The first-generation ethanol industry has enjoyed a rare spate of good news lately (see A Comeback for Corn Ethanol?). Low corn prices have resulted in improved margins. Companies like The Andersons and Green Plains Renewable Energy have announced blowout earnings in recent weeks. The EPA recently re-affirmed corn ethanol mandates via the Renewable Fuel Standards (see EPA Issues Renewable Fuel Standards) of 12 billion gallons in 2010 from 10.5 billion in 2009.

While there are questions about whether Congress will allow the $0.45/gal blenders credit to lapse at the end of 2010 in a similar way that the $1.01/gal production credit for biodiesel was not extended (see The State of U.S. Biodiesel), for the most part, the corn ethanol industry's short-term prospects look good.

Although only 6.5 million gallons of 2nd Generation cellulosic ethanol is expected to be produced in 2010 (see Spotting the Next Wave), this number is expected to ramp up in coming years. Combined with Brazilian imports of 1 billion gallons per year, the U.S. could have 14 billion gallons of ethanol in 2011.

Yay for ethanol!

Not so fast.

14 billion gallons of ethanol would represent approximately 10% of the 140-billion-gallon U.S. gasoline market on a volumetric (not energy) basis. Considering the paucity of E-85 ethanol pumps and the dearth of Flex Fuel Vehicles compared to the overall mix of cars and trucks running on gasoline, we can assume that the vast majority of ethanol produced in the U.S. for the foreseeable future will be used as a blend.

Which brings us to the concept of the "blend wall."

Under current EPA policy, gasoline engines are only approved in blends up to 10% ethanol.

Higher blends of ethanol can affect engines in a variety of ways. For example, one concern is whether an engine's fuel control system can adequately compensate for the higher oxygen content associated with higher ethanol blends.

In October 2008, the National Renewable Energy Laboratory and Oak Ridge National Laboratory released a report entitled, "Effects of Intermediate Ethanol Blends on Legacy Vehicles and Small Non-Road Engines." The report examined 13 popular late-model vehicles under real-world driving conditions and analyzed factors such as: exhaust and catalyst temperatures, engine performance, and observable operational issues. The report used E0, E10, E15, and E20 blends in the 13 vehicles and also in a number of small nonroad engines.

Among the findings were:

- Loss in vehicle fuel economy in proportion with the energy density of the fuel

- Vehicle tailpipe emissions remained largely unaffected by the proportion of ethanol in fuel

- As ethanol blends increased, temperatures of exhaust components and cylinders also increased. Exhaust temperatures jumped between 5°C and 10°C when blends increased from E10 to E15

- Higher ethanol content corresponded to higher idle speed and unintentional clutch engagement in three handheld line trimmers

Ethanol lobbyist groups, like Growth Energy (co-chaired by General Wesley Clark), have petitioned the EPA to raise the amount of ethanol sold in most gasoline to 15%.

On December 1st, 2009, the EPA ruled that "although all of the studies have not been completed, our engineering assessment to date indicates that the robust fuel, engine and emissions control systems on newer vehicles (likely 2001 and newer model years) will likely be able to accommodate higher ethanol blends, such as E15."

The EPA is expected to announce its final rulings mid-year.

If the EPA decides that E15 is safe for newer models but unfit for vehicles manufactured before 2001, there could be a number of logistical problems. For example, consumers might not know off-hand whether their car is older than the 2001 model year and could inadvertently put in the wrong fuel. Additionally, large convenience stores and discount service stations (i.e., Wal-Mart) might have 25 fuel pumps, creating an added difficulty for the store managers forced to monitor their customers and make sure they are using the correct blend.

Which brings us to the issue of liability.

What happens if the EPA makes a decision to dismantle the blend wall, and it turns out that E15 does adversely affect boats, lawnmowers, and other appliances using gasoline?

Who is liable? Ethanol producers? Gas refiners? Automobile manufacturers? The federal government? The consumer?

Given that most automobile and motor equipment manufacturers have warranties that are valid for E10, these companies would have to extend warranties to cover engines running on blends above 10%.These companies have no self-interest to act on their own accord without carrots (e.g., government guarantees liabilities) or sticks (e.g., the government requires that as a condition of entering the U.S. market, the engine must be able to accommodate blends above E10).

Although we believe that there is a high likelihood that the EPA will increase the blend wall, we have to ask: if the blend rates were not increased (due to aforementioned technical or logistical problems), what are the alternatives to accommodating the tremendous increase in ethanol supply projected in the coming years?

Proponents of ethanol point out that companies like Ford and GM have pledged that 50% of their gasoline vehicles will have "Flex-Fuel" capability by 2012. Flex-Fuel Vehicles (FFVs) have been the main growth catalyst in recent years in Brazil, as close to 90% of all passenger vehicles that will be sold in Brazil in 2010 will be FFVs. In fact, the 7 million flex fuel vehicles on the road in the U.S. outnumber the amount in Brazil (6 million).

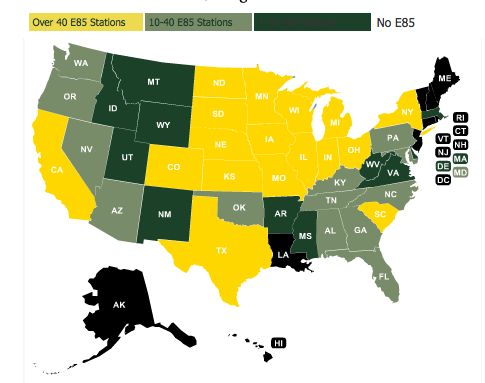

Although it is relatively inexpensive to convert one's gasoline engine into a FFV (<$500), only 1% of all gas stations in the United States have E85 ethanol pumps (2246 E85 pumps vs. 169,000 gas stations). Most of these pumps are located in the Midwest, far away from the large population densities on both coasts (e.g., one-fifth are located in Minnesota). Consumers are faced with the chicken-and-egg question of whether to get a FFV: why pay extra if there are no E85 stations close by?

(courtesy: http://e85vehicles.com)

The EIA estimates that it costs $22,000-$80,000 to replace one gas pump and retrofit it to carry E85. While the "Alternative Fuel Infrastructure Tax Credit" (under the Energy Policy Act of 2005) provides a tax credit equal to 30% of the cost of implementing alternative refueling equipment, project finance for ethanol projects (even on the downstream infrastructure side) is not exactly flowing.

The coming blend wall debacle is a great example of what happens when Congress picks and chooses technologies without thinking holistically about the long-term consequences that can occur when those technologies "win."

41

41

15

15

9

9