It's tough times for concentrated photovoltaic (CPV) solar firms. GreenVolts went under and Amonix went quiet after shuttering its Nevada factory and laying off much of its staff last year. SolFocus is trying to sell itself and finding no buyers. Only Soitec seems to be developing new CPV systems, helped presumably, by a healthier balance sheet.

I listened to Amonix founder, CTO, Chairman, and former CEO Vahan Garboushian speak on the state of concentrated photovoltaics in a webinar yesterday put on by PV Insider in anticipation of what will be the world's most depressing solar conference.

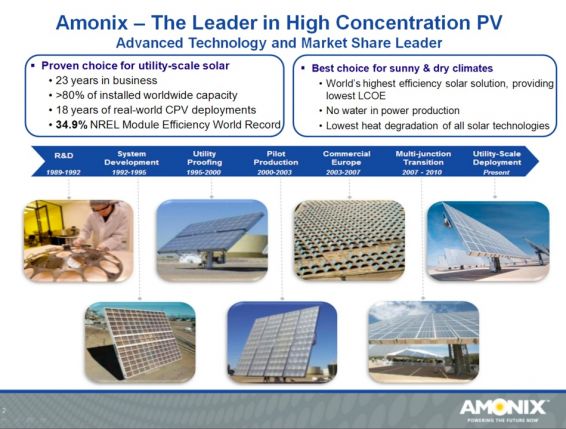

Amonix is/was a pioneering CPV vendor that developed product, grew organically and led this small industry with about 80 percent of its installed base. The firm went through a number of product revisions -- moving from low-concentration silicon to high-concentration, triple-junction solar cells and steadily increasing the scale of the design.

But, with solar's growth curve on the upswing, the firm succumbed to the siren's song of venture capital, rapid growth, and the promise of wealth. Instead, the price of silicon dropped -- and the CPV industry remains trapped with an underdeveloped technology, an immature supply chain and technologists like Garboushian wondering what happened.

In what could have been a re-broadcast from 2007, Garboushian said that concentrating PV is the "next big PV happening," that "the potential is great," and that "we think it has the lowest LCOE [levelized cost of energy]." Garboushian also claims that CPV has the lowest capital cost -- at 35 cents per watt -- to build a factory.

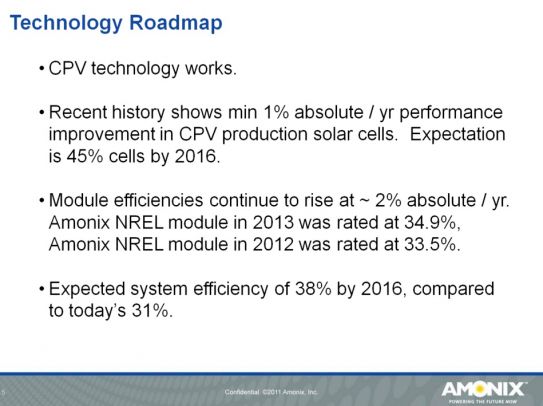

Amonix holds the world record for a CPV module with a 34.9 percent conversion efficiency.

Garboushian maintained that the idea of CPV is sound and valid and demonstrated with the 30-megawatt CPV installation in Alamosa, CO, owned by The Carlyle Group. The founder of Amonix said that the plant has a 99.6 percent availability and is generating 2,500 kilowatts per kilowatt-hour at the 6.7 DNI site. We've heard otherwise, and have asked Amonix and the plant owner to share that information in the past, but have yet to receive any documentation.

He called CPV bankable technology -- but it's hard to be considered bankable if the vendor is not going to be around in one year, let alone twenty.

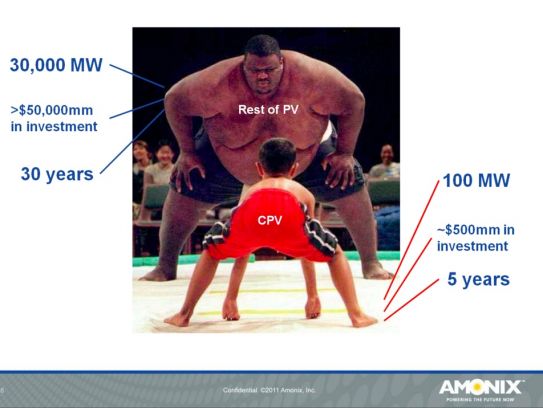

Garboushian described CPV as an impoverished market with 100 megawatts deployed and $500 million invested over the last ten years, compared to the $50 billion received by the silicon industry. Garboushian said that what CPV needs is a supply chain, large-scale manufacturing, consolidation of the technology, and a big corporate backer instead of VCs looking to flip companies in a few years' time.

In April, Amonix signed a co-development agreement with triple-junction solar cell upstart Solar Junction. This announcement looks to be coming out about five years too late, given the painful decline of Amonix and the fierce learning curve of c-Si.

Ben Kortlang of Kleiner Perkins is on Amonix's board of directors and is a former employee of Goldman Sachs. Years ago, Kortlang told me that the Amonix LCOE and cost per watt were lower than First Solar (about $0.65 per watt today and headed lower).

A colleague and early employee at a rival CPV firm notes, "The CPV industry remains locked in a battle against declining costs with silicon technologies. The 2012 surge in cost reduction achieved by silicon may ultimately prove to be the death blow to today's commercial CPV providers, though there continue to be innovations in CPV cell efficiency and module design that could keep the technology alive in the highest-DNI environments. The big question is whether silicon will allow some breathing room in 2013 with the price increases that some predict, or whether further cost and price reductions in 2013 make the gap wholly uncrossable."

I've sent email and left phone messages with Amonix PR, Ben Kortlang of KP, and Vahan Garboushian and await their responses.

41

41

15

15

9

9