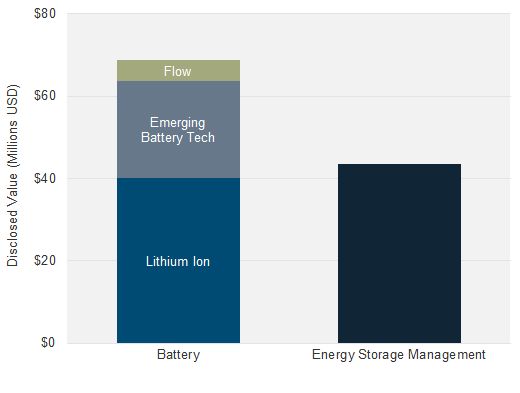

GTM Research predicts the U.S. will deploy 220 megawatts of energy storage in 2015, with the market on a path to reach 861 megawatts of annual installations and a value of $1.5 billion in 2019, about 11 times its 2014 size. Meanwhile, energy storage companies have garnered about $112 million in investment so far this year, with about $40 million going to energy storage management providers Greensmith, Advanced Microgrid Solutions and Stem. Other key energy storage management software providers include Geli and 1Energy.

Figure: 2015 Investment in Energy Storage

Source: GTM Research

41

41

15

15

9

9